The Strategy for People Who Cannot Quit Their Day Job

If you are a physician, a software engineer, a partner at a firm, or a sales executive pulling sixty-hour weeks, you have probably heard that real estate is the way high earners shelter income from tax. And you have probably also heard the catch: to make rental losses offset your W-2 wages, the advice almost always points to becoming a Real Estate Professional. Then you read what that actually requires and your heart sinks. More than 750 hours in real estate, and more than half of all your working hours in real estate, in the same year. With a career like yours, that math simply does not work.

Here is the good news that rarely gets equal airtime: Real Estate Professional status (you will see it written REP or REPS) is not the only door. For busy professionals there is a quieter, more realistic alternative built around short-term rentals, the Airbnb strategy. It deliberately sidesteps the two REP tests that your schedule makes impossible, and it replaces them with a much lower, time-budget-friendly bar that a working person can genuinely hit on nights and weekends.

This article is about fit, not hype. The question is not whether the STR strategy is glamorous; it is whether it fits a life that already has a full-time job in it. For a large share of high earners, the honest answer is yes, where full REP status is a no.

We will walk through why REP status collides with a demanding career, why the STR path does not, what the lower 100-hour bar actually asks of you week to week, how to budget that time around a real job, and how cost segregation turns a modest time commitment into a meaningful deduction. Treat this as a way to ask your CPA sharper questions about your own situation, not as advice on your specific return.

Why REP Status Collides With a Busy Career

To see why the alternative exists, you have to see precisely where full REP status breaks down for someone with a big job. REP status is earned by a person, in a single tax year, by clearing two hurdles, and both are measured per individual (your spouse cannot lend you hours toward them):

- The 750-hour test: more than 750 hours during the year in real property trades or businesses in which you materially participate.

- The 50% test: more than half of all the personal-service (working) hours you put in across everything you do, in any field, are in real property trades or businesses.

The 750-hour test is hard for a busy professional but not always fatal; it is about fifteen hours a week. The 50% test is the wall. If your W-2 job consumes, say, 2,000 hours a year, then to make real estate more than half of your total working hours you would need to log more than 2,000 hours in real estate on top of that, an essentially full-time second occupation stacked on a career you are not leaving. For most high earners, that is not a stretch goal; it is arithmetic that cannot be satisfied without quitting.

The 50% test is exactly why guru promises of "REPS for busy doctors" so often fall apart in an audit. There is no version of the test that exempts your day job. Your working hours all count in the denominator, and a full-time career almost always tips the ratio against you.

There is one legitimate REP route for households, and it is worth naming so you can rule it in or out: on a joint return, a non-working or part-time spouse may be able to qualify as the Real Estate Professional. But if both spouses work demanding jobs, that door closes too. For the genuinely time-strapped dual-income household, the STR strategy is frequently the only realistic path left, and that is the rest of this article.

How the Airbnb Path Bypasses the REP Tests Entirely

The STR strategy does not help you pass the REP tests. It avoids them. The mechanism is a definitional quirk, not a loophole you have to argue your way into. Under Treasury Regulation Section 1.469-1T(e)(3), an activity is a "rental activity" only if the average period of customer use is more than seven days. If your guests stay, on average, seven days or fewer, your property is not a rental activity for passive-loss purposes at all.

That matters because the rule that makes rentals automatically passive applies to rental activities. Take the property out of the rental-activity bucket and the per-se passive label never attaches. Your STR is treated like any other trade or business, and for any trade or business the passive-versus-non-passive question turns on a single thing: did you materially participate? Notice what is conspicuously absent here. The 750-hour test and the 50% test appear nowhere. They are REP tests, and you are not relying on REP status.

So the busy professional's version of the strategy is two steps, neither of which asks you to dethrone your career:

- Step 1 - Keep the average stay at seven days or fewer. This takes the property out of "rental activity" status and away from the automatic passive label.

- Step 2 - Materially participate in that STR by meeting one of the seven tests of Treasury Regulation Section 1.469-5T. For a self-managing owner with a day job, the 100-hour test is usually the realistic one.

The seven-day average is decided by your actual bookings, so a few longer stays can quietly push you over the line. REP Helper calculates your running average guest stay from booking data as the year unfolds, so you find out in March, not at tax time, that the average is drifting toward eight days.

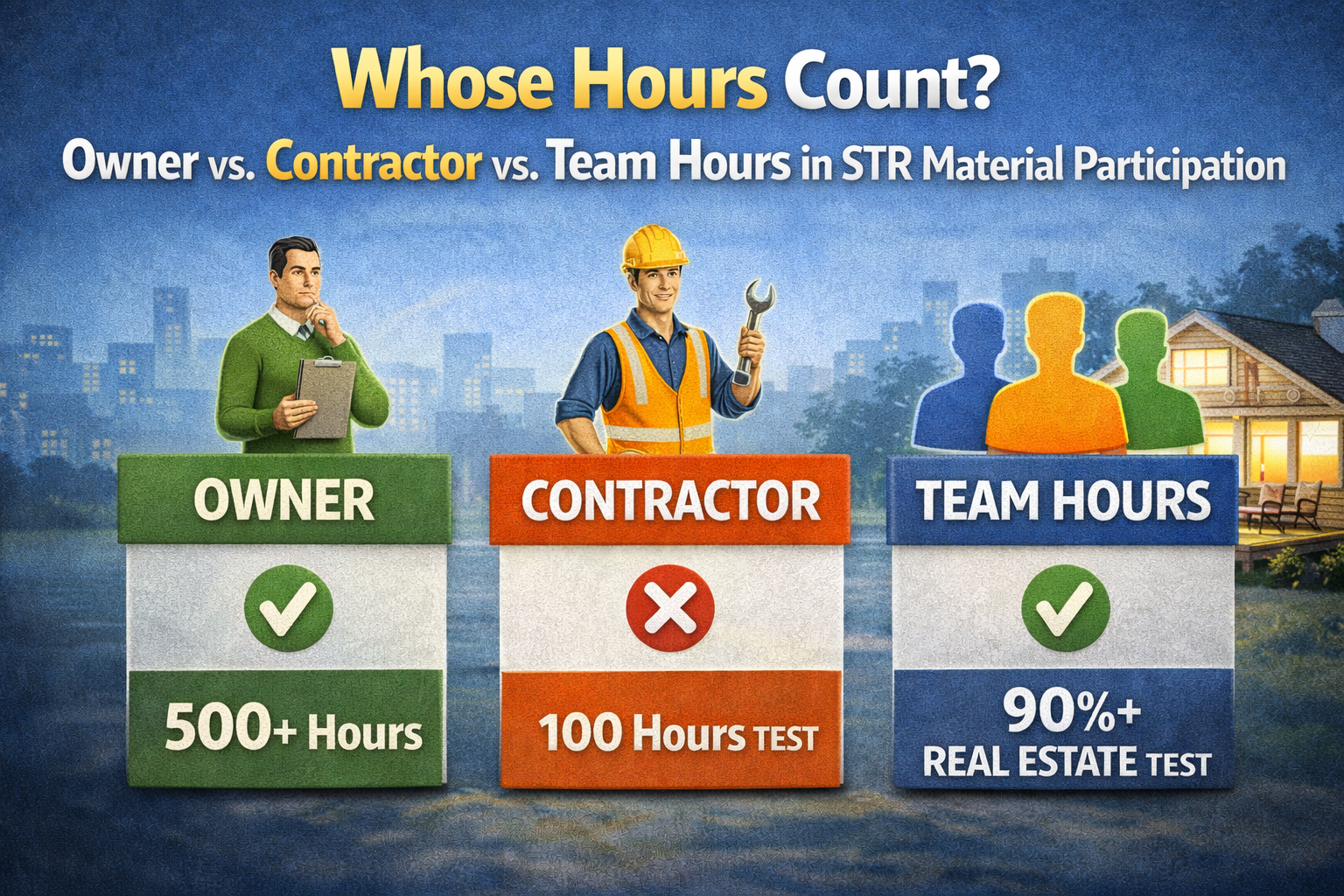

The Lower Bar: The 100-Hour Material-Participation Test

This is the heart of why the Airbnb path fits a busy life. To make your STR losses non-passive you must materially participate, and you get to pick whichever of the seven tests you can meet. The 500-hour test is the famous one, but for a self-managing owner the 100-hour test is usually the door that fits. It has two parts:

- You participated in the activity for more than 100 hours during the tax year, and

- No other individual participated more than you did, including any paid manager, cleaner, or contractor.

Read that second part carefully, because it is the catch that the time-strapped owner must respect. The 100-hour test is not just about your hours; it is about your hours relative to everyone else's. If you hand the property to a full-service property manager who racks up 300 hours, you do not clear it, even if you personally log 150. The strategy rewards owners who self-manage and keep outside help limited, which, conveniently, is also the cheaper way to run a small STR.

Full REP status asks for

- More than 750 hours in real estate (per individual)

- More than 50% of ALL your working hours in real estate

- Plus material participation on top of that

- Re-earned every single year

- Realistically incompatible with a big W-2 job

The STR 100-hour path asks for

- Average guest stay of 7 days or fewer

- More than 100 hours of your own participation

- No one else (manager, cleaner) doing more than you

- No 750-hour or 50% test at all

- Compatible with a demanding full-time career

One hundred-plus hours over an operating year is roughly two focused hours a week, the kind of commitment a working professional can actually fold into evenings and weekends. There are also other tests you might meet, the substantially-all-the-work test if you truly do nearly everything yourself, or the facts-and-circumstances test for owners who do more than 100 hours and participate on a regular, continuous, and substantial basis. But for most busy owners, "more than 100 hours and more than anyone else" is the cleanest target to aim at.

Time-Budgeting It Around a Real Job

Two hours a week sounds easy until you try to prove it. The way busy professionals actually clear the 100-hour bar is not by grinding daily; it is by counting the real, legitimate work of running a short-term rental, work you are already doing, and logging it as it happens. The hours add up faster than people expect once they stop overlooking the small tasks.

Activities that genuinely count toward your participation include guest communication and booking management, coordinating and inspecting turnovers, restocking supplies, handling maintenance and repairs (or supervising them), updating pricing and listings, reviewing reviews and bookkeeping, and the periodic deeper work of furnishing, renovating, or onboarding a new property. A first acquisition year, with its setup and furnishing push, often clears 100 hours almost on its own.

- Block a recurring weekly window (for example, a weekday evening) for guest messaging, pricing, and bookkeeping, and log it every time.

- Capture turnover days: when you inspect a clean, restock, or fix something, that is participation, not a chore to forget.

- Front-load the acquisition year: furnishing, photographing, listing, and onboarding a new STR is participation-heavy, so lean into it.

- Limit how much any single outside person does, so no manager or cleaner out-hours you and breaks the 100-hour test.

- Record the hour the moment it happens, with a date and a short description, rather than reconstructing it in April.

- Track who performed each task (you, your spouse, or a contractor) so you can prove you did more than anyone else.

The whole 100-hour strategy lives or dies on contemporaneous records, and that is precisely the friction REP Helper removes. You log a task by phone, voice, or web the moment it happens, tag who did it, and the record is built as the work occurs, with a CPA-ready export at year end, so you are never guessing whether you crossed 100 hours.

Pairing It With Cost Segregation

Clearing the 100-hour bar makes your STR losses non-passive. Cost segregation is what makes those losses large enough to matter. The two are designed to be used together, and for a busy high earner the combination is the entire point of the exercise.

Normally a building is depreciated slowly over decades. A cost segregation study breaks the property into components, fixtures, flooring, appliances, land improvements, and reclassifies them into much shorter recovery periods. Many of those shorter-lived components are eligible for bonus depreciation, which lets you front-load a large chunk of the deduction into the first year. The result is often a sizable first-year paper loss on a property that is cash-flow positive.

Here is the sequence that makes it work for a W-2 earner. Without the STR strategy, that big depreciation loss would be passive and locked away, useful only against passive income, suspended and carried forward until you sell. Beat the seven-day rule and clear the 100-hour test, and the same loss becomes non-passive, free to offset your salary, bonus, or business income this year. A modest weekly time commitment is the key that unlocks a deduction generated by depreciation, not by hours.

A note on bonus depreciation: the percentage available has been changing year to year, and the rules around cost segregation studies are technical. The illustrative point holds, front-loaded depreciation plus non-passive treatment is the engine, but the exact figures depend on the current law and your property, so this is squarely a conversation to have with your CPA.

The mistake to avoid is buying the cost seg study and forgetting the participation. The study creates the loss; the 100 hours, properly documented, are what let you use it. Skipping the hours, or failing to prove them, turns a powerful strategy into a suspended loss you cannot touch.

Is the Airbnb Alternative Actually for You?

The STR alternative is powerful for the right person and a poor fit for the wrong one. Run your own situation through this quick screen before you commit time or capital.

- You have a demanding full-time career you are not leaving, which rules out full REP status for you personally.

- You own, or are willing to buy, a property suited to nightly or weekly stays where the average can stay at seven days or fewer.

- You are willing to self-manage enough that no manager, cleaner, or contractor out-works you.

- You can realistically protect roughly two focused hours a week for owner tasks across the year.

- You will keep contemporaneous records of hours, who did the work, and average guest stay.

- You have W-2 or active income this year that a depreciation-driven loss could actually offset.

If you checked most of these, the Airbnb path is likely a genuine fit, and a far more realistic one than chasing REP status you cannot earn. If you checked few, be honest with yourself: a property you hand entirely to a manager, or one whose guests stay for months, will not deliver the result no matter how good the cost seg study is. The strategy is not for everyone, and recognizing that early is cheaper than discovering it in an audit.

Because the deciding facts are an average stay, a 100-hour threshold, and who did the work, REP Helper tracks all three in one place, your running average guest stay, your participation hours, and a who-did-it tag on every task, so you can see in real time whether you are on track rather than hoping you are.

Pitfalls That Sink the Busy Owner

The STR alternative fails for predictable reasons, and almost all of them are avoidable with attention up front. These are the ones that catch busy professionals most often, precisely because they are busy.

- Hiring a full-service property manager who out-hours you, which breaks the 100-hour test even when you personally cleared 100 hours.

- Letting the average guest stay creep past seven days through a few monthly bookings, a snowbird tenant, or a long corporate stay, which silently disqualifies the property for the year.

- Buying the cost segregation study but never documenting the participation hours, leaving a large loss suspended and unusable.

- Reconstructing a logbook the weekend before filing; courts give little weight to estimates and round numbers created after the fact.

- Assuming this is REP status by another name and that 100 hours qualifies you as a Real Estate Professional. It does not; this is material participation on a non-rental activity, a separate concept.

- Forgetting that large losses against W-2 income with thin hour logs are a known examination theme, so the records are the defense, not an afterthought.

Notice that every pitfall is either a record-keeping gap or a misunderstanding of which test applies. The busy professional who gets the seven-day average right, keeps the participation in their own hands, and logs the hours as the work happens has neutralized most of the risk before the year even ends.

Frequently Asked Questions

Q: Do I need to become a Real Estate Professional to use the Airbnb strategy as a busy W-2 earner?

A: No, and that is exactly why it suits busy people. Because short-stay rentals (average stay of seven days or fewer) are not treated as rental activities, the per-se passive rule never applies, so you never face the 750-hour or 50% REP tests. You only need to materially participate in the STR, which for a self-managing owner is usually the much lighter 100-hour test.

Q: How many hours does the 100-hour test really require each week?

A: More than 100 hours across the tax year, which works out to roughly two focused hours a week over an operating year, plus the requirement that no one else (such as a property manager or cleaner) participates more than you do. Guest communication, turnovers, restocking, maintenance, pricing, and bookkeeping all count, and an acquisition year with furnishing and setup often clears 100 hours almost by itself.

Q: If I clear the 100-hour test, am I now a Real Estate Professional?

A: No. The 100-hour test is a material-participation test, not the REP qualification, and they are entirely separate. You are not claiming REP status at all under the STR strategy; you are relying on the fact that a short-stay property is not a rental activity, so only material participation matters. Calling yourself a Real Estate Professional based on 100 STR hours would be incorrect and could draw scrutiny.

Q: Can I still use the strategy if I hire a cleaner or a part-time manager?

A: Yes, as long as no single outside individual participates more than you do, because the 100-hour test requires that you do more than anyone else. A cleaner who handles turnovers is fine if your own hours exceed theirs; a full-service manager who runs everything is the problem, since their hours can easily surpass yours. Tracking who performed each task is what lets you prove you stayed on the right side of that line.

Q: Why pair the strategy with cost segregation?

A: Because clearing the 100-hour test only makes the losses non-passive; cost segregation and bonus depreciation are what make those losses large enough to be worth the effort. A cost seg study front-loads depreciation into the early years, and once the activity is non-passive that loss can offset your W-2 wages or business income now instead of being suspended. The current bonus-depreciation percentage and the study itself are technical, so confirm the specifics with your own tax advisor.

About the author

Real Estate Investor · Founder, REP Helper

Carlos Lourenço is a real estate investor and the founder of REP Helper. Over 10+ years he's built a portfolio of long- and short-term rentals across several states, personally qualifying for Real Estate Professional Status (REPS) and running the short-term-rental strategy on his own properties. A product manager by trade, he built REP Helper after years of tracking his own hours and IRS tests by hand.

Connect on LinkedInDisclaimer: Carlos Lourenço is a real estate investor, not a CPA, enrolled agent, or tax attorney. This article is for educational purposes only and is not tax, legal, or financial advice. Tax outcomes depend on your specific facts and on current law, which changes. Always consult a qualified CPA or tax attorney before implementing any tax strategy.