Why the Math Matters More Than the Rule

Most short-term rental owners can recite the headline: if the average guest stay is seven days or fewer, the property is not treated as a rental activity, which means it sidesteps the rule that automatically labels rentals as passive. That much is widely explained. What trips people up is not the concept; it is the arithmetic and the operations behind it. The seven-day rule is a measurement, and measurements can be gamed against you by a single long booking, a misread calendar, or a property manager who quietly raised your minimum-night setting for the holidays.

This article is the operational how-to. We are not re-explaining what the rule is for; we are showing you how to calculate the average correctly, how to keep it at or under seven days on purpose rather than by luck, and where the calculation silently goes wrong. If you want the conceptual background on why short stays fall outside rental treatment, that lives in our basic explainer. Here, we stay in the spreadsheet and the booking calendar.

Important framing: clearing the seven-day test does not give you the loss. It only removes the per-se-passive label. You still have to materially participate in the activity for the loss to be non-passive. The math gets you to the starting line, not the finish.

The Formula: Total Nights Divided by Number of Stays

The average period of customer use is calculated for the tax year, per property, as the total number of rental-use days divided by the number of separate periods of customer use. In plain operational terms: add up every night a paying guest occupied the property across the whole year, then divide by the number of distinct stays (reservations). The result must be 7 or less.

Notice what the denominator is. It is the count of stays, not the count of guests, not the count of nights, and not the count of months. One reservation for five nights is one stay of five nights. Ten reservations of three nights each is ten stays totaling thirty nights, for an average of three. This is the single most important distinction in the entire calculation, because confusing the denominator is where the majority of errors begin.

Worked example A (passes)

- 40 separate stays during the year

- 210 total rental nights

- 210 / 40 = 5.25 average days

- 5.25 is at or under 7, so it is not a rental activity

Worked example B (fails)

- 18 separate stays during the year

- 150 total rental nights

- 150 / 18 = 8.33 average days

- 8.33 exceeds 7, so it stays a rental activity

These figures are illustrative. The takeaway is structural: the same property can pass or fail depending on the mix of stay lengths, and you control that mix through your booking settings. Run this formula on your own actual calendar, not on a guru's hypothetical, and confirm the result with your tax advisor before relying on it.

What Counts as a Night, and as a Stay

Before you can divide, you have to know exactly which days and which reservations belong in the calculation. Getting the inputs right is more than half the battle, because a clean formula on dirty data still produces a wrong answer.

- Count only days of paying customer use as rental nights. The numerator is occupancy by guests who are paying for short-term use.

- Each separate reservation is one stay, regardless of how many people are in the party. A family of six on one booking is a single stay.

- Owner-blocked dates, when you or family use the property personally and no one is paying, are not paying-customer nights and are generally excluded from this rental-use average. They have separate personal-use consequences elsewhere on your return, so flag them but do not put them in the numerator.

- Vacant nights between guests are not counted as rental nights; they are simply nights with no stay.

- A back-to-back same-guest situation, such as a guest who books, checks out, and rebooks for a fresh period, is generally two stays if they are two distinct reservations. Document the booking records so the count is defensible.

Edge case worth flagging: gaps and partial cleanings. The turnover day itself is usually a checkout in the morning and a check-in in the evening counted within the respective stays' nights, not a separate phantom rental night. Do not double-count the changeover.

Operational Levers to Keep the Average at or Under Seven

If your strategy depends on staying inside the seven-day test, you do not want to discover in February that one ten-night winter booking pushed your average over the line. You want the calendar configured so it is structurally hard to fail. Here are the practical levers, in roughly the order of how much control they give you.

- Set a maximum-stay cap of 7 nights on every booking channel. This is the single most powerful lever: if no individual reservation can exceed seven nights, your average is mathematically guaranteed to be seven or fewer.

- If a 7-night cap is too restrictive for your market, set the cap lower (for example 5 or 6 nights) on your peak periods so that the inevitable occasional longer stay has slack to average against.

- Audit every channel separately. Airbnb, Vrbo, Booking.com, and your direct-booking site can each carry their own minimum and maximum night settings; a manager or co-host may change one without telling you.

- Disable or carefully gate any 'monthly stay' or '28+ night' discount features, which exist specifically to attract long bookings that will blow past seven days.

- Decline or redirect off-platform inquiries for multi-week stays into a separate property or a separate strategy, rather than accepting them on a property where you are managing to the seven-day test.

- Recalculate the running average at least quarterly, not just at year-end, so you can course-correct while there is still calendar left to adjust.

The maximum-stay cap is the safety net, but the quarterly recalculation is the seatbelt. Together they turn the seven-day test from an anxious year-end coin flip into a managed number. REP Helper's average-stay calculation for STRs is built for exactly this: it pulls your nights and stays per property and shows the running average as the year unfolds, so a single long booking is visible the moment it lands rather than at filing.

The Miscalculations That Quietly Break the Rule

Almost every failed seven-day calculation we see comes from one of a short list of recurring mistakes. None of them are exotic. They are the kind of error that looks fine until you re-run the numbers carefully.

- Averaging the wrong way. Owners compute 'average nights per booking' in their head and assume it matches the test, but then accidentally use total guests or total months as the denominator. The denominator is the number of distinct stays. Nothing else.

- Blending multiple properties. The test is applied per property (or per appropriate unit of activity), not portfolio-wide. Two properties at 5 days and 9 days do not average to a passing 7; the 9-day property fails on its own.

- The single long stay. One generous multi-week booking can drag a year of short stays above the line. Twenty stays at 4 nights plus one stay at 70 nights is 150 nights over 21 stays, which is about 7.1, just over.

- Counting owner-blocked or vacant days as rental nights. Padding the numerator with personal-use or empty nights inflates the average and is simply wrong data.

- Forgetting the calculation is annual. A property can pass for one tax year and fail the next purely because the booking mix shifted. It is not a one-time determination; re-run it every year.

- Assuming passing the test finishes the job. The most consequential miscalculation of all is treating a sub-7-day average as the whole strategy and never establishing material participation.

A useful gut check: if your average is sitting between 6 and 7, you have almost no margin for error. One miscounted long stay or one wrongly included owner-block can flip the result. Treat anything above roughly 6.0 as a yellow flag and tighten your maximum-stay settings.

Edge Cases and the 30-Day Variant

The seven-day test has a less-discussed sibling. Under the same regulation, an activity can also fall outside rental treatment when the average customer use is 30 days or fewer and significant personal services are provided, or when extraordinary personal services are provided regardless of the average period. These are narrower and more facts-and-circumstances heavy, but they matter for operators whose stays naturally run longer than a week.

The 7-day path (most common)

- Average guest stay 7 days or fewer

- No services requirement to escape rental treatment

- Cleanest to operate to with a max-stay cap

- Still requires material participation for the loss

The 30-day-plus-services path

- Average stay 30 days or fewer

- Plus significant personal services to guests

- More fact-specific and harder to document

- Also still requires material participation

A few other edge cases deserve a note. A property converted to or from short-term use mid-year still has its average computed over its actual rental-use days for that year. A property rented partly short-term and partly on long leases is genuinely messy and should be discussed with your advisor, because the character of the activity can be unclear. And remember that even where you legitimately clear seven days, this only addresses whether the activity is a rental activity; it does not by itself make any loss usable.

After You Pass: Material Participation Is the Real Gate

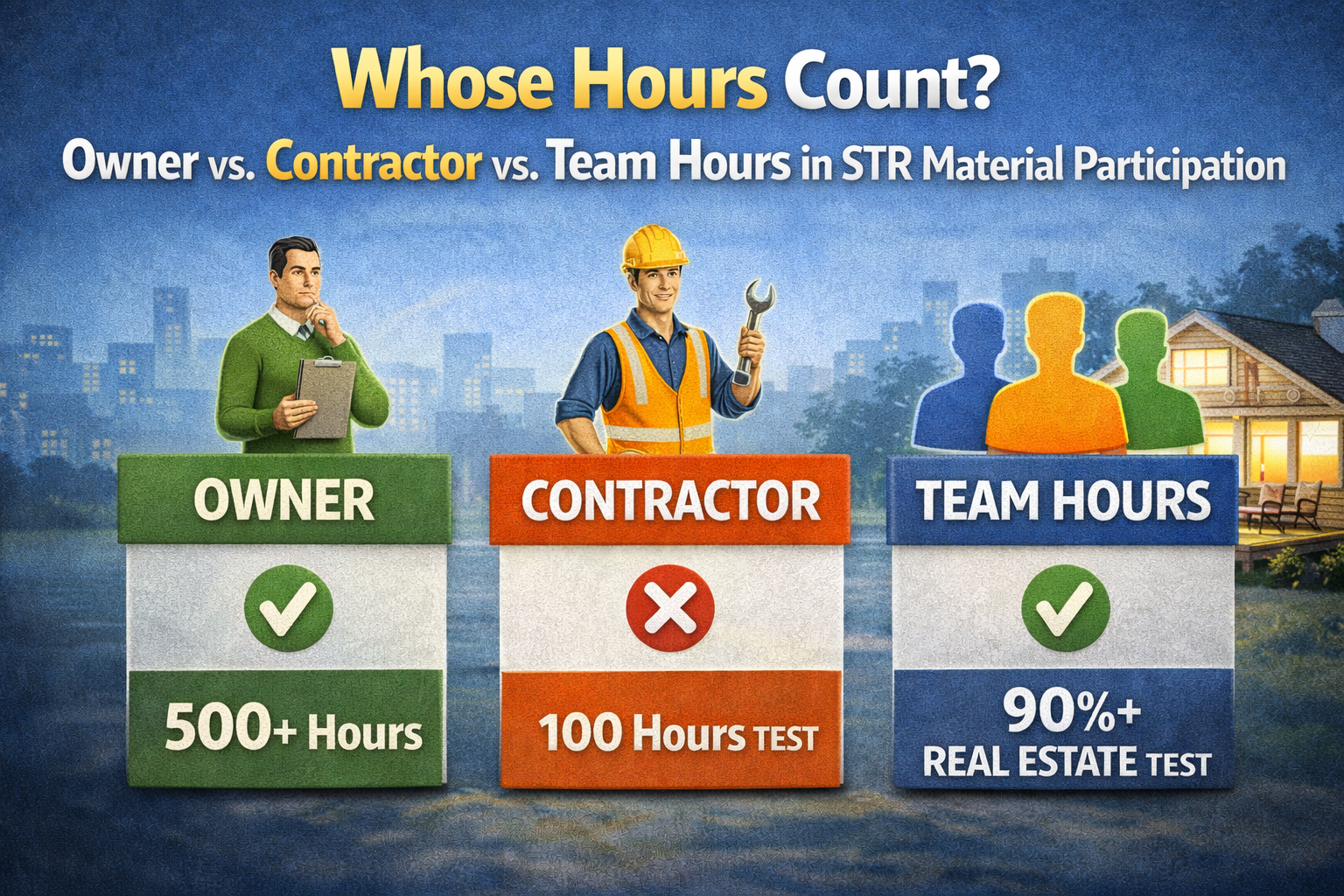

This is the point the operational crowd most often misses, so it earns its own section. Clearing the seven-day test means your activity is not a rental activity, which means it is not automatically passive and you do not need Real Estate Professional status for it. But not-automatically-passive is not the same as non-passive. To deduct losses against your other income, you must materially participate in the activity under the seven tests of Treas. Reg. section 1.469-5T.

- The 500-hour test is the one most short-term operators rely on: participate more than 500 hours in the activity during the year.

- The 100-hour test can work if your hours exceed 100 and no other individual, including a cleaner or co-host, participates more than you.

- The substantially-all test applies when essentially all of the work in the activity is done by you.

- Other tests exist (significant participation, prior-year history, and facts-and-circumstances), but for an actively run STR the 500-hour and 100-hour tests are the practical workhorses.

Hours spent on a self-managed short-term rental, such as guest communication, scheduling turnovers, restocking, maintenance, and bookkeeping, are exactly the kind of records that need to be contemporaneous to survive scrutiny. REP Helper logs these by phone, voice, or web as the work happens, tags each entry by who performed it (you, a spouse, or a contractor), and tracks your hours per property toward the material-participation thresholds, so the average-stay number and the participation hours live in one defensible file.

Bottom line: a sub-7-day average answers 'is this a rental activity?' (no). Material participation answers 'is the loss passive?' (also no, if you clear it). You need both answers to go your way. This is general information, not advice for your specific facts, so confirm the application with your tax advisor.

Putting It Together: A Year-Round Operating Rhythm

The owners who never sweat the seven-day test at filing time are the ones who turned it into a routine rather than a year-end scramble. Here is a workable rhythm.

- Before the year starts: set a 7-night (or lower) maximum-stay cap on every channel and document the setting with a screenshot.

- Monthly: log a quick check that no booking slipped past the cap and that no channel setting was changed.

- Each turnover: capture material-participation hours contemporaneously, tagged to the property and to who did the work.

- Quarterly: recalculate the running average (total paying nights divided by number of stays) per property and confirm it is comfortably under 7.

- If the average creeps toward 6: tighten max-stay caps for the remainder of the year before it crosses the line.

- At year-end: reconcile owner-blocked and vacant days out of the numerator, finalize the per-property average, and export a CPA-ready record of both the average-stay math and the participation hours.

Done this way, the seven-day test becomes a number you watch all year rather than a verdict you receive in April. The same system that produces a clean average-stay figure also produces the contemporaneous participation log that the real gate, material participation, depends on.

Frequently Asked Questions

Q: Is the seven-day test based on each booking or on the whole year's average?

A: It is the whole-year average for the property, calculated as total paying rental nights divided by the number of separate stays. No single booking determines it, although one unusually long booking can pull the annual average above seven, which is exactly why a maximum-stay cap is so effective.

Q: If my average is seven days or fewer, do I still need Real Estate Professional status?

A: No. Once the average is seven or fewer, the activity is not a rental activity, so the rule requiring REP status for rentals does not apply to it. You do, however, still have to materially participate in the activity, usually via the 500-hour or 100-hour test, for the loss to be non-passive and offset your other income.

Q: Do owner-use or vacant nights count in the calculation?

A: No. The numerator is paying-customer nights only. Owner-blocked personal-use nights and vacant nights between guests are not rental nights for this average. Personal use has separate consequences elsewhere on your return, so track it, but keep it out of the seven-day numerator.

Q: Can I average two properties together to pass?

A: No. The seven-day determination is made per property (the relevant unit of activity), not across your whole portfolio. A property at nine days fails on its own even if another property at five days would, on paper, average down to seven. Run the math property by property.

Q: My average is sitting right at 6.8 days. Is that safe?

A: It passes, but it has almost no margin. A single miscounted long stay or a wrongly included owner-block can flip it over seven. Treat anything above roughly 6.0 as a yellow flag, tighten your maximum-stay settings, and watch the running average more frequently. When the number is this close, confirm your inputs and your conclusion with your tax advisor.

About the author

Real Estate Investor · Founder, REP Helper

Carlos Lourenço is a real estate investor and the founder of REP Helper. Over 10+ years he's built a portfolio of long- and short-term rentals across several states, personally qualifying for Real Estate Professional Status (REPS) and running the short-term-rental strategy on his own properties. A product manager by trade, he built REP Helper after years of tracking his own hours and IRS tests by hand.

Connect on LinkedInDisclaimer: Carlos Lourenço is a real estate investor, not a CPA, enrolled agent, or tax attorney. This article is for educational purposes only and is not tax, legal, or financial advice. Tax outcomes depend on your specific facts and on current law, which changes. Always consult a qualified CPA or tax attorney before implementing any tax strategy.