The Rule That Quietly Disqualifies Most W-2 Earners

Most people who chase Real Estate Professional status (REP, often written REPS) focus on the 750-hour test. They count showings, repairs, bookkeeping, and tenant calls, watch the total climb past 750, and assume they have qualified. Then their CPA asks the second question, and the whole plan collapses: how many hours did you spend at your day job?

REP status has two gates, and you must pass BOTH in the same tax year. The first is the 750-hour minimum. The second is the more-than-50% test: more than half of ALL the personal-service hours you worked during the year must be in real property trades or businesses in which you materially participate. The 750-hour test is an absolute floor. The 50% test is a ratio, and it is the ratio that quietly kills REP for people with full-time jobs.

The 750-hour test asks 'did you do enough real estate work?' The 50% test asks 'was real estate the MAJORITY of all your work?' A full-time job can let you pass the first while making the second nearly impossible.

This article stays narrowly on the mechanism. We are not going to rehash the tax benefits of REP or hand you a playbook of workarounds. We are going to show you exactly WHY a W-2 job defeats the 50% test, using the math itself. Once you see how the denominator works, you will understand the problem better than most investors ever do, and you will know precisely what you would have to change to beat it.

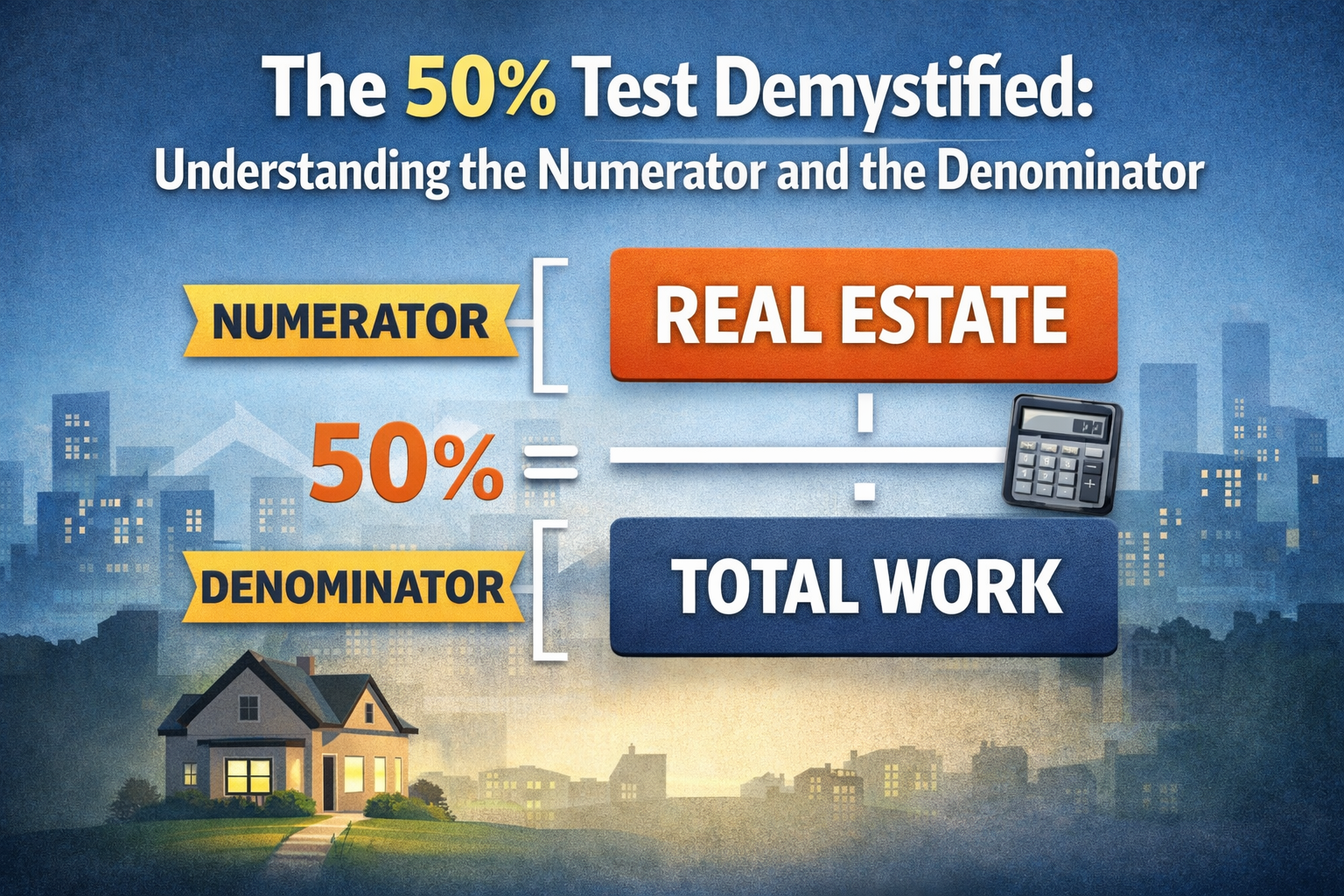

The 50% Test Is a Fraction, and Your Job Lives in the Bottom

Strip away the legal language and the 50% test is one fraction. The numerator is the hours you spent in real property trades or businesses in which you materially participated. The denominator is ALL of your personal-service hours for the year, meaning every hour of work you performed in any trade or business, real estate or not. The test is passed only when the numerator is more than half of the denominator.

Numerator (counts FOR you)

- Hours in real property trades or businesses

- Where you materially participate

- Rental management, brokerage, construction, development, acquisition, leasing, operations

Denominator (ALL working hours)

- Every numerator hour, PLUS

- All W-2 employment hours

- Any non-real-estate self-employment or side business hours

- Any other personal-service hours in a trade or business

Here is the crucial structural point: your W-2 hours are in the denominator only. They never count in the numerator (unless you are a 5%-or-more owner of the employer, which is a narrow exception most employees do not meet). So every hour you spend at your job makes the bottom of the fraction bigger without doing anything for the top. The job is pure ballast. That is the whole reason employment is so corrosive to REP.

Your real estate hours have to out-vote everything else you do for money. A full-time job is a large, immovable block of votes on the wrong side.

"More Than" Half, Not "At Least" Half

The statute says MORE than 50%, not at least 50%. A perfect tie does not pass. This sounds like a technicality, but it has a concrete consequence: if your job is exactly 2,000 hours, you cannot win the test with 2,000 real estate hours, because 2,000 out of 4,000 is exactly half. You need at least 2,001 real estate hours to push the ratio over the line.

Generalize it. If your non-real-estate working hours total J (mostly your job), then to pass the 50% test your qualifying real estate hours R must satisfy R > J. The numerator must strictly exceed everything in the denominator that is not real estate. In plain terms: you must do more real estate work than the total of all your other work, by at least one hour.

- Required real estate hours = (your non-real-estate working hours) + 1, at minimum.

- A 2,000-hour job requires 2,001+ real estate hours.

- A 1,800-hour job requires 1,801+ real estate hours.

- A 2,400-hour job (overtime, long hours) requires 2,401+ real estate hours.

The 750-hour floor and the 50% ratio interact: you must clear BOTH. With a full-time job, the 50% ratio is almost always the higher bar, so it sets the real number you have to hit, and it is usually far above 750.

The Denominator Problem in Numbers

Let's make the mechanism concrete with illustrative figures. Assume in each case the person also performs the real estate hours shown, and ask whether the ratio clears 50%. Remember: real estate hours have to be MORE than non-real-estate hours.

- Job 2,080 hrs (40/week), RE 750 hrs: total 2,830; RE share = 26.5% -> FAILS the 50% test (passes 750 floor, fails ratio).

- Job 2,080 hrs, RE 1,500 hrs: total 3,580; RE share = 41.9% -> still FAILS.

- Job 2,080 hrs, RE 2,000 hrs: total 4,080; RE share = 49.0% -> FAILS by a hair.

- Job 2,080 hrs, RE 2,081 hrs: total 4,161; RE share = 50.01% -> PASSES, barely.

- Job 1,000 hrs (part-time), RE 1,001 hrs: total 2,001; RE share = 50.02% -> PASSES.

- Job 0 hrs, RE 751 hrs: total 751; RE share = 100% -> PASSES (only the 750 floor matters).

Notice what changes the answer. In the full-time cases, even 2,000 hours of genuine real estate work is not enough, because the 2,080-hour job keeps the denominator higher than the numerator. The only full-time row that passes requires more than 2,081 real estate hours, which is roughly 40 hours every single week of the year ON TOP OF the 40-hour job. That is the denominator problem in one table.

The cruelty of the mechanism: working harder at real estate raises BOTH the numerator and the denominator at the same time. Each new RE hour adds 1 to the top and 1 to the bottom, so the ratio moves slowly. Cutting a job hour only moves the denominator, so it moves the ratio faster.

Why Adding Real Estate Hours Barely Moves the Needle

People assume the fix is simply to log more real estate time. The arithmetic shows why that is so inefficient when a full-time job is fixed in place. Suppose your job is locked at 2,080 hours. Watch what each additional 250 real estate hours does to the ratio:

- RE 500: 500 / 2,580 = 19.4%

- RE 750: 750 / 2,830 = 26.5%

- RE 1,000: 1,000 / 3,080 = 32.5%

- RE 1,250: 1,250 / 3,330 = 37.5%

- RE 1,500: 1,500 / 3,580 = 41.9%

- RE 1,750: 1,750 / 3,830 = 45.7%

- RE 2,000: 2,000 / 4,080 = 49.0%

- RE 2,081: 2,081 / 4,161 = 50.01% (finally over the line)

Each 250-hour block of additional real estate work moves the ratio by only about 5 to 7 percentage points, because each of those hours also enlarges the denominator. You have to grind all the way up to 2,081 real estate hours to cross 50% while the job sits at 2,080. The fraction approaches 50% asymptotically until your real estate hours finally exceed your job hours by one.

Mathematically, with a fixed job J, your ratio can never reach 50% until R exceeds J. No amount of partial effort gets you there. It is all-or-nothing against the job's hour count.

Shrinking the Denominator Is Twice as Powerful

Because the job lives only in the denominator, cutting job hours is the single most powerful lever you have. When you remove an hour of employment, you do two things at once: the denominator falls by one, and you free up an hour you can redirect into the numerator. That is why people who succeed at REP almost always change their employment situation, not just their real estate effort.

Adding 1 RE hour

- Numerator: +1

- Denominator: +1

- Net effect on ratio: small

- Requires you to find brand-new time

Moving 1 hour from job to RE

- Numerator: +1

- Denominator: 0 (one leaves job, one enters RE)

- Net effect on ratio: roughly double

- Uses time you already spend working

Reconsider the table. Drop the job from 2,080 hours to 1,000 hours (going part-time, a sabbatical, or leaving mid-year) and suddenly 1,001 real estate hours wins. Drop it to zero and the 50% test becomes trivial; only the 750-hour floor remains. This is the mechanical reason that 'beating' the 50% test is really a conversation about your employment, not about how dedicated a landlord you are.

REP Helper tracks the ratio live. Because it logs your real estate work as it happens AND lets you record your outside/W-2 hours, the 750-hour AND 50% progress bars update together, so you can see in real time whether your denominator is still out-voting your numerator.

What Actually Counts in the Denominator

The denominator is broader than your main job. It is ALL personal-service hours in any trade or business. People underestimate it and then fail the test on hours they never thought to count. The denominator typically includes:

- All W-2 employment hours, including overtime, travel time treated as work, and meaningful on-call work.

- A non-real-estate side business or consulting practice (a software side gig, a freelance design business, a medical practice).

- A second job, seasonal work, or gig-economy work performed as a trade or business.

- Your real estate hours themselves (they are in the numerator AND therefore in the denominator total).

What is generally NOT in the denominator: passive investing where you are not providing services, purely personal activities, sleeping, commuting in most cases, and time that is not personal service in a trade or business. The point is that the denominator captures your WORKING life, and a high-hour profession (think a demanding W-2 plus a side business) can put the bar so high that no realistic amount of real estate work clears it.

A person with a 2,080-hour job AND a 600-hour side consulting business needs more than 2,680 real estate hours to pass. The side business you forgot to count can be the difference between passing and failing.

The Test Is Per Individual: The Spouse Escape Hatch

There is one structural feature of the 50% test that gives full-time earners a way out: the test is applied per individual, not per household. Even on a married-filing-jointly return, each spouse's hours are tallied separately for the 750-hour and 50% tests. The hours are NOT combined for REP qualification purposes.

That cuts both ways. It means you cannot pool a working couple's real estate hours to get one of you over the line, which disappoints many couples. But it also means the spouse with little or no W-2 income has a tiny denominator. If one spouse works full-time and the other does the real estate work, the non-working spouse may pass the 50% test easily, because their denominator is mostly real estate to begin with.

- Spouse A: 2,080-hour W-2 job, 200 RE hours -> RE share well under 50% -> A does not qualify.

- Spouse B: no other job, 800 RE hours -> RE share is 100% of B's working hours, and 800 > 750 floor -> B qualifies.

- If B materially participates in the rentals, the household can use REP based on B's qualification on the joint return.

REP Helper tags every logged activity by who performed it (owner vs spouse vs contractor), so each spouse's separate 750-hour and 50% totals stay clean and you can prove whose hours qualified.

Passing the 50% Test Is Necessary, Not Sufficient

One last guardrail so the mechanism is not oversold. Clearing the 750-hour and 50% tests gets you REP status, but REP status by itself only removes the rule that treats rentals as automatically (per se) passive. It does not, on its own, make your rental losses deductible against your W-2 income.

After you qualify as a REP, you still have to materially participate in the rental activity (under one of the seven tests of the regulations, most commonly the 500-hour test), per property or per group if you make the grouping election. REP and material participation are separate gates. The 50% test decides whether you are a Real Estate Professional; material participation decides whether each activity's losses are non-passive.

REP Helper tracks these as separate ledgers: the 750-hour and 50% progress for REP status, and per-property or grouped material-participation hours for the activity-level test, with CPA-ready exports for each. As always, confirm your specific facts with your tax advisor.

Frequently Asked Questions

Q: If my job is exactly 2,000 hours and my real estate work is exactly 2,000 hours, do I pass the 50% test?

A: No. The test requires MORE than 50%, and 2,000 out of 4,000 is exactly half, which is a tie. A tie fails. You would need at least 2,001 real estate hours so the ratio strictly exceeds 50%. This 'more than, not at least' wording is exactly why one extra hour can matter.

Q: Do my W-2 hours count toward the 750-hour test too, or just the 50% test?

A: Neither test counts W-2 hours in your favor. The 750-hour test only counts real property trade-or-business hours. The 50% test counts your W-2 hours in the denominator (the total), not the numerator. So your job never helps you pass either test; it only raises the bar on the ratio.

Q: Can I add my spouse's real estate hours to mine to get over 50%?

A: No. The 750-hour and 50% tests are applied per individual, even on a joint return, so hours are not pooled across spouses for REP qualification. The practical workaround is the reverse: have the spouse with the smaller (or zero) outside-work denominator be the one who does the real estate work, since they can clear 50% far more easily.

Q: Why does adding 500 more real estate hours barely change my ratio?

A: Because each real estate hour increases BOTH the numerator and the denominator by one. With a fixed full-time job in the denominator, the ratio creeps toward 50% but cannot cross it until your real estate hours actually exceed your non-real-estate hours. Cutting job hours moves the ratio much faster because it only shrinks the denominator.

Q: I cleared the 750-hour and 50% tests. Are my rental losses now deductible against my salary?

A: Not automatically. Passing those two tests gives you REP status, which removes the per-se-passive label on rentals. You must ALSO materially participate in the rental activity (per property, or per group if you make the grouping election) for the losses to be non-passive. Confirm the specifics with your tax advisor.

About the author

Real Estate Investor · Founder, REP Helper

Carlos Lourenço is a real estate investor and the founder of REP Helper. Over 10+ years he's built a portfolio of long- and short-term rentals across several states, personally qualifying for Real Estate Professional Status (REPS) and running the short-term-rental strategy on his own properties. A product manager by trade, he built REP Helper after years of tracking his own hours and IRS tests by hand.

Connect on LinkedInDisclaimer: Carlos Lourenço is a real estate investor, not a CPA, enrolled agent, or tax attorney. This article is for educational purposes only and is not tax, legal, or financial advice. Tax outcomes depend on your specific facts and on current law, which changes. Always consult a qualified CPA or tax attorney before implementing any tax strategy.