Why This Cheat-Sheet Exists

Material participation is the make-or-break gate for nearly every real estate tax strategy, yet the rules are buried in a single dense regulation: Treas. Reg. section 1.469-5T. That regulation lists seven separate tests, and here is the good news most people miss: you only have to pass ONE of them. This page is the fast version. No long examples, no case law, just one line per test and a quick guide to which test fits your situation.

If you want the full deep-dive with worked examples for each test, that lives in our companion article. This is the cheat-sheet you screenshot, pin, or hand to your spouse so you both know which test you are actually trying to satisfy this year. Use it to triage your situation in two minutes, then go log your hours accordingly.

Pass any ONE of the seven tests and your participation in that activity is 'material' for that tax year. You do not need to pass all seven.

First, Don't Confuse This With REP

Before the seven tests matter, clear up the most common mix-up. Real Estate Professional (REP) status and material participation are two different doors, and you usually need to walk through both.

REP Status (the year-level gate)

- More than 750 hours in real property trades or businesses

- More than 50% of ALL your working hours in those trades

- Both in the SAME tax year, measured per individual

- Effect: removes the automatic 'passive' label on your rentals

Material Participation (the activity-level gate)

- Pass ONE of the seven tests below

- Applied per activity (or per group if you elect)

- Effect: makes the losses non-passive so they offset active income

- Required even after you qualify as a REP

REP alone does not let you deduct rental losses against your W-2. REP plus material participation does. The seven tests on this page are about that second gate.

The 7 Tests, One Line Each

Here is the entire regulation, distilled. Read top to bottom and stop at the first one you can pass.

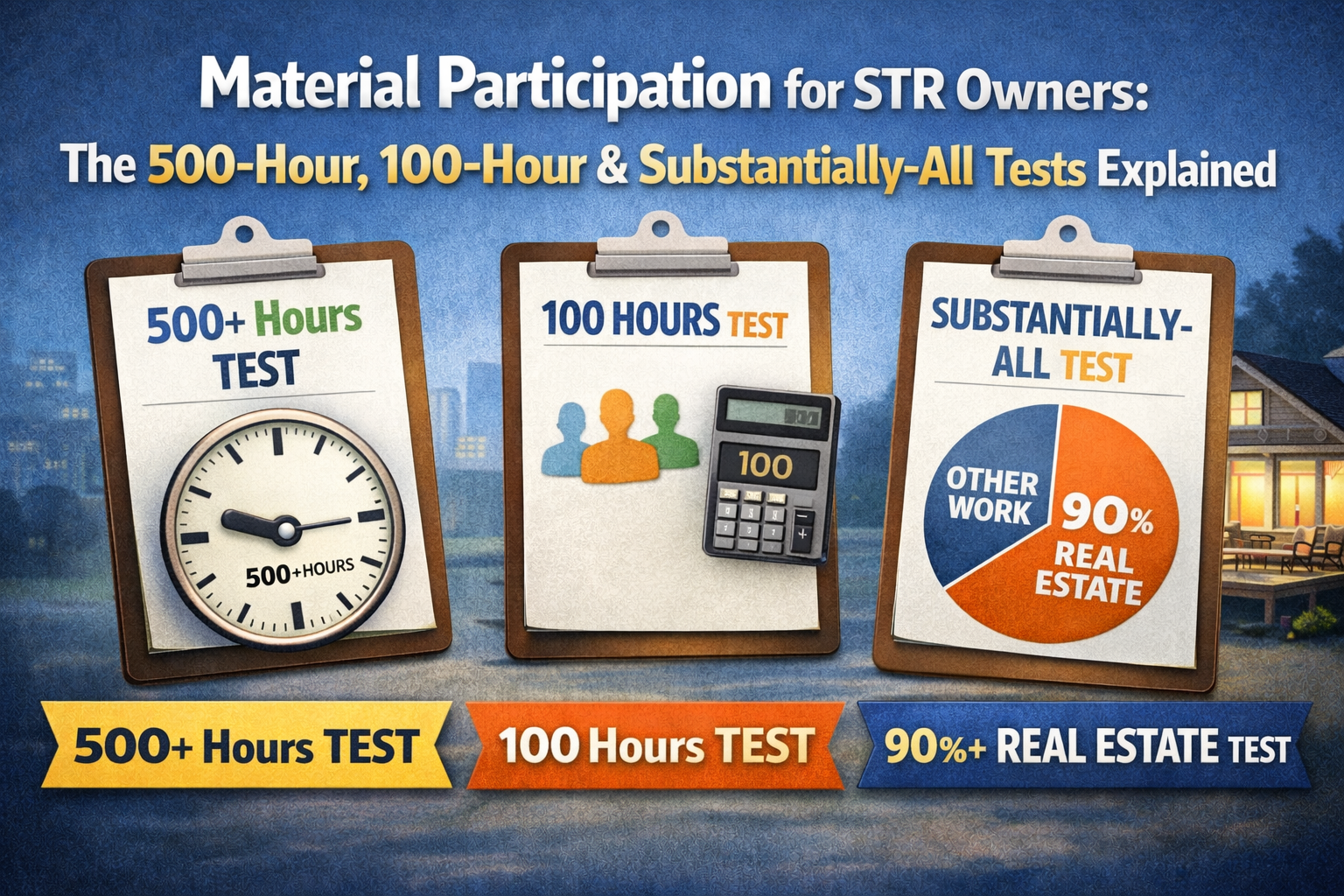

- Test 1 - 500-Hour Test: You participated in the activity for more than 500 hours during the year.

- Test 2 - Substantially All: Your participation was substantially all of the participation by everyone (including non-owners) in the activity.

- Test 3 - 100 Hours and Most of Anyone: You participated more than 100 hours, and no other individual (including paid help) participated more than you.

- Test 4 - Significant Participation Activities (SPA): The activity is a 'significant participation activity' (over 100 hours), and your total hours across ALL such SPAs exceed 500.

- Test 5 - Any 5 of the Last 10 Years: You materially participated in the activity for any 5 of the prior 10 tax years.

- Test 6 - Personal Service Activity, 3 Prior Years: For a personal-service activity, you materially participated for any 3 prior years (rarely applies to rentals).

- Test 7 - Facts and Circumstances: You participated on a regular, continuous, and substantial basis (over 100 hours), based on all facts and circumstances.

Tests 1, 3, 4, and 7 are the ones real estate investors actually use. Tests 5 and 6 are history-based, and Test 2 only works when you do nearly everything yourself.

Quick Decoder: What Each Test Really Means

The one-liners above are the law. Here is the plain-English translation so you know what you are actually counting.

- Test 1: Simplest and strongest. 500 logged hours, full stop. No comparison to anyone else needed.

- Test 2: You ARE the activity. If you (and your spouse) do effectively all the work and no one else touches it, you win even with modest hours.

- Test 3: The 'I do the most' test. You cleared 100 hours and you out-worked every other single person, including any property manager, cleaner, or contractor.

- Test 4: The bundling test. Several activities each over 100 hours but each under 500? Add them up; if the total tops 500, all of them count.

- Test 5: The veteran test. You earned material participation in the past, so it carries forward for a while even in a lighter year.

- Test 6: Aimed at personal-service fields (law, medicine, consulting). Rental owners almost never use it.

- Test 7: The judgment-call test. Weakest and most audit-prone; only viable above 100 hours and disfavored when others are paid to manage.

Which Test Fits Whom

Match your real-world situation to the test most likely to work. Most people land on Test 1, 3, or 4.

Your Situation

- Hands-on owner-operator with real time to give

- DIY landlord, no manager, no crew

- Self-manage but hire occasional help (cleaner, handyman)

- Several smaller rentals, none individually huge

- Used to be very active, lighter year now

- Professional in law/medicine/consulting

- Substantial involvement but hard to hit a bright line

Best-Fit Test

- Test 1 (500 hours)

- Test 2 (substantially all)

- Test 3 (100 hrs and most of anyone)

- Test 4 (significant participation, 500 aggregate)

- Test 5 (5 of last 10 years)

- Test 6 (personal-service, 3 prior years)

- Test 7 (facts and circumstances, 100+ hrs)

If you use a property manager, Tests 2 and 7 get hard fast, because the manager's hours undercut your claim. Aim for Test 1 or Test 3 instead.

Short-Term Rentals: Same Tests, No REP Needed

Short-term rentals deserve a special note because they change the math. If your average guest stay is 7 days or less, the activity is not a 'rental activity' under Reg. section 1.469-1T(e)(3). That means it is not automatically passive, and you do NOT need REP status to make losses non-passive.

- Confirm average guest stay is 7 days or less (compute it from booking data, not gut feel)

- Skip the REP test entirely; it is not required for the 7-day STR

- Still pass ONE of the seven material participation tests, usually Test 1, 3, or 7

- Track your hours separately for each STR unless you group properly

This is why the STR path is popular with busy professionals: it removes the brutal 750-hour and 50% REP hurdles. But it does NOT remove material participation. You still owe the IRS a passing score on one of these seven tests, and for STRs the 100-hour bar (Test 3) is often realistic when you self-manage.

Cheat-Sheet of Mistakes to Avoid

- Assuming REP status is enough. It is not; material participation is a separate test you must also pass.

- Counting investor-type activities. Studying markets, reviewing statements, and 'investor' oversight generally do not count toward your hours.

- Ignoring everyone else's hours. Tests 2, 3, and 7 all compare you to other people; a heavy-hours property manager can sink your claim.

- Forgetting Test 4 aggregation. Don't give up because no single property hits 500; bundle your over-100-hour activities first.

- Leaning on Test 7. The facts-and-circumstances test is the weakest and is unavailable below 100 hours and when management is paid out.

- Reconstructing hours at tax time. A calendar rebuilt in April is far weaker than a contemporaneous log built as the work happened.

Almost every lost case comes down to the same thing: the hours were not credibly documented. The test you pick matters less than the log behind it.

Make the Test You Picked Stick

Every one of the seven tests ultimately turns on hours: how many you worked, and how that compares to everyone else. So once you have picked your target test from the guide above, the job is simply to build a defensible record that proves it.

- Decide your target test before the year starts, so you know what number you are chasing

- Log hours as the work happens, not from memory months later

- Tag each entry by who did the work (owner vs spouse vs contractor) so Tests 2, 3, and 7 are provable

- Tag which test each block of time supports, so Test 4 aggregation is easy at year-end

- Keep a running total against your threshold (100, 500, or your aggregate target)

This is exactly the bookkeeping REP Helper is built for. It captures hours contemporaneously by phone, voice, or web as you work, tags each activity by who performed it and which test it counts toward, and tracks your running totals per property or across a grouped portfolio. For STRs it also computes your average guest stay, so you can confirm the 7-day threshold before you rely on it. When you pick a test from this cheat-sheet, the app keeps the proof building in the background.

Frequently Asked Questions

Q: Do I have to pass all seven material participation tests?

A: No. You pass material participation by satisfying any ONE of the seven tests under Treas. Reg. section 1.469-5T. Most real estate investors rely on the 500-hour test, but the 100-hour-and-most-of-anyone test and the significant-participation aggregation test are common fallbacks.

Q: If I'm a Real Estate Professional, do I still need to pass one of these tests?

A: Yes. REP status only removes the automatic-passive presumption on your rentals. To actually deduct rental losses against active income, you must also materially participate in the activity (per property, or per group if you make the grouping election). REP and material participation are separate gates.

Q: Which test is best if I use a property manager?

A: Aim for the 500-hour test (Test 1), because it does not compare your hours to anyone else's. Tests 2, 3, and 7 all weigh your hours against other participants, so a manager who logs significant time can defeat those claims. The cleaner your bright-line hour count, the stronger your position.

Q: Do short-term rentals use the same seven tests?

A: Yes. If your average guest stay is 7 days or less, the STR is not a 'rental activity,' so REP is not required, but you still must pass one of the same seven material participation tests. For self-managed STRs, the 100-hour test or the 500-hour test are usually the most realistic.

Q: What documentation do these tests require?

A: The regulation allows hours to be established by 'any reasonable means,' but in practice a contemporaneous log naming the date, activity, who performed it, and time spent is far more persuasive than a calendar rebuilt at tax time. Because every test turns on hours, your records are what make the test hold up. As always, run your specific facts by your tax advisor.

About the author

Real Estate Investor · Founder, REP Helper

Carlos Lourenço is a real estate investor and the founder of REP Helper. Over 10+ years he's built a portfolio of long- and short-term rentals across several states, personally qualifying for Real Estate Professional Status (REPS) and running the short-term-rental strategy on his own properties. A product manager by trade, he built REP Helper after years of tracking his own hours and IRS tests by hand.

Connect on LinkedInDisclaimer: Carlos Lourenço is a real estate investor, not a CPA, enrolled agent, or tax attorney. This article is for educational purposes only and is not tax, legal, or financial advice. Tax outcomes depend on your specific facts and on current law, which changes. Always consult a qualified CPA or tax attorney before implementing any tax strategy.