The Question Behind the Question

If you have written a check into a real estate syndication or a private real estate fund, you have probably wondered whether the paper losses flowing onto your Schedule K-1 can offset your salary, your consulting income, or your stock gains. The pitch deck may have hinted that bonus depreciation plus Real Estate Professional status equals a tax-free year. The reality for most limited partners is far narrower, and it turns on a specific provision of the passive activity loss rules that has nothing to do with how many hours you work.

This article stays tightly in one lane: what it means to hold an interest as a limited partner under Internal Revenue Code section 469, why that status is presumptively passive, the handful of exceptions that exist, and what all of it implies for someone hoping to claim Real Estate Professional status (REP, often written REPS). We will not re-walk the 750-hour and 50-percent tests in general terms; instead we focus on the unique obstacle the limited-partner rule creates and the precise conditions under which it can be overcome.

The core trap: REP status answers a different question than the limited-partner rule. Earning REP status changes how your rentals are classified, but it does not change the fact that a passive LP interest is still passive. Two separate gates, two separate analyses.

How the Passive Loss Machine Actually Works

Section 469 sorts every activity you are involved in into one of two buckets: passive or non-passive. Losses from passive activities can generally offset only passive income; they cannot reduce your wages, your business income, or your portfolio gains. Anything you cannot use is suspended and carried forward until you have passive income to absorb it or you dispose of the activity in a fully taxable transaction.

An activity is passive if it is a trade or business in which you do not materially participate, or if it is a rental activity. Rental activities carry a per-se-passive label: by default they are treated as passive regardless of how hard you work. There are two principal escape hatches from that per-se label. The first is qualifying as a Real Estate Professional, which lifts the automatic passive treatment from your rentals. The second is the short-term rental rule, where an average guest stay of seven days or less means the activity is not a rental activity at all under Treasury Regulation section 1.469-1T(e)(3).

Both escape hatches share the same catch. Removing the per-se-passive label does not make an activity non-passive on its own. You still have to materially participate in the activity (or in the group, if you make a valid grouping election) before the losses become non-passive and usable against active income. Hold that idea, because the limited-partner rule attacks material participation directly.

The Limited-Partner Presumption Under Section 469

Section 469(h)(2) and the underlying temporary regulations create a special rule for interests held as a limited partner. The general principle is blunt: except as provided in the regulations, no interest in an activity as a limited partner is treated as one in which the taxpayer materially participates. In plain terms, a limited-partner interest is presumptively passive, and the burden is on you to fit into a narrow exception.

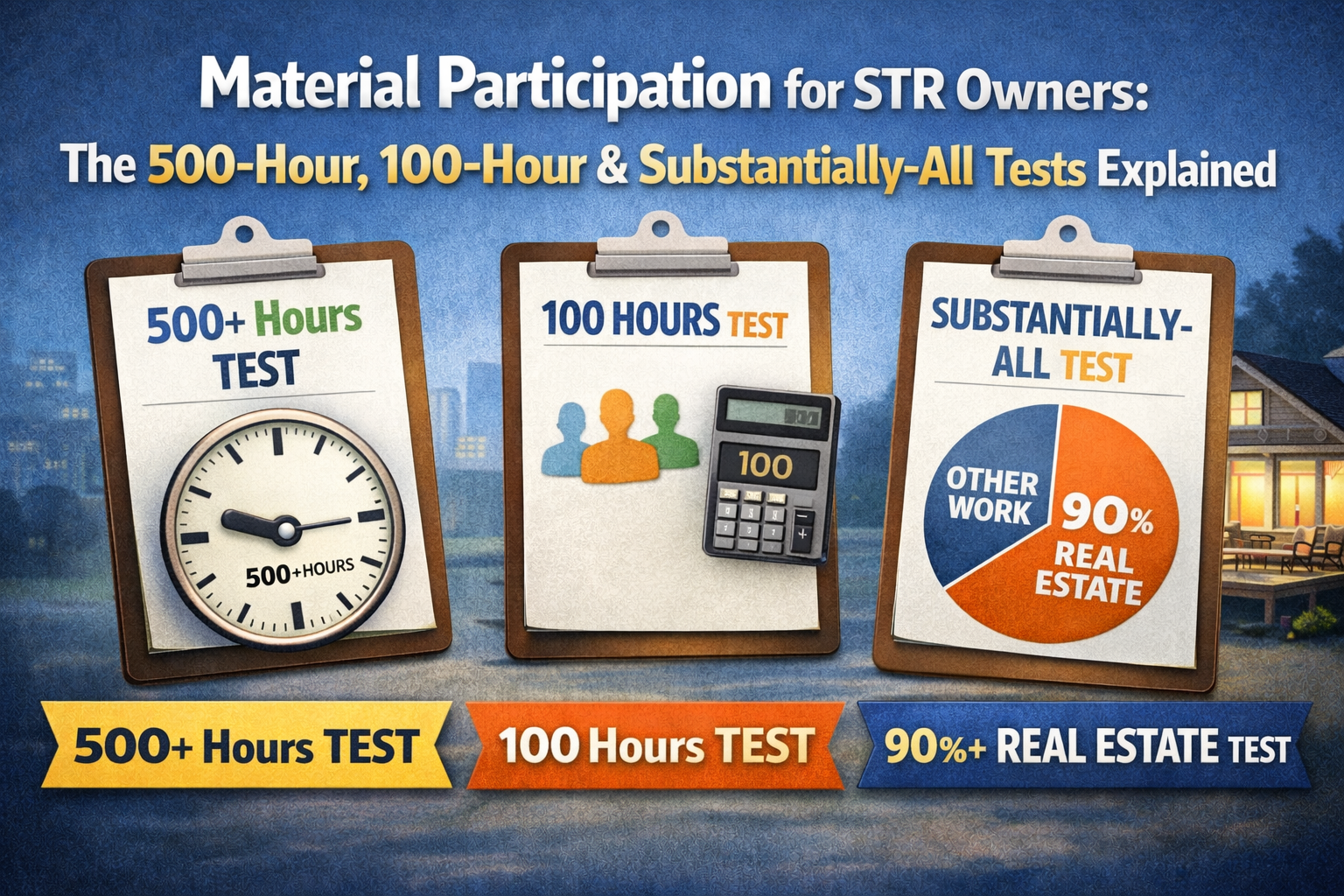

This matters because most of the seven material-participation tests in Treasury Regulation section 1.469-5T are simply unavailable to a limited partner. For an interest held as a limited partner, you can establish material participation through only three of the seven tests, not the full menu. The other four are off the table by regulation. That restriction is the heart of why fund and syndication investors so often come up short.

Available to a limited partner

- Test 1: more than 500 hours of participation in the activity during the year

- Test 5: material participation in any 5 of the prior 10 tax years

- Test 6: a personal-service activity in which you materially participated for any 3 prior years

Closed to a limited partner

- Test 2: substantially all of the participation in the activity

- Test 3: more than 100 hours and not less than anyone else

- Test 4: significant participation activities totaling more than 500 hours

- Test 7: regular, continuous, substantial participation on a facts-and-circumstances basis

Notice what is lost. The 100-hour test and the facts-and-circumstances test, the two tests that let active owners qualify on relatively modest involvement, are exactly the ones a limited partner cannot use. For a true LP, the practical bar becomes 500 documented hours in that specific activity, or a multi-year history of prior material participation in it. For a passive capital investor, neither is realistic.

What Counts as an Interest Held as a Limited Partner

The label that matters is not just what your operating agreement calls you; it is whether the interest functions as a limited-partner interest for these rules. The temporary regulations describe a limited-partner interest as one whose liability for the entity's obligations is limited to a determinable fixed amount, generally the capital you committed. The classic example is a true limited partner in a state-law limited partnership who has no authority to manage and whose downside is capped at the investment.

The harder cases are limited liability companies. An LLC member also enjoys liability protection, which historically led the IRS to argue that LLC interests should be treated as limited-partner interests subject to the restrictive rule. Several courts disagreed, reasoning that an LLC member who actively manages the business is not the kind of passive, capped-liability investor Congress had in mind, and proposed regulations have moved toward a function-over-form approach that looks at whether you have management rights rather than merely whether you have liability protection.

Practical read: a managing member of an LLC who genuinely runs the operation may be able to use all seven material-participation tests, while a non-managing member who simply contributed capital looks much more like a classic limited partner. The precise terms of your interest and your actual role drive the answer. This is a place to confirm the analysis with your tax advisor for your specific entity and state.

There is also a dual-interest concept. If you hold both a limited-partner interest and a general-partner (or active member) interest in the same entity, the regulations can let you treat the activity under the rules for the general-partner portion, which reopens all seven tests. Most syndication LPs do not hold any such active interest; they hold a single passive class of units.

Why REP Status Does Not Rescue a Passive LP Interest

This is the point most investors miss. Real Estate Professional status under section 469(c)(7) requires that more than 750 hours of your personal services during the year, and more than half of all your personal services, be performed in real property trades or businesses in which you materially participate, measured per individual in a single tax year. When you qualify, the per-se-passive label is lifted from your rental activities.

But the REP rule operates on the rental classification, not on the limited-partner presumption. If your only connection to a deal is a passive limited-partner interest, two problems stack up. First, the hours you devote to that interest are essentially zero, because you do not manage the property, so the interest contributes nothing toward your 750 hours or your more-than-50-percent ratio. Second, even after you achieve REP status through other, actively managed properties, the limited-partner interest remains subject to its own presumption and its own restricted set of material-participation tests. REP status does not waive the LP rule.

- Gate one, REP status: removes the per-se-passive label from your rentals based on your total real estate hours across activities you materially participate in.

- Gate two, material participation in the specific LP activity: still required for that activity's losses to be non-passive, and for a limited partner only three tests are available.

- Result: you can be a fully qualified Real Estate Professional and still have a syndication K-1 loss treated as passive because you do not clear 500 hours in that particular deal.

Put differently, REP status is necessary but not sufficient for rental losses generally, and for a limited-partner interest it is largely beside the point. The deciding factor is whether you can satisfy one of the three available material-participation tests in that activity.

The Three Tests Still Open to a Limited Partner

If you are determined to treat a limited-partner interest as non-passive, here is the realistic terrain. Only three of the seven tests apply, and for most investors only one of them is achievable.

Test 1: the 500-hour test

- You participate in the activity for more than 500 hours during the tax year.

- This is the practical path, but it requires genuine, documented work in that specific deal, not capital contribution.

- Investor-type activity such as reviewing reports and monitoring finances generally does not count toward participation.

Tests 5 and 6: the history tests

- Test 5: you materially participated in the activity for any 5 of the prior 10 tax years.

- Test 6: a personal-service activity in which you materially participated for any 3 prior years, which rarely fits a real estate fund.

- Both require a pre-existing record of real participation, so they cannot be conjured for a brand-new passive investment.

For a genuine syndication LP, all three are usually out of reach. You did not work 500 hours on a property a sponsor manages on the other side of the country, and you have no multi-year history of materially participating in it. That is precisely the outcome the rule is designed to produce: capital-only investors are treated as passive.

A note on what counts: time spent in your capacity as an investor, including studying financial statements, monitoring operations from a non-management posture, and preparing summaries for your own use, is specifically not treated as participation under the regulations unless you are directly involved in the day-to-day management or operations. A passive LP almost never is.

Structuring, Recharacterization, and Documentation

There are legitimate situations where an investor is more than a passive LP, and in those cases documentation is what carries the day. If you are a managing member, a co-general-partner, or you hold a dual interest with real management authority, you may have access to all seven tests, and clearing 500 hours, or even the 100-hour test if it applies, can make the activity non-passive. The dividing line is function and form together: what your interest legally is, and what you actually do.

- Confirm the precise legal character of your interest: true limited partner, non-managing LLC member, managing member, general partner, or a dual interest.

- Determine which material-participation tests are available to that interest before counting a single hour.

- If you are relying on the 500-hour test, log contemporaneous, activity-specific hours that reflect genuine management or operations, not investor monitoring.

- Separate the hours for each activity, because material participation is tested activity by activity unless a valid grouping election applies.

- Keep evidence that distinguishes management work from passive oversight, since the regulations exclude investor-capacity time.

- Revisit whether a section 469(c)(7) grouping election helps your actively managed rentals, recognizing that it generally does not pull a passive LP interest into the group.

Contemporaneous records are decisive here because the available tests for a limited-type interest are the hour-counting and history tests, and those are exactly the ones the IRS probes for credibility. Reconstructed estimates and round-number ballparks created at filing time are the classic audit casualty. This is where REP Helper fits the limited-partner problem specifically: it lets you log hours as the work happens by phone, voice, or web, and it keeps each activity separated so you can show genuine 500-hour participation in a deal you actually help run, distinct from the passive interests where you do not.

Tracking That Matches the Tests You Can Actually Use

Because a limited-type interest narrows you to the 500-hour test and the history tests, the quality of your hour log is not a formality; it is the entire case. The two failure modes are counting hours that do not qualify (investor-capacity time) and being unable to prove the hours that do (no contemporaneous record). Both are solvable, but only with discipline maintained throughout the year rather than assembled in April.

- Track participation per activity so a 500-hour claim in a managed deal is never muddled with passive interests.

- Tag each entry by the nature of the work and who performed it, so management hours are clearly separated from non-qualifying investor oversight.

- Keep your overall 750-hour and more-than-50-percent REP picture updating live, including your outside or W-2 hours, so you know whether the REP gate is even in reach before you worry about a specific LP interest.

- Produce CPA-ready exports that show, activity by activity, exactly which test each block of hours is meant to satisfy.

REP Helper is built around exactly this separation. It tracks your 750-hour and 50-percent progress, including non-real-estate work hours so the ratio is honest, while keeping per-activity material-participation records distinct, and it tags each activity by who performed it and which test it counts toward. For an investor sorting active deals from passive LP interests, that per-activity discipline is the difference between a defensible position and a hopeful one.

Frequently Asked Questions

Q: I qualify as a Real Estate Professional. Can I now deduct my syndication K-1 losses against my salary?

A: Not automatically, and usually not at all for a passive limited-partner interest. REP status lifts the per-se-passive label from your rentals, but it does not override the limited-partner presumption. For that specific LP interest you still must satisfy one of the three material-participation tests available to limited partners, which for a true LP typically means 500 documented hours of genuine participation in that deal, something a passive capital investor will not have.

Q: Does holding my interest in an LLC instead of a limited partnership change the answer?

A: It can. Courts and proposed regulations have moved toward looking at whether you have management rights rather than just liability protection. A managing member who actively runs the business may be able to use all seven material-participation tests, while a non-managing member who only contributed capital still looks like a classic limited partner restricted to three tests. The terms of your interest and your actual role control, so confirm the specifics with your tax advisor.

Q: If my LP losses are passive, are they simply lost?

A: No. Disallowed passive losses are suspended and carried forward indefinitely. They can offset passive income in future years, and on a complete taxable disposition of the entire interest to an unrelated party the suspended losses from that activity are generally freed up and become deductible. The benefit is deferred rather than destroyed.

Q: Which material-participation tests can a limited partner actually use?

A: Only three of the seven in Treasury Regulation section 1.469-5T: the more-than-500-hours test, the any-5-of-the-prior-10-years test, and the personal-service-activity-for-3-prior-years test. The 100-hour test, the substantially-all test, the significant-participation test, and the facts-and-circumstances test are not available to an interest held as a limited partner.

Q: Can the short-term rental seven-day rule help a limited partner avoid this?

A: The seven-day rule means a short-stay activity is not a rental activity, so REP status is not required, but it does not change the limited-partner presumption. You still must materially participate, and as a limited partner you are still limited to the three available tests. If you do not run the operation, the seven-day rule does not rescue a passive LP interest.

About the author

Real Estate Investor · Founder, REP Helper

Carlos Lourenço is a real estate investor and the founder of REP Helper. Over 10+ years he's built a portfolio of long- and short-term rentals across several states, personally qualifying for Real Estate Professional Status (REPS) and running the short-term-rental strategy on his own properties. A product manager by trade, he built REP Helper after years of tracking his own hours and IRS tests by hand.

Connect on LinkedInDisclaimer: Carlos Lourenço is a real estate investor, not a CPA, enrolled agent, or tax attorney. This article is for educational purposes only and is not tax, legal, or financial advice. Tax outcomes depend on your specific facts and on current law, which changes. Always consult a qualified CPA or tax attorney before implementing any tax strategy.