The December Deadline Nobody Warns You About

Every year, the same scene plays out. An investor finds the right short-term rental in October, plans to use a cost segregation study to accelerate depreciation, and expects a large paper loss to offset W-2 or business income for the current year. Then the closing slips. The seller asks for an extension. The furniture is backordered. The listing does not go live until January 3rd. And just like that, the entire deduction the investor was counting on has quietly rolled into next year's return.

The short-term rental (STR) strategy is powerful precisely because it can produce non-passive losses without Real Estate Professional (REP) status, provided your average guest stay is seven days or fewer and you materially participate. But the strategy is also unforgiving about timing. The tax code does not care when you signed the purchase contract or when you wired the down payment. It cares about one thing for depreciation: the date the property was placed in service. Get that date in this year, and the write-off lands on this year's return. Miss it by a day, and you wait twelve months.

This article stays in one lane: year-end timing. We are not re-explaining the seven-day rule or the cost segregation mechanics here; we are explaining exactly what has to happen, and by when, so the depreciation you planned for actually lands in the tax year you wanted it.

If you are reading this in the fourth quarter with a deal in motion, treat the rest of this piece as a checklist for protecting your deduction before the ball drops.

What "Placed in Service" Actually Means

Depreciation begins when an asset is placed in service, not when you buy it and not when you close. For real estate, placed in service means the property is ready and available for its intended use. For a short-term rental, that means the unit is furnished, functional, cleaned, and genuinely listed and available to accept bookings, not still mid-renovation with no listing live.

This distinction trips up more investors than almost any other timing issue. Closing in November feels like the finish line, but if the property sat empty and unlisted through December because you were still installing appliances and staging bedrooms, it may not have been placed in service that year. The IRS looks at whether the property was actually ready and held out for rent, not merely owned.

Does NOT place it in service

- Closing on the purchase

- Wiring the down payment

- Owning the deed

- Buying furniture still in boxes

- Planning to list "soon"

- Mid-renovation with no live listing

DOES place it in service

- Furnished and functional unit

- Cleaned and guest-ready

- Listing live and accepting dates

- Available to rent to the public

- Calendar open for bookings

- Ready for its intended use

You do not need a paying guest to have walked through the door by December 31. Available and ready is the standard, not occupied. A property genuinely listed and bookable on December 28, with an open calendar, is generally placed in service even if the first reservation does not arrive until January. But a property that was not listed, not furnished, and not bookable has not been placed in service, no matter when you closed.

Why the Calendar Date Controls Your Deduction

Depreciation is an annual deduction tied to the year an asset is placed in service. A cost segregation study reclassifies parts of your building into shorter-life categories (5-, 7-, and 15-year property) instead of the standard 27.5- or 39-year schedule. Those shorter-life assets, generally those with a recovery period of 20 years or less, can qualify for bonus depreciation, which lets you deduct a large share of their cost in the very first year they are placed in service.

Here is the catch that makes the December 31 date so important: bonus depreciation is a first-year deduction. It belongs to the tax year the asset was placed in service. Under the 2025 One Big Beautiful Bill Act (OBBBA), 100 percent bonus depreciation was restored for qualified property acquired and placed in service after January 19, 2025. That means an investor who gets a property placed in service this year can potentially deduct a very large portion of the cost-segregated components this year. Slip the placed-in-service date into next year, and that same first-year deduction simply moves to next year's return.

The deduction is not lost forever if you miss December 31. It moves. The pain is in the timing: the loss you were planning to use against this year's income is now stranded until you file next year, which can be a meaningful cash-flow and tax-planning difference.

For an investor who had a high-income year, a bonus, a business sale, or a large capital gain to offset, that twelve-month slip can be the difference between neutralizing this year's tax bill and writing a large check now while waiting a year for relief. The amounts are illustrative and depend entirely on your facts, but the lesson is universal: the placed-in-service date is the lever.

Timing Does Not Save a Property That Fails the Seven-Day Test

Before you sprint to place a property in service by December 31, remember that timing only matters if the underlying strategy works. The STR loophole depends on your average guest stay being seven days or fewer, which removes the activity from the definition of a rental activity under the passive activity rules. If your average stay creeps above seven days, the property is treated as a regular rental and the non-passive treatment you were chasing disappears, regardless of when it was placed in service.

Average stay is computed per property for the year: total rental nights divided by the number of separate reservations. A property placed in service late in December has very few reservations to average, which is usually fine, but it underscores why you should be tracking this number from the first booking, not reconstructing it at tax time.

This is one of the points where REP Helper earns its place in the workflow. It calculates your average stay per property directly from your bookings, so you know whether you are under the seven-day threshold long before your CPA asks. Year-end timing is wasted effort if the property quietly fails the average-stay test, and the only way to know is to measure it.

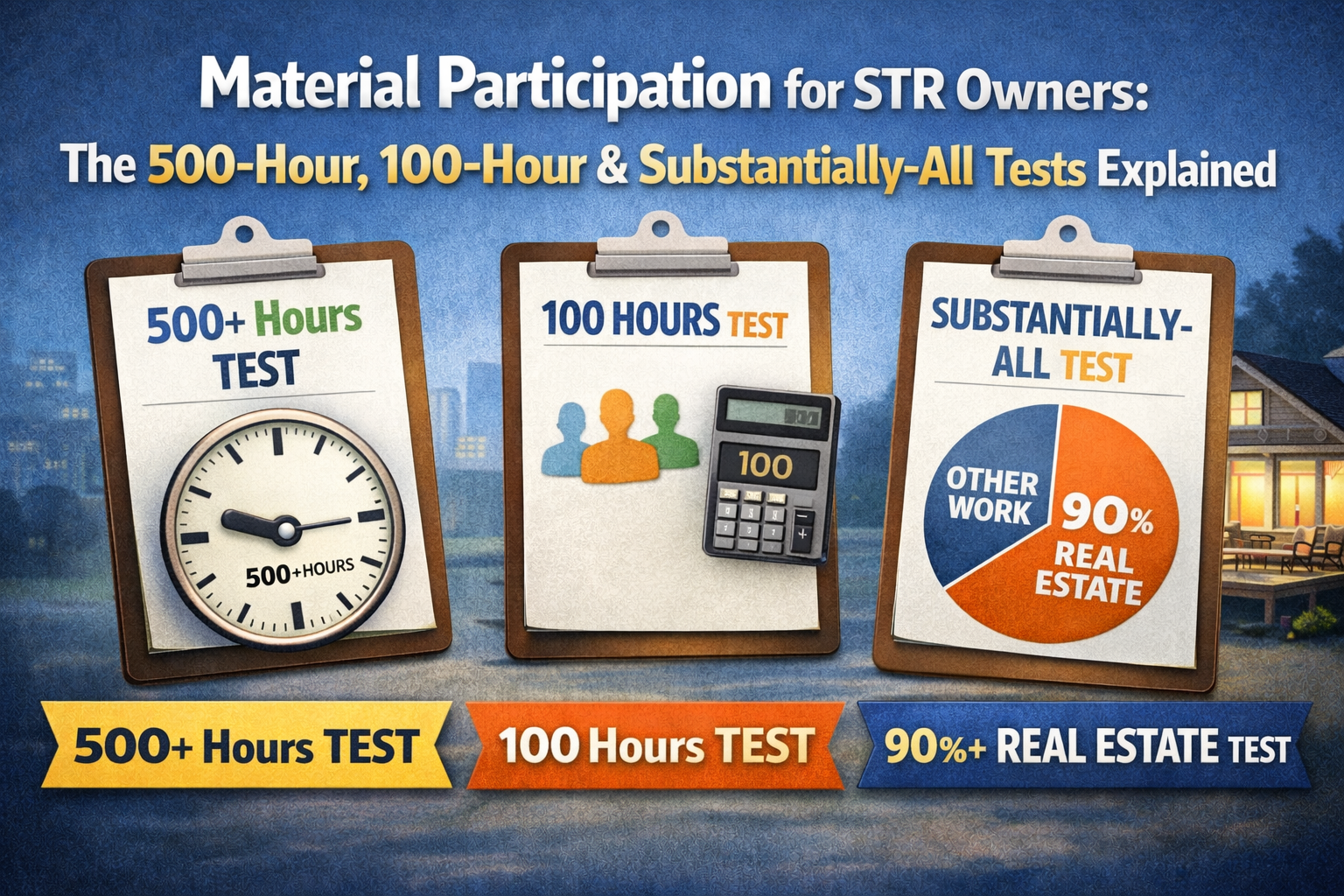

Your Material Participation Clock Resets Every January 1

Getting the property placed in service is half the year-end picture. The other half is material participation, because clearing the seven-day average only removes the automatic passive label. To actually use the loss against W-2 or active income, you must materially participate in the activity, and material participation is measured per calendar year.

The most common tests for short-term rental owners are: more than 500 hours in the activity; or more than 100 hours where no single other person (cleaner, co-host, or property manager) participates more than you; or doing substantially all of the work yourself. Hours you log this year count toward this year's test. Hours you log in January count toward next year. They do not carry backward.

If you place a property in service on December 28, you have only a few days left in the year to accrue this year's material participation hours. With so little time, the substantially-all test or the 100-hour test (where you out-participate everyone else) is often more realistic than the 500-hour test for the stub period, but the facts have to genuinely support it.

This creates a subtle trap. An investor races to list the property by December 31 to capture the placed-in-service date, then outsources every task to a cleaner and a co-host. If those contractors collectively do more of the work than the owner in the few remaining days, the 100-hour test can fail, because contractor and employee hours do not count as the owner's hours and can actually defeat that test. Placing the property in service is necessary, but it is not sufficient; you still have to show you participated.

REP Helper is built for exactly this pressure point. It logs your participation hours contemporaneously by phone, voice, or web, and it tags each activity by who performed it, owner, spouse, cleaner, co-host, or property manager, so you can demonstrate that you out-participated everyone else when you lean on the 100-hour test. It also tracks your progress toward the specific test you have chosen, which matters most in a compressed end-of-year window.

Anatomy of the End-of-Year Scramble

The fourth-quarter rush is predictable, which is exactly why it is avoidable. The deductions are large enough that investors push to close before year-end, and the same bottlenecks show up every December. Knowing them in advance is how you keep your placed-in-service date from slipping.

- Closing delays: lenders, appraisals, and title work all slow down at year-end, and a single extension can push your closing past December 31.

- Furnishing lead times: furniture, mattresses, and kitchenware ordered in mid-December may not arrive until January, leaving the unit not ready and available.

- Listing lag: a property is not placed in service until it is genuinely listed and bookable, so a finished unit with no live listing still does not count.

- Renovation overruns: a property mid-rehab with no live listing is generally not placed in service, no matter when you closed.

- Cost segregation scheduling: the study itself can be completed after year-end, but the property still has to be placed in service by December 31 to claim the first-year deduction this year.

- Material participation crunch: a late-December placed-in-service date leaves almost no runway to accrue this year's participation hours.

Notice that most of these bottlenecks are logistical, not legal. They are within your control if you start early. The investor who lines up financing, orders furniture, and prepares the listing before the closing date is the one who can flip the property to placed in service within days of getting the keys. The investor who waits until after closing to think about furniture and listings is the one writing next year a much bigger check this year.

Is a Rushed December Closing Worth It?

Closing in December to capture a current-year deduction can be smart, but it is not automatically the right move. The placed-in-service date is the goal, and a December closing only helps if you can actually get the property ready, listed, and available before the year ends. If you cannot, you may be better off closing cleanly in early January and treating the deduction as a next-year benefit you can plan around properly.

A December push makes sense when

- You have high current-year income to offset

- Financing and title are on track to close in time

- Furniture is ordered or already on site

- You can realistically list and go live by December 31

- You have days to log meaningful participation hours

- Your average-stay plan keeps you under seven days

Slowing to January may be smarter when

- The closing keeps slipping past mid-December

- The unit needs weeks of renovation first

- Furniture cannot arrive before year-end

- You cannot get a live listing up in time

- Next year is your higher-income year anyway

- Rushing risks a sloppy, unprovable file

There is no prize for forcing a deduction into a year you cannot defend. A clean January placed-in-service date with strong documentation usually beats a contested December one where the property was never truly ready. As always, run the specific facts and numbers past a qualified tax advisor and your cost segregation provider before you decide which year to target.

Your Year-End Placed-in-Service Checklist

If you are aiming to place a short-term rental in service by December 31, work backward from that date. Use this checklist to make sure the placed-in-service standard, the average-stay strategy, and the material participation requirement all line up before the year closes.

- Confirm a closing date with enough runway to furnish and list before December 31.

- Order furniture and essentials early so the unit can be fully ready, not waiting on backordered deliveries.

- Complete cleaning and staging so the property is genuinely guest-ready, not a partial setup.

- Get a live listing published with an open calendar so the property is available and bookable.

- Document the placed-in-service date with dated photos, the live listing, and the open booking calendar.

- Engage your cost segregation provider so the study can support this year's placed-in-service assets.

- Pick a realistic material participation test for the stub period and start logging hours immediately.

- Tag every task by who performed it so contractor hours do not quietly defeat your 100-hour test.

- Track your average stay from the first reservation to confirm you stay at seven days or fewer.

- Review the whole plan with a qualified tax advisor before forcing a current-year deduction.

The placed-in-service evidence is the part most investors neglect under deadline pressure. REP Helper keeps your placed-in-service date and supporting evidence together, alongside your average-stay and material participation records, and produces CPA-ready documentation so the deduction you raced to capture can actually survive a closer look.

Frequently Asked Questions

Q: If I close on December 30 but no guest stays until January, can I still claim depreciation this year?

A: Potentially yes. The standard is placed in service, which means the property is ready and available for rent, not occupied. If the unit was furnished, cleaned, and genuinely listed with an open calendar before December 31, it can be considered placed in service that year even though the first reservation arrives in January. Document that ready-and-available status with dated photos and the live listing, and confirm the result with your tax advisor.

Q: Does the cost segregation study itself have to be finished by December 31?

A: No. The property must be placed in service by December 31, but the cost segregation study can be completed later, even after you start preparing the return. The study identifies and documents the short-life assets; the placed-in-service date is what determines the tax year in which you claim the first-year and bonus depreciation on those assets.

Q: I placed my STR in service on December 28. Is it realistic to meet material participation in just a few days?

A: It can be, but only if the facts support it. With a short stub period, the substantially-all test or the 100-hour test where you out-participate everyone else is usually more achievable than 500 hours. The danger is outsourcing the setup to cleaners and co-hosts whose hours can exceed yours and defeat the 100-hour test. Log your own hours contemporaneously and tag who did what so you can prove you participated more than anyone else.

Q: Do material participation hours I log in early January count toward last year?

A: No. Material participation is measured per calendar year. Hours worked in January count toward the new year's test, not the prior year's. This is why a late-December placed-in-service date is risky: you have very little time left to accrue qualifying hours for the year you want the deduction in.

Q: If I miss December 31, do I lose the deduction entirely?

A: No, you do not lose it; it shifts. The depreciation and bonus depreciation simply land in the next tax year, when the property is placed in service. The real cost is timing and cash flow, because the loss you wanted against this year's income is now stranded until you file next year. If this year was your high-income year, that delay can be expensive even though no deduction disappears.

About the author

Real Estate Investor · Founder, REP Helper

Carlos Lourenço is a real estate investor and the founder of REP Helper. Over 10+ years he's built a portfolio of long- and short-term rentals across several states, personally qualifying for Real Estate Professional Status (REPS) and running the short-term-rental strategy on his own properties. A product manager by trade, he built REP Helper after years of tracking his own hours and IRS tests by hand.

Connect on LinkedInDisclaimer: Carlos Lourenço is a real estate investor, not a CPA, enrolled agent, or tax attorney. This article is for educational purposes only and is not tax, legal, or financial advice. Tax outcomes depend on your specific facts and on current law, which changes. Always consult a qualified CPA or tax attorney before implementing any tax strategy.