The Question Every STR Owner Eventually Asks

Once a short-term rental owner learns what cost segregation can do, the next thought is almost always the same: a study costs real money, the property is depreciating either way, so why not just do the allocation myself? You can punch some numbers into an online calculator, split the purchase price into a few buckets, and claim a big first-year depreciation deduction. On the surface it looks like the same outcome for a fraction of the cost.

It is a fair question, and the answer is not a flat no. You are legally allowed to determine your own depreciation classifications. The IRS does not require you to hire anyone. But "allowed to" and "will hold up" are two different things. The real question is not whether you can do your own cost segregation, but whether the support behind your number is strong enough to survive scrutiny, and whether the size of the deduction justifies skipping the protection an engineered study buys you.

This article stays in one lane: DIY versus engineered cost segregation. What a study actually is, the difference between an online estimate and an engineered report, what the IRS expects for support, the audit risk of an unsupported allocation, and when the property's size and value justify paying a professional.

We will keep the figures illustrative and the tone honest. Cost segregation is genuinely powerful, but it is also one of the more technical depreciation areas, so treat this as a way to ask your CPA and a cost-seg firm sharper questions, not as a substitute for their advice on your specific property.

What a Cost-Segregation Study Actually Is

When you buy a building, the default rule is that you depreciate the whole structure over a long life: 27.5 years for residential rental property and 39 years for nonresidential property. That is slow. A cost-segregation study breaks the building back into its parts and recognizes that many of those parts are not really "the building" for depreciation purposes at all.

Carpet, cabinetry, specialty plumbing and electrical that serve specific equipment, decorative lighting, and removable fixtures are personal property that belongs in a 5- or 7-year MACRS class. Land improvements like driveways, patios, landscaping, and fencing belong in a 15-year class. Only the true structural shell stays on the 27.5- or 39-year schedule. Moving those components into shorter recovery periods is what accelerates your depreciation, and because everything with a recovery period of 20 years or less is eligible for bonus depreciation, those reclassified assets can often be written off in the first year.

So a study is two things at once. It is a calculation that produces a number, and it is a body of evidence that explains how the number was reached. The calculation part is easy to imagine doing yourself. The evidence part is where DIY and engineered approaches diverge sharply, because the IRS cares far more about how you allocated than about the allocation looking reasonable at a glance.

A cost-seg study is not a tax shelter you bolt on. It is just depreciation done with precision. Nothing about it changes how much you spent on the property; it only changes the timing of when you recover that cost. That timing shift is the whole benefit, and the whole audit exposure.

DIY Estimate vs. Engineered Study: The Real Difference

The word "study" gets stretched to cover wildly different things. On one end is a free online calculator that asks for your purchase price, property type, and a few details, then spits out estimated percentages for each asset class. On the other end is an engineered study where a specialist reviews construction documents, inspects the property, identifies and measures actual components, and prices them using recognized cost-estimating methods. Both can hand you a first-year deduction. Only one of them hands you the support that deduction needs.

DIY / Online Estimate

- Based on broad rule-of-thumb percentages, not your actual components

- No site inspection, no measurement, no construction-record review

- Cheap or free, fast, and entirely in your control

- Produces a number but little defensible methodology behind it

- Best as a rough screen to see if a real study is worth pursuing

Engineered Study

- Built from actual identified, measured, and priced components

- Includes site work, photos, and a documented methodology

- Costs real money (often a few thousand dollars and up)

- Produces a report designed to be handed to an examiner

- The standard the IRS guidance points to for reliability

The crucial point is that the IRS does not weigh your deduction by how big it is; it weighs it by how well you can prove it. Two owners can claim the identical reallocation on identical buildings. The one with an engineered report explaining each component is in a strong position. The one whose only support is "the online tool said 25 percent was 5-year property" is exposed, because there is nothing tying that 25 percent to anything real about the building.

There is also a middle ground worth knowing about: a so-called desktop or modeling study, performed by a professional but without a full on-site inspection. It uses real cost data and a documented method but relies on photos, plans, and remote analysis rather than a physical walk-through. For a smaller, simpler property this can be a reasonable, lower-cost compromise that is still far more defensible than a free calculator.

What the IRS Expects for Support

The IRS has actually written down what it looks for. Its Cost Segregation Audit Techniques Guide describes the elements of what it calls a quality study, and it is the closest thing to a rulebook on this topic. While the guide does not legally mandate any single format, it tells examiners what a credible study looks like, which means it effectively tells you what your support should contain.

- A clear methodology that explains how costs were identified and assigned to each asset class, not just the final percentages.

- Identification of the specific assets being reclassified, tied to the actual building, ideally with photographs and descriptions.

- A reconciliation back to the total cost or purchase basis, so every dollar is accounted for and nothing is double-counted.

- Documentation of the source data, such as construction records, invoices, blueprints, or recognized cost-estimating references.

- Preparation by someone with the expertise in both construction and tax law to defend the classifications, which the guide expressly values.

Notice what is missing from a typical DIY estimate against that list. An online calculator gives you percentages but no asset identification, no reconciliation tied to your building, no source documents, and no methodology you could explain under questioning. It is not that the number is necessarily wrong; it is that you cannot show your work, and showing your work is precisely what the guide asks for.

Think of it like a math test where partial credit depends on the steps. The IRS is far more comfortable with a defensible method that produces a slightly conservative number than with an aggressive number that appears from nowhere. Methodology is the currency.

The Audit Risk of an Unsupported Allocation

Here is the uncomfortable part of the DIY path. A large first-year depreciation deduction is, by its nature, noticeable. Reclassifying a big chunk of a building into 5- and 15-year property and then layering bonus depreciation on top can turn a property into a sizeable paper loss in year one. That loss is exactly what makes the strategy attractive, and it is also exactly what can draw a second look.

If that second look comes and your only support is a screenshot from a free calculator, the examiner is not obligated to accept your percentages. They can disallow the accelerated portion, push those costs back onto the long 27.5- or 39-year schedule, and recompute your depreciation. The result can be a chain reaction: the disallowance can wipe out the loss you used to offset other income, and underpayment interest and potentially accuracy-related penalties can follow. None of these outcomes are guaranteed, but the exposure is real and it scales with the size of the deduction.

- Disallowance of the accelerated classifications, reverting components to the long building life.

- Recapture-style consequences and a recomputed depreciation schedule going forward.

- Loss of the first-year loss you relied on to offset W-2 or business income for that year.

- Interest on the resulting underpayment, and potentially accuracy-related penalties.

- Time, stress, and professional fees defending a position you could have documented up front.

An engineered report does not make you audit-proof; nothing does. What it does is shift the conversation. Instead of being asked to justify a number you cannot trace, you hand over a document that already answers the examiner's questions. The cost of the study, in that light, is partly the price of buying that better starting position.

When DIY Can Be Reasonable

None of this means DIY is always the wrong call. There are situations where a careful do-it-yourself approach, or a lighter professional study, is a sensible match for the stakes involved. The honest test is proportionality: how much deduction is on the line, and how complex is the property?

- The property is modest in value, so the dollars at stake from a misclassification are small.

- The building is simple, with few specialty systems or unusual components to identify.

- You are using the DIY estimate only as a screen to decide whether a real study is worth commissioning.

- You are comfortable taking a conservative allocation rather than maximizing the first-year number.

- Your CPA has reviewed your approach and is willing to sign the return behind it.

A free calculator is a genuinely useful first step. Run your property through one, see roughly what an accelerated allocation could produce, and compare that to the quoted cost of an engineered study. If the calculator suggests modest first-year benefit, the math may simply not justify a full study, and a conservative DIY or desktop approach blessed by your CPA could be appropriate. The estimate becomes a decision tool rather than your final, audit-facing support.

The mistake is not using an online estimate. The mistake is treating an online estimate as if it were an engineered study and claiming an aggressive deduction with nothing real behind it.

When the Property Justifies a Professional Study

On the other side, the larger and more complex the property, the more an engineered study earns its fee. As the dollar amount being reclassified grows, two things happen at once: the tax benefit of getting the allocation right gets bigger, and the cost of getting it wrong on exam gets bigger too. Past a certain point the study is not really an expense; it is cheap insurance on a much larger number.

Lean Toward an Engineered Study When

- The property is higher value, so the reclassified dollars are large

- The building has many specialty systems or unique components

- You intend to claim an aggressive, bonus-driven first-year deduction

- You have multiple properties and want consistent methodology

- Your tax situation makes a disallowance especially costly

A Lighter Approach May Suffice When

- The property is low value and simple in construction

- The potential first-year benefit is modest

- You only need a screen before deciding on a full study

- A professional desktop study covers the risk adequately

- Your CPA is comfortable with a conservative allocation

A useful gut check: estimate the first-year tax savings the acceleration would create, then compare it to the study fee and to the downside if the allocation were challenged. When the savings dwarf the fee and the downside is meaningful, the engineered study is almost always the right move. When the savings barely exceed the fee, slow down and reconsider whether you need the full treatment at all.

A Study Only Helps If You Can Actually Use It

Here is the trap that catches more short-term rental owners than a botched allocation ever will: spending money on a beautiful engineered study and then being unable to use the depreciation it unlocks. Accelerated depreciation produces a big loss, but a loss only offsets your W-2 or business income if that loss is non-passive. For an STR, that hinges on two facts that have nothing to do with the cost-seg report itself.

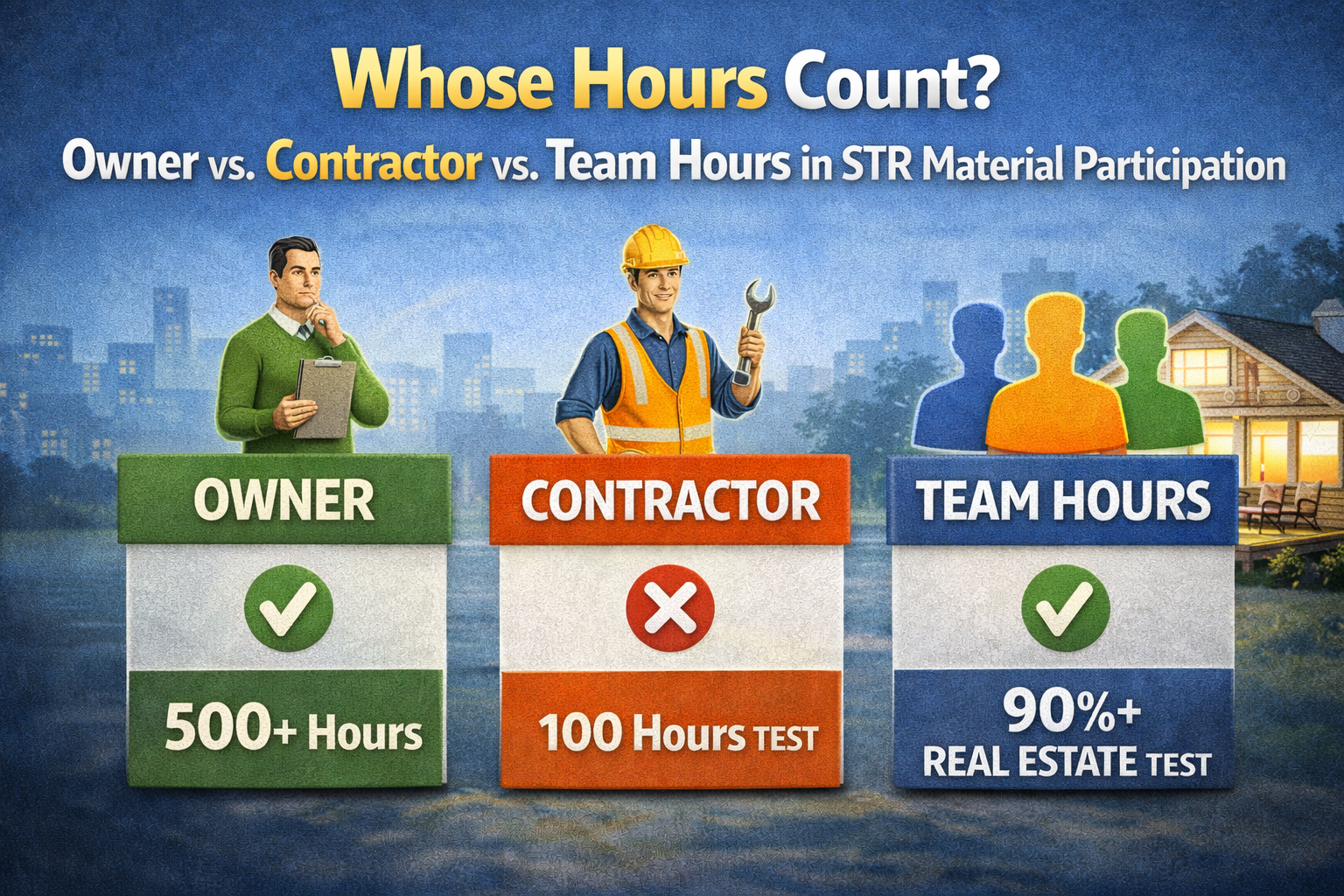

- Your average guest stay must be 7 days or fewer, which keeps the property out of "rental activity" status under Reg. 1.469-1T(e)(3) so it is not automatically passive and you do not need Real Estate Professional (REP) status.

- You must materially participate under the tests of Reg. 1.469-5T, commonly the more-than-500-hour test or the more-than-100-hours-and-more-than-anyone-else test.

If your average stay creeps over 7 days, or if your cleaner, co-host, or property manager logs more hours than you do and defeats the 100-hour test, that gorgeous depreciation becomes a suspended passive loss. It sits on the shelf doing nothing for your current tax bill, no matter how engineered the study was. The cost-seg report and the right to use it are two separate problems, and owners routinely solve the first while ignoring the second.

This is where REP Helper fits. The cost-segregation study itself is the specialist firm's job; REP Helper's job is proving the two facts that let you actually use the depreciation. It calculates your average stay per property straight from your bookings so you know whether you are under the 7-day line, and it logs material-participation hours contemporaneously by phone, voice, or web as you do the work.

Crucially, REP Helper tags every logged activity by who performed it, owner versus spouse versus cleaner versus co-host versus property manager, so you can prove you out-participated everyone else for the 100-hour test. It tracks your progress toward whichever material-participation test you are aiming at, keeps your placed-in-service evidence, and produces CPA-ready documentation.

Putting It Together: A Simple Decision Path

You do not have to choose between "never DIY" and "never hire anyone." The sensible path runs in order: estimate first, decide second, and only then commission the level of study that matches the stakes. Here is a workflow that keeps you out of trouble.

- Run a free online estimate to gauge the potential first-year benefit on your property.

- Confirm you can actually use the depreciation: average stay 7 days or fewer, and a realistic path to material participation.

- Compare the estimated savings to study fees and to the downside of a challenged allocation.

- For small, simple properties with modest benefit, consider a conservative DIY or desktop study with CPA review.

- For higher-value or complex properties, or aggressive bonus-driven deductions, commission an engineered study.

- Keep your placed-in-service date, your booking-based average stay, and your tagged participation hours documented all year, not reconstructed at filing time.

Done in that order, the cost-seg question stops being "DIY or pro?" and becomes "what level of support does this specific deduction justify, and can I prove I am entitled to use it?" That is a far better question, and it is the one a careful owner and a good advisor can actually answer together.

Frequently Asked Questions

Q: Is it legal to do my own cost segregation without hiring a firm?

A: Yes. The IRS does not require you to hire anyone to classify your depreciation. What it does scrutinize is your support. You are free to do the allocation yourself, but if you claim an aggressive accelerated deduction with nothing behind it but an online calculator, you carry the risk that an examiner disallows it. The legality is not the issue; the defensibility is.

Q: Will using a free online cost-seg calculator trigger an audit?

A: Using the tool does not trigger anything by itself, and an online estimate is a perfectly good first screen. The exposure comes from claiming a large, aggressive deduction whose only support is that estimate. A big first-year loss can draw attention regardless of how it was calculated, so the real question is whether you can document your method if asked, not which tool you started with.

Q: What is the difference between a desktop study and a full engineered study?

A: A full engineered study includes a site inspection where a specialist identifies and measures actual components. A desktop or modeling study is done by a professional using photos, plans, and real cost data but without a physical walk-through. The desktop version is cheaper and still far more defensible than a free calculator, which makes it a reasonable middle option for smaller, simpler properties.

Q: How big does a property need to be before a professional study is worth it?

A: There is no universal threshold, but the logic is proportionality. Estimate the first-year tax savings the acceleration would create and compare it to the study fee and to the downside if the allocation were challenged. When the savings clearly dwarf the fee and a disallowance would hurt, an engineered study is usually worth it. When the benefit barely exceeds the fee, a lighter approach may make more sense. Ask your CPA to run the comparison with you.

Q: I paid for a great study but cannot use the loss. What happened?

A: Almost always one of two things. Either your average guest stay crept above 7 days, which makes the property a rental activity and pushes the loss back to passive, or someone else (a cleaner, co-host, or property manager) participated more than you and defeated your material-participation test. The depreciation is real but suspended as a passive loss. REP Helper exists to keep those two facts on track, calculating your average stay from bookings and logging tagged participation hours so the loss you paid to create is one you can actually use.

About the author

Real Estate Investor · Founder, REP Helper

Carlos Lourenço is a real estate investor and the founder of REP Helper. Over 10+ years he's built a portfolio of long- and short-term rentals across several states, personally qualifying for Real Estate Professional Status (REPS) and running the short-term-rental strategy on his own properties. A product manager by trade, he built REP Helper after years of tracking his own hours and IRS tests by hand.

Connect on LinkedInDisclaimer: Carlos Lourenço is a real estate investor, not a CPA, enrolled agent, or tax attorney. This article is for educational purposes only and is not tax, legal, or financial advice. Tax outcomes depend on your specific facts and on current law, which changes. Always consult a qualified CPA or tax attorney before implementing any tax strategy.