Introduction

The short-term rental "loophole" is one of the most powerful tax strategies available to W-2 earners and business owners who do not qualify as Real Estate Professionals. Run the property with an average guest stay of 7 days or fewer, materially participate, and your losses can be non-passive and offset active income.

Most articles about this strategy live entirely in the world of federal tax law: average-stay math, the seven material-participation tests, cost segregation, bonus depreciation. All of that matters. But there is a quieter risk that sits underneath the whole structure and can quietly demolish it before you file a single form.

Your city, county, and HOA do not care about Section 469. But their rules control the facts your federal tax result is built on.

A minimum-night ordinance, an outright STR ban, a permit cap, or a single HOA covenant can force your average stay above 7 days, or stop you from renting short-term at all. When that happens, the elegant federal strategy you researched simply does not have a property to attach to. This article is about that local-regulation risk: what to look for, why it must happen before you buy, and how a mid-strategy rule change can undo everything.

Two Separate Systems That Quietly Interact

It helps to be precise about what is happening, because people conflate two very different bodies of law and then get surprised.

Federal Tax Law

- Decides whether your activity is a "rental activity" under Reg. 1.469-1T(e)(3)

- Cares about average guest stay (7 days or fewer)

- Cares about material participation under Reg. 1.469-5T

- Determines whether losses are passive or non-passive

- Enforced by the IRS

Local / Private Law

- Decides whether you may operate an STR at all

- Sets minimum-night requirements and zoning

- Issues (or caps) permits and licenses

- HOA covenants restrict use of the unit

- Enforced by the city, county, or HOA board

Notice that the IRS does not set a minimum-night rule and your city does not care whether you materially participate. They are independent. The trap is that they are not insulated from each other. Local law dictates the operating facts, and federal tax law then applies to those facts.

The federal loophole is a conclusion drawn from your operating reality. If local law changes the reality, the conclusion changes with it.

So when a city ordinance says "no rentals under 30 days in this zone," it is not a tax rule, but it has a direct tax consequence: it makes a 7-day-or-fewer average impossible, which means the activity is treated as a rental activity, which means your losses are passive again unless you can clear the much harder Real Estate Professional bar.

The Minimum-Night Ordinance Trap

This is the single most dangerous local rule for the STR loophole, precisely because it looks harmless. A growing number of cities and counties have adopted minimum-stay ordinances to discourage party rentals and protect long-term housing supply. Common forms include a 7-night minimum, a 30-night minimum, or seasonal minimums that change throughout the year.

Recall how the federal average is computed: total rental nights divided by the number of separate reservations, per property, per year. The loophole requires that average to be 7 days or fewer. A minimum-night ordinance attacks the math directly.

- A 30-night minimum makes every reservation at least 30 days, so your average stay can never fall to 7 or fewer. The loophole is structurally impossible.

- Even a 7-night minimum is dangerous: an average of "7 days or fewer" is easy to breach when the FLOOR on every stay is 7. A few longer bookings push the average over the line.

- Seasonal minimums (for example, 30-night minimums in peak months) can wreck the annual average even if shoulder-season stays are short.

A 7-night minimum does not give you a 7-day average. It removes your cushion. "7 or fewer" needs short stays to average down against the long ones — and the ordinance bans the short ones.

This is why the average is a year-end number you must actually watch, not assume. If a property sits in a zone with a 7-night minimum and you take several two-week bookings, you can quietly cross into rental-activity territory without noticing until you file.

REP Helper calculates your average stay per property directly from your bookings throughout the year, so you can see in real time whether a string of longer reservations — forced or chosen — is dragging your average over the 7-day line while there is still time to adjust your booking strategy.

Bans, Caps, and Permits: When You Cannot Operate at All

Minimum-night rules degrade the strategy. The next category can stop it cold. If you cannot legally run a short-term rental, there is no activity to characterize, no material participation to count, and no depreciation to accelerate against active income.

- Outright bans: some cities prohibit non-owner-occupied STRs entirely, or ban them in specific residential zones.

- Permit and license caps: many jurisdictions issue a fixed number of STR permits, run waitlists, or stop issuing new ones. You can buy a perfect property and never get a permit.

- Owner-occupancy requirements: some rules only allow STRs if the owner lives on-site, which interacts with the federal personal-use limits under Section 280A.

- Primary-residence-only rules: STR allowed only in your primary home, sometimes capped at a number of nights per year, which can defeat the loophole math on its own.

- Density and proximity rules: limits on how many STRs can operate per block or within a set distance of each other.

A permit cap is the cruelest version of this risk: the property qualifies, the numbers work, the strategy is sound — and the city simply will not let you in.

If you also live in the property, watch the federal overlay. Under Section 280A, personal use of more than the greater of 14 days or 10% of the days rented at fair value makes the dwelling a "residence" and limits your loss deductions — so an owner-occupancy rule that local law requires can collide with the federal result you are after.

The HOA Risk Most Investors Ignore

Even when the city and county are friendly, a private homeowners association can override all of it. HOA covenants, conditions, and restrictions (CC&Rs) frequently impose minimum lease terms — often 30, 90, or 180 days — specifically to keep short-term renters out. These are private contracts you agree to at closing, and they are enforceable even where city law would permit a short-term rental.

The HOA risk is sneaky for three reasons:

- It is not in the zoning code, so a check of city ordinances alone will miss it.

- HOA boards can amend the CC&Rs by member vote, so a permissive document today can become a 30-day-minimum document next year.

- A 30-day HOA minimum has the exact same federal effect as a 30-day city ordinance — it makes a 7-day-or-fewer average impossible — but investors often never read the CC&Rs closely.

Read the CC&Rs before you buy, and read them for minimum-lease and rental-use clauses specifically. An HOA minimum-stay rule kills the loophole just as effectively as a city one.

Diligence Local Rules BEFORE You Buy

The whole strategy is decided at the property level, which means the time to discover a fatal local rule is before closing, not after a cost-segregation study and a year of operations. Treat regulatory diligence as part of underwriting, on equal footing with the financials.

- Confirm short-term rentals are permitted in the specific zoning district of the exact address, not just "the city."

- Find the minimum-night requirement, if any, including seasonal variations — anything 8 nights or longer threatens the average-stay test.

- Verify a permit or license is available, not capped, waitlisted, or frozen, and learn the renewal terms.

- Check for owner-occupancy or primary-residence-only requirements.

- Obtain and read the full HOA / condo CC&Rs for minimum-lease and rental-use restrictions.

- Ask whether any ban, cap, or minimum-stay change is currently proposed or under council/board review.

- Get the rules in writing from the jurisdiction; do not rely on a listing agent's summary.

Be especially skeptical when a market is popular and politically active about STRs. Those are exactly the places where rules tighten. A property that pencils out today in a city debating a 30-day minimum is a property whose entire tax thesis could evaporate at the next council vote.

If a single rule — a minimum stay, a missing permit, or an HOA covenant — can break the federal strategy, that rule deserves the same scrutiny as your purchase price.

When the Rules Change in the Middle of Your Strategy

Diligence protects you at purchase. It does not freeze the law. Cities and HOAs change STR rules constantly, and a change mid-strategy is uniquely painful because you may have already invested in the depreciation play — paid for a cost-segregation study and front-loaded large deductions — on the assumption you could keep operating short-term.

Consider the shape of the problem with illustrative numbers only. Suppose you buy in year one, run a 4-day average stay, materially participate, and use a cost-segregation study plus 100% bonus depreciation to generate a large first-year loss against your W-2 income. Then in year two the city imposes a 30-night minimum.

- Year two onward, your average stay is forced above 7 days, so the activity becomes a rental activity again and new losses are passive unless you qualify as a Real Estate Professional.

- The depreciation schedule from the cost-seg study keeps running, but it is now generating passive deductions that may be suspended rather than offsetting active income.

- Depreciation recapture still looms on eventual sale — gain attributable to depreciation is taxed, partly at up to 25% for real property and at ordinary rates for personal-property components — so you accelerated the deduction but the recapture bill does not disappear.

- Your exit options narrow: pivoting to mid-term or long-term rentals may be the only legal path, but that is a different business with a different return profile.

A regulation change does not claw back deductions you legitimately earned while the strategy was valid — but it can stop the strategy from working going forward, which matters most if you were counting on multiple years of active-income offset.

The defensive move is documentation. If your average stay and material participation were genuinely met in the years you claimed the benefit, you want clean, contemporaneous proof of exactly that, so a later rule change — or an examiner reviewing a year of transition — cannot cast doubt on the years that did qualify.

This is where REP Helper earns its place in the strategy. It logs your material-participation hours contemporaneously by phone, voice, or web, tags each activity by who performed it so you can prove you out-participated any cleaner, co-host, or property manager for the 100-hour test, and keeps your placed-in-service date and supporting evidence — producing CPA-ready documentation that nails down the years the loophole held.

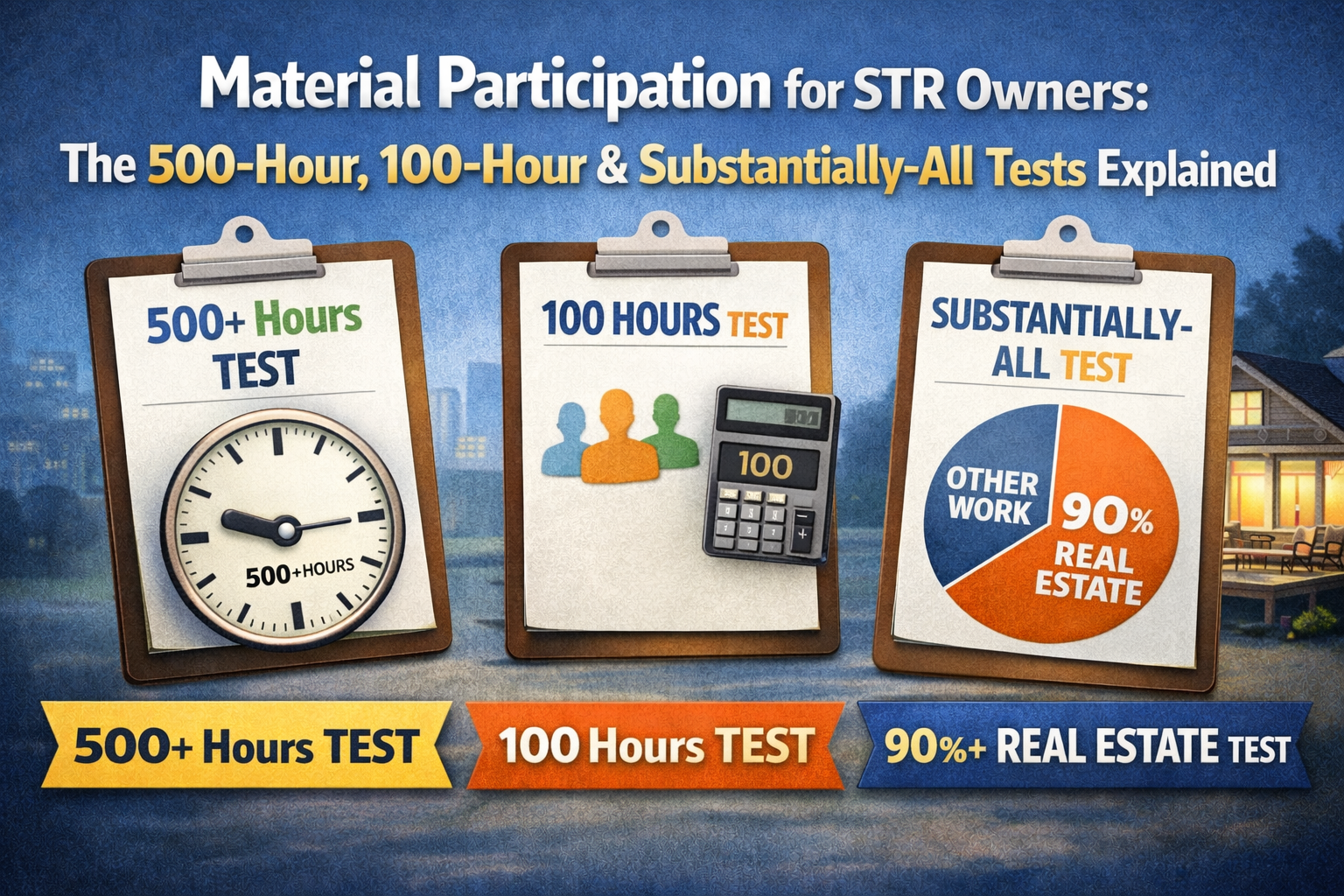

Even When Local Rules Allow It, the Federal Tests Still Apply

It is worth restating the boundary, because clearing local hurdles is necessary but not sufficient. A perfectly legal STR with a 4-day average still gives you nothing against active income unless you also materially participate.

The most common material-participation paths for STR owners are:

- More than 500 hours of participation in the activity during the year.

- More than 100 hours AND more than anyone else — critically, your hours must beat the cleaner, co-host, and property manager combined-by-person comparison.

- Substantially all of the participation in the activity was done by you.

Contractor, employee, and property-manager hours are not your hours. Heavy reliance on a full-service manager can defeat the 100-hour test even when local law is fully satisfied.

So the order of operations is: first confirm local law lets you operate short-term, then confirm your average stay is 7 days or fewer, then confirm you materially participate. Local diligence opens the door; the federal tests determine whether the deduction actually flows. REP Helper tracks your progress toward whichever material-participation test you have chosen so you can see, before year-end, whether you are on pace to clear it.

Frequently Asked Questions

Q: Does a city minimum-night rule directly change my federal taxes?

A: Not directly — the IRS has no minimum-night rule. But it changes the operating facts the federal result depends on. If a local 30-night minimum forces every reservation to be at least 30 days, your average stay can never be 7 days or fewer, so the activity is a "rental activity" under the federal regulations and your losses are passive again. Local law and federal tax are separate systems, but the local rule controls the facts, and the federal conclusion follows the facts.

Q: An HOA allows short-term rentals but my city does not, or vice versa. Which one wins?

A: You must satisfy both, plus the county if it has its own rules. The most restrictive applicable rule controls in practice. An HOA can ban or set a minimum lease term even where the city permits short-term rentals, and a city can ban them even where the HOA is silent. Read the city ordinance, any county rules, and the full HOA CC&Rs, and assume the strictest one governs what you can actually do.

Q: If the rules change after I already took a big depreciation deduction, do I lose it?

A: Deductions you legitimately earned in a year when the strategy was valid are not retroactively clawed back simply because the law changes later. What a mid-strategy change does is stop the strategy from working going forward — future losses can revert to passive. Keep in mind depreciation recapture still applies on sale regardless. This is exactly why contemporaneous proof of your average stay and material participation for the qualifying years is so valuable, and why you should consult a qualified tax advisor about a transition year.

Q: I cannot get an STR permit because the city capped them. Can I still use the loophole?

A: If you cannot legally operate a short-term rental, there is no qualifying activity to attach the strategy to. A permit cap, waitlist, or freeze can block the loophole entirely even when the property and the numbers would otherwise work. This is precisely why you must verify permit availability before you buy — the strategy is decided property by property, and an unavailable permit is a deal-breaker, not a paperwork detail.

Q: How do I prove the loophole held in a year when local rules were in flux?

A: Keep contemporaneous records of the two facts that drive the federal result: your average guest stay per property (computed from your actual bookings) and your material-participation hours, tagged by who performed each task so you can show you out-participated any cleaner, co-host, or manager. REP Helper is built for exactly this — it calculates average stay from your bookings, logs participation hours as they happen, and produces CPA-ready documentation, so the years that qualified are clearly documented even if the rules shifted around them. Always pair this with a qualified tax advisor for the actual filing position.

About the author

Real Estate Investor · Founder, REP Helper

Carlos Lourenço is a real estate investor and the founder of REP Helper. Over 10+ years he's built a portfolio of long- and short-term rentals across several states, personally qualifying for Real Estate Professional Status (REPS) and running the short-term-rental strategy on his own properties. A product manager by trade, he built REP Helper after years of tracking his own hours and IRS tests by hand.

Connect on LinkedInDisclaimer: Carlos Lourenço is a real estate investor, not a CPA, enrolled agent, or tax attorney. This article is for educational purposes only and is not tax, legal, or financial advice. Tax outcomes depend on your specific facts and on current law, which changes. Always consult a qualified CPA or tax attorney before implementing any tax strategy.