Two Roads to the Same Tax Outcome

Most real estate investors who want their rental losses to offset W-2 wages, business income, or capital gains eventually run into the same wall: the passive activity loss rules of Internal Revenue Code Section 469. By default, rental real estate is passive, and passive losses can only offset passive income. They sit suspended, carried forward year after year, until you finally sell. The frustration of watching paper losses pile up with no tax benefit is what sends people looking for a way out.

There are two well-traveled roads around that wall, and they are frequently confused for one another. The first is the short-term rental (STR) strategy, often nicknamed the Airbnb strategy because it tends to involve nightly or weekly stays. The second is qualifying as a Real Estate Professional, or REP status (you will also see it written REPS). Both can convert rental losses from passive to non-passive. But they get there by entirely different legal mechanisms, they fit entirely different investor profiles, and choosing the wrong one for your situation wastes a year of effort.

This article is a decision framework, not a sales pitch for either route. By the end you should be able to look at your own portfolio, income, and time, and say with confidence which path is realistic and which is a dead end for you.

We will lay out how each strategy actually works, the honest pros and cons of each, a side-by-side comparison, and a chooser that walks through the handful of facts that usually settle the question. A quick note up front: rules in this area are technical and fact-specific, so treat this as a way to ask your CPA sharper questions, not as a substitute for their advice on your return.

How the Airbnb (STR) Strategy Works

The STR strategy is built on a quirk in the regulations, not on REP status at all. Under Treasury Regulation Section 1.469-1T(e)(3), an activity is only a "rental activity" if the average period of customer use is more than seven days. If your average guest stay is seven days or fewer, your property is, for Section 469 purposes, not a rental activity. That single fact is the entire foundation of the strategy.

Why does it matter? Because the rule that makes rentals automatically passive applies to rental activities. Take the property out of the rental-activity bucket and the per-se passive treatment never attaches. The property is treated like any other trade or business. And for any trade or business, the question of passive versus non-passive turns on one thing: did you materially participate?

So the STR strategy is really a two-step test, and notably the 750-hour and 50%-of-working-hours REP tests appear nowhere in it:

- Step 1 - Beat the 7-day rule: Confirm the average guest stay across the year is seven days or fewer (or up to 30 days if you also provide substantial hotel-like services). This takes the property out of "rental activity" status.

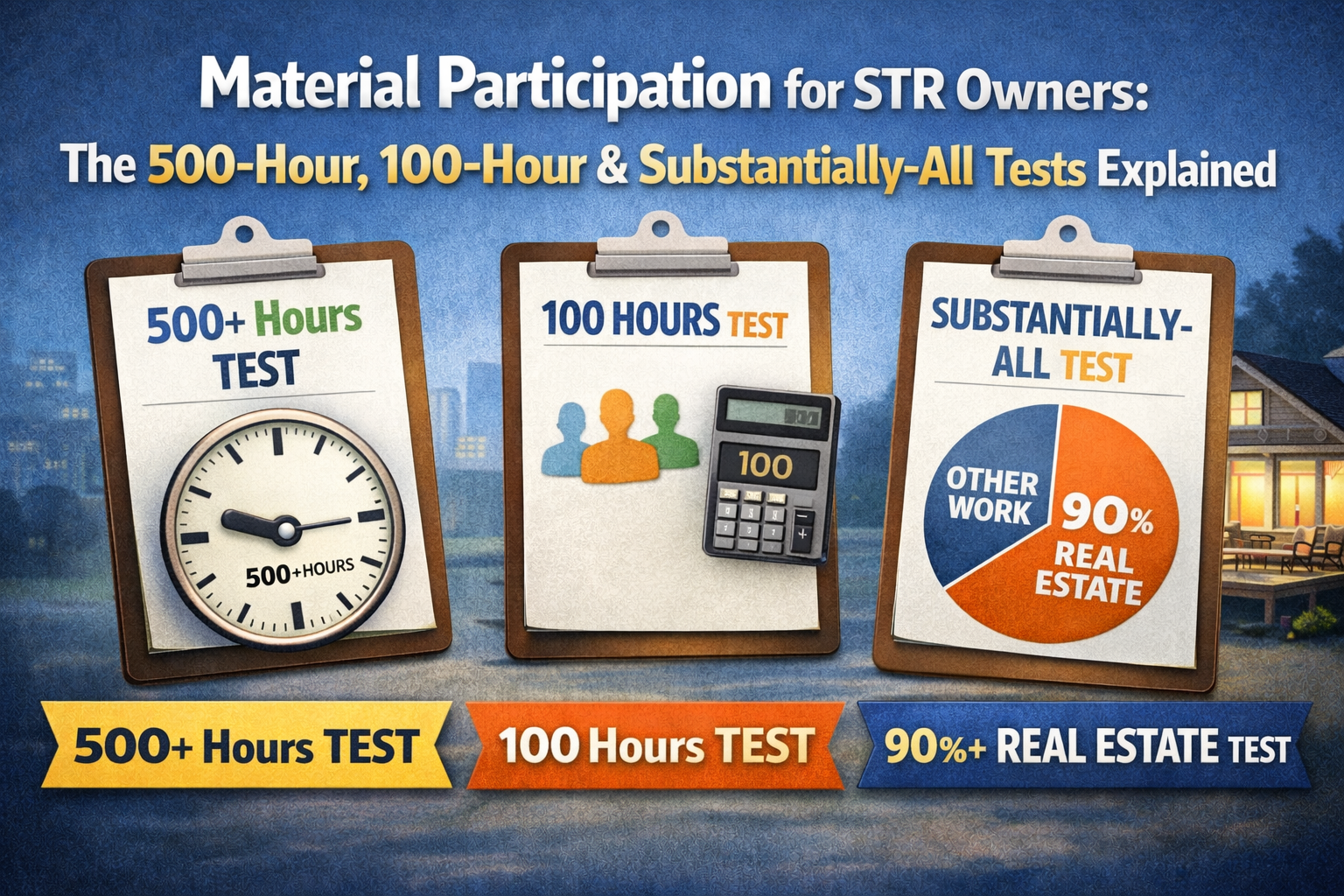

- Step 2 - Materially participate: Meet one of the seven material participation tests of Treasury Regulation Section 1.469-5T for that activity. For most STR owners the realistic ones are the 500-hour test, the 100-hour-and-no-one-else-did-more test, or the substantially-all-the-work test.

Clear both steps and the STR's losses are non-passive. They can offset your wages, your business income, and other active income, with no requirement that you be a Real Estate Professional and no requirement that real estate dominate your working life. That is the strategy's signature advantage: it is open to people who hold demanding full-time jobs in completely unrelated fields.

Because the 7-day question is decided by your actual average stay, the math is unforgiving of guesswork. REP Helper calculates your running average guest stay from booking data as the year unfolds, so a few longer reservations don't quietly push you over the seven-day line without warning.

How Full REP Status Works

Full Real Estate Professional status is a status you earn as a person, not a feature of any one property. To qualify for a tax year you must clear two hurdles in that same year, and both are measured per individual (a spouse cannot lend you their hours toward these two tests):

- The 750-hour test: You spend more than 750 hours during the year in real property trades or businesses in which you materially participate.

- The 50% test: More than half of all the personal-service (working) hours you put in across everything you do, in any field, are in real property trades or businesses.

Here is the step that trips up the most people: REP status by itself does not make your rental losses non-passive. It only removes the rule that makes rentals automatically, per-se passive. After you are a REP, you still have to materially participate in your rental activities, the same seven tests of Section 1.469-5T, for the losses to be non-passive. REP and material participation are two separate gates, and you must walk through both.

There is a powerful companion move here. By default, you must materially participate in each rental property separately, which is brutal if you own many. The grouping election under IRC Section 469(c)(7)(A) and Treasury Regulation Section 1.469-9(g) lets a REP treat the entire rental portfolio as a single activity. Now your hours across all properties combine to meet one 500-hour test instead of property-by-property. The election is filed by a statement attached to the return and is generally irrevocable, so it deserves a deliberate decision rather than a default one.

The 50% test is where careers collide with portfolios. If you work 2,000 hours at a non-real-estate W-2 job, you would need more than 2,000 hours in real estate to put real estate over half your total, an essentially full-time second occupation. This is why full REP status is most realistic for people not working a large W-2, or for a spouse who can dedicate the time.

Side by Side: The Core Differences

The cleanest way to see the choice is to put the mechanics next to each other. Notice that the STR column never mentions 750 hours or the 50% test, while the REP column requires both before material participation even enters the picture.

Airbnb / STR Strategy

- Legal hook: short stays are not a 'rental activity' (7-day rule)

- 750-hour test: not required

- 50%-of-working-hours test: not required

- Still must materially participate (per property)

- Compatible with a demanding full-time job in any field

- Covers only the short-stay properties that meet the rule

- Key risk: average stay creeping above 7 days; thin hour logs

Full REP Status

- Legal hook: you personally qualify as a Real Estate Professional

- 750-hour test: required, per individual

- 50%-of-working-hours test: required, per individual

- Still must materially participate (per property or grouped)

- Hard to clear alongside a large unrelated W-2 job

- Can cover an entire long-term rental portfolio (with grouping)

- Key risk: failing 50% test; weak time logs; spouse-hours confusion

The single most important takeaway from this table: the STR path is narrower in scope but far easier to qualify for if you have a day job, while the REP path is broader in scope but demands that real estate be the majority of your working life. Scope versus accessibility is the central trade.

STR Strategy: Honest Pros and Cons

The STR strategy's biggest selling point is that it sidesteps the two hardest REP tests. A surgeon, a software engineer, or a sales executive working 50 hours a week can still use it, because the 50% test simply does not apply. For high earners with no realistic path to REP status, this is often the only door that opens.

- Pro: No 750-hour or 50% requirement, so it works with a full-time non-real-estate career.

- Pro: The material-participation bar can be relatively reachable; the 100-hour test (you do more than anyone else) is attainable for an owner who self-manages a small STR.

- Pro: Short-term rentals often throw off large first-year losses from bonus depreciation and cost segregation, and those losses are exactly what the strategy frees up.

- Con: Scope is limited to properties whose average stay is seven days or fewer; your long-term rentals get no help from this strategy.

- Con: The 7-day average is fragile. A handful of monthly bookings, a winter snowbird tenant, or a long corporate stay can push the average over seven days and silently disqualify the property for the year.

- Con: If you hire a property manager and a cleaning crew and barely touch the property, you may fail material participation even though you cleared the 7-day rule.

- Con: It is an audit-attention magnet, because large losses against W-2 income with light hour logs are a known examination theme.

The two STR failure modes, blowing the 7-day average and failing material participation, are both record-keeping problems at heart. REP Helper tracks the running average stay from your bookings and logs your participation hours by who did the work (you versus a cleaner or manager), which is precisely the evidence the 100-hour test depends on.

Full REP Status: Honest Pros and Cons

Full REP status is the heavier lift, but it is also the more powerful and durable strategy for the right person. It is not tied to guest-stay length, so it works for traditional long-term rentals, and with the grouping election it can unlock an entire portfolio at once.

- Pro: Covers long-term rentals, not just short stays, so it fits a conventional buy-and-hold portfolio.

- Pro: With the grouping election, hours across all properties combine to satisfy one material-participation test instead of fighting that battle property by property.

- Pro: Once you genuinely live a real-estate-centered working life, it tends to be sustainable year after year.

- Con: The 50% test is the real wall. If you have a substantial W-2 job in another field, it is very hard, often impossible, to make real estate more than half your total working hours.

- Con: It must be re-earned every single year; one busy year at a non-real-estate job can break the chain.

- Con: REP status alone is not enough; you still must materially participate, and people forget this second gate.

- Con: Tax Court has repeatedly disallowed REP claims that rested on estimates, round numbers, and reconstructed logs rather than contemporaneous records.

A common and legitimate variation: if you cannot clear the 50% test because of your own job, your spouse may be able to. On a joint return, if one spouse qualifies as a REP, the rental losses can become non-passive for the couple, provided the couple materially participates. The qualifying spouse's REP tests are still measured on that one spouse individually, but material participation can draw on both spouses' hours.

Because REP requires both a per-individual 750/50% calculation and per-activity (or grouped) material participation, REP Helper tracks your real estate hours and your outside working hours so the 50% ratio updates live, and it tags each logged activity by which test it counts toward and by who performed it.

Which Profile Fits Which Strategy

Strategy choice is rarely a matter of taste. In practice, a few facts about your life decide it. Here are the most common investor profiles and where each one usually lands.

Lean toward the STR strategy if...

- You have a demanding full-time job outside real estate

- You own (or want to buy) properties suited to nightly or weekly stays

- You can plausibly do more of the work than anyone else, or hit 500 hours, on the STR

- You want a tax benefit without quitting your career

- You want first-year depreciation losses to offset W-2 wages

Lean toward full REP status if...

- You or your spouse can make real estate the majority of working hours

- Your portfolio is mostly long-term rentals the 7-day rule cannot help

- You own several properties and want grouping to unlock the whole portfolio

- One spouse can dedicate full-time-ish hours while the other earns the W-2

- You are retired, semi-retired, or self-employed in real estate already

Two profiles deserve special mention. First, the busy high earner with no STR-suitable property and no available spouse: for them, neither path may be realistic this year, and the honest answer is to either acquire a short-stay property or wait for a life change. Second, the investor with a mixed portfolio of long-term rentals and a couple of STRs: they may run the STR strategy on the short-stay properties now while building toward REP status (often via a spouse) to capture the long-term rentals later. These are not always either-or choices.

The Chooser: Walk Through These Questions

Run your own situation through this short sequence. Answer honestly; the wrong honest answer simply tells you to pick the other path or wait, which is far cheaper than discovering it during an audit.

- Do you (or your spouse) have a full-time job outside real estate? If yes, full REP status for that person is likely off the table; look hard at the STR strategy or the other spouse.

- Is the average guest stay on the relevant property seven days or fewer? If yes, the STR strategy is available; if no, it is not, and you need REP status (or to change the rental model).

- On that short-stay property, can you do more work than anyone else, or log 500 hours? If yes, the STR material-participation gate is reachable.

- Is your portfolio mostly long-term rentals? If yes, the STR strategy can't help those, and REP status (with grouping) is the path that covers them.

- Can either spouse make real estate more than half of their total working hours and clear 750 hours? If yes, full REP status is genuinely on the table for the household.

- Are you prepared to keep contemporaneous records of hours, who did the work, and average stay? If no, neither strategy will survive scrutiny, regardless of which you pick.

Notice the last item applies to both paths equally. The strategy you choose changes which numbers you must prove, but not the requirement to prove them with records built as the work happens. REP Helper exists to make that contemporaneous record automatic, via quick phone, voice, or web entries, with CPA-ready exports at year end.

If the chooser points you in two directions at once, that is usually a sign you have a mixed portfolio and may run both strategies in parallel, the STR approach on short-stay properties and REP status on the rest. That is a perfectly normal, and often optimal, outcome.

Mistakes That Sink Either Strategy

The strategies fail for predictable reasons. Most are not about choosing the wrong path; they are about executing the chosen path carelessly.

- Assuming REP status finishes the job. It only removes per-se passive treatment; you still must materially participate. Skipping the second gate is the single most common REP mistake.

- Treating the 7-day rule as a property type rather than a yearly average. A property that averaged five days last year can average nine this year and quietly lose STR treatment.

- Counting a spouse's hours toward the 750-hour and 50% tests. Those two tests are per individual; spouse hours help with material participation, not with REP qualification itself.

- Reconstructing a logbook the night before filing. Courts give little weight to estimates and round numbers created after the fact; contemporaneous beats reconstructed every time.

- Hiring out so much of the work that you fail material participation, then claiming losses anyway. If a manager and crew do most of the work, you may not clear the test.

- Forgetting the grouping election, or making it without realizing it is generally irrevocable.

There is a reason every one of these mistakes traces back to documentation or to a misunderstanding of which test applies. Get the strategy right and the records right, and most of the danger disappears.

Frequently Asked Questions

Q: Do I need to be a Real Estate Professional to use the Airbnb / STR strategy?

A: No, and that is the whole point of the strategy. Because short-stay rentals (average stay of seven days or fewer) are not treated as rental activities under the regulations, the per-se passive rule never applies, so you do not need to clear the 750-hour or 50%-of-working-hours REP tests. You do, however, still have to materially participate in the STR for the losses to be non-passive.

Q: Can I run both the STR strategy and full REP status at the same time?

A: Yes. They are not mutually exclusive. A common setup is to use the STR strategy on short-stay properties while a spouse pursues REP status (with a grouping election) to unlock the long-term rentals. Just keep clear, separate records for each, because the tests you must prove are different for each property.

Q: Which strategy is better if I have a full-time W-2 job in another field?

A: For most full-time employees in non-real-estate jobs, the STR strategy is the realistic option, because the 50% test makes personal REP status nearly impossible when most of your working hours go to your day job. The main alternatives are to have a spouse pursue REP status, or to accept that this may not be your year for either path.

Q: Does REP status by itself make my rental losses non-passive?

A: No. REP status only removes the rule that automatically treats rentals as passive. You still have to materially participate in each rental activity (or in the grouped portfolio if you make the election) under the seven tests of Section 1.469-5T. REP and material participation are two separate gates, and you must clear both.

Q: What records do I actually need to defend either strategy?

A: Contemporaneous records built as the work happens: a log of your hours with dates and descriptions, a note of who performed each task (you, your spouse, or a contractor), and, for STRs, the data behind your average-stay calculation. For REP status you also need a record of your non-real-estate working hours to support the 50% ratio. Tools like REP Helper are designed to capture all of this in real time and export it in a CPA-ready format. As always, confirm the specifics with your own tax advisor.

About the author

Real Estate Investor · Founder, REP Helper

Carlos Lourenço is a real estate investor and the founder of REP Helper. Over 10+ years he's built a portfolio of long- and short-term rentals across several states, personally qualifying for Real Estate Professional Status (REPS) and running the short-term-rental strategy on his own properties. A product manager by trade, he built REP Helper after years of tracking his own hours and IRS tests by hand.

Connect on LinkedInDisclaimer: Carlos Lourenço is a real estate investor, not a CPA, enrolled agent, or tax attorney. This article is for educational purposes only and is not tax, legal, or financial advice. Tax outcomes depend on your specific facts and on current law, which changes. Always consult a qualified CPA or tax attorney before implementing any tax strategy.