The Test Nobody Talks About

The 50% test cost me the most sleep when I was qualifying for REP status, because it’s the one you can fail even with thousands of real estate hours. Let me walk through the numerator and denominator the way I had to learn them.

If there's one rule that quietly disqualifies more real estate investors than any other, it's the 50% test.

Most people focus on the 750-hour rule. They track their rental hours. They feel good about crossing that line.

Then tax season comes.

And the 50% test becomes the problem.

What the 50% Test Actually Says

To qualify as a Real Estate Professional, you must spend more time working in real estate than in all other jobs combined.

That's it.

It's not about income. It's not about which job feels bigger. It's not about which one pays more. It's strictly about hours worked.

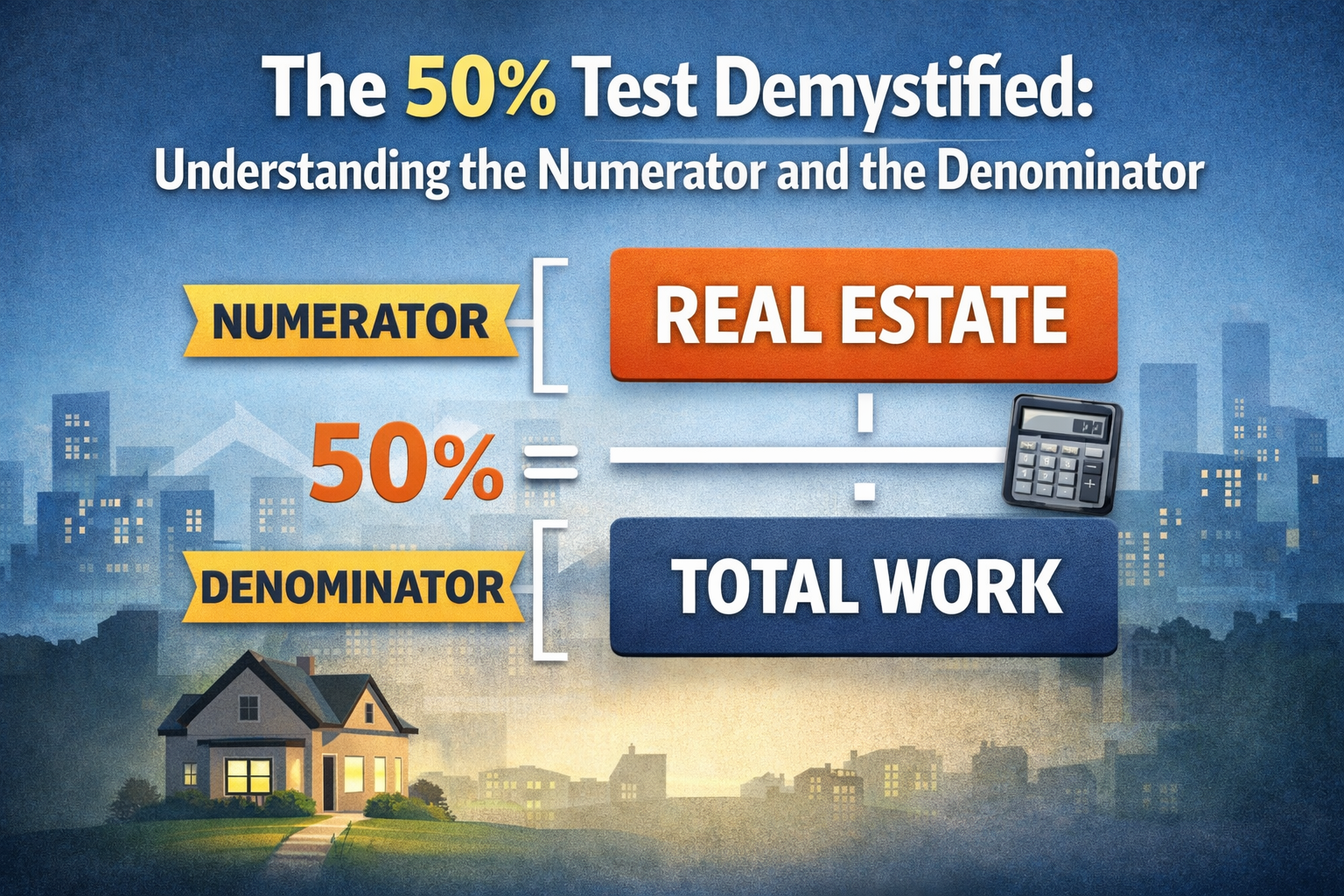

Think of It as a Simple Fraction

Real estate work must be more than half of your total working time. So we're comparing two numbers:

- Numerator: Your real estate hours

- Denominator: Your total working hours (real estate + everything else)

If real estate hours are more than 50% of total work hours, you pass. If not, you fail.

Breaking Down the Numerator

The numerator is the total number of hours you personally spend working in real estate businesses. That can include:

- Managing your rental properties

- Meeting contractors

- Advertising vacancies

- Reviewing leases

- Researching acquisitions

- Overseeing renovations

- Bookkeeping for your rentals

- Property management work

- Real estate brokerage work

The important word here is personally. If your contractor spends 20 hours fixing a roof, that doesn't count. If your property manager handles tenant calls, that doesn't count.

The hours must be legitimate business activities. Casual investment review from your couch doesn't count. You need real, active involvement.

The Denominator: Where It Gets Tricky

The denominator includes all of your working time for the year. Not just your day job. Everything.

This includes:

- W-2 employment

- Consulting work

- Side businesses

- Freelance income

- Any trade or business you actively work in

If you work 40 hours per week at a W-2 job, that's about 2,000 hours per year. Those hours go straight into the denominator. And they raise the bar significantly.

A Real Example

Let's say you spend 900 hours managing your rentals and you work 2,000 hours at your W-2 job.

Total working hours = 2,900. Real estate percentage = 900 ÷ 2,900 = about 31%.

You fail. Even though 900 hours sounds impressive. Even though you passed 750 hours. The denominator killed the qualification.

Why High-Income Earners Struggle With This

An investor with a demanding corporate job logs 800 hours on their rentals. They feel confident. But they worked 2,200 hours at their job.

To pass the 50% test, they would need more than 2,200 real estate hours. That's extremely hard to do while keeping the full-time job.

The rule doesn't care about salary. It only looks at time.

What If You Work Part-Time?

This is where things get interesting.

Suppose: 800 hours in real estate, 600 hours in part-time consulting. Total = 1,400 hours. Real estate is about 57%.

You pass. Same real estate effort. Different denominator. Different outcome.

That's why the denominator matters just as much as the numerator.

What About Spouses?

If you file jointly, your spouse's real estate hours can help you meet the 750-hour rule.

But the 50% test applies individually.

If you personally have a 2,000-hour job, your spouse's rental hours won't reduce your denominator. That's a detail many couples misunderstand.

The Most Common Mistakes

- Ignoring small side work — Investors forget about small consulting projects or business activities. Those hours still count in the denominator.

- Underestimating W-2 hours — Some assume a "40-hour job" is 40 hours flat. In reality, many people work closer to 45–50 hours per week. That adds up fast.

- Tracking only real estate hours — They log rental work carefully but never track other work hours. At year-end, they're guessing. That's dangerous.

Why You Need Real-Time Visibility

You don't want to discover in November that your denominator makes qualification impossible. You want to know in March.

That's where structured tracking becomes critical. Inside REP Helper, the 50% test isn't an afterthought. The system compares your total real estate hours against your non-real-estate working hours. It updates continuously.

If your outside job makes qualification unrealistic, you'll see it early. That allows you to adjust — reduce outside work, increase involvement, or accept that this isn't your qualifying year.

Guessing at this is risky. Seeing the numbers clearly removes the uncertainty.

Documentation Matters

If you ever need to defend your qualification, you'll need:

- Dates

- Descriptions

- Time spent

- Evidence

And you need that for both sides of the equation. You can't just estimate your W-2 hours. You can't just estimate your rental hours.

REP Helper was designed around this reality. It separates real estate work from other working time, and calculates the percentage automatically. You're not left doing math in a spreadsheet.

One Final Thought

The 50% test isn't complicated. It's strict.

Real estate must be the majority of your working life for the year. That's the standard.

Before you plan around large rental losses offsetting W-2 income, run the numbers honestly. If your outside job dominates your time, the denominator will quietly disqualify you.

Track early. Track consistently. Know where you stand. That clarity alone changes how you plan your year.

About the author

Real Estate Investor · Founder, REP Helper

Carlos Lourenço is a real estate investor and the founder of REP Helper. Over 10+ years he's built a portfolio of long- and short-term rentals across several states, personally qualifying for Real Estate Professional Status (REPS) and running the short-term-rental strategy on his own properties. A product manager by trade, he built REP Helper after years of tracking his own hours and IRS tests by hand.

Connect on LinkedInDisclaimer: Carlos Lourenço is a real estate investor, not a CPA, enrolled agent, or tax attorney. This article is for educational purposes only and is not tax, legal, or financial advice. Tax outcomes depend on your specific facts and on current law, which changes. Always consult a qualified CPA or tax attorney before implementing any tax strategy.