The 60-Second Version

If you only have a minute, here it is: "material participation" is the IRS phrase for being genuinely involved in your rental business, rather than treating it as a hands-off investment. When you materially participate, the tax law stops treating your rental losses as automatically "passive," and a non-passive loss can offset your salary, business income, or other active earnings.

The shortcut definition: material participation means you are involved on a regular, continuous, and substantial basis. The most common way to prove it is to work more than 500 hours in the activity during the tax year.

That is the whole concept in one breath. The rest of this article unpacks each piece in plain English so you understand what counts, why it matters, and how it differs from Real Estate Professional status (REP), which people constantly confuse with it.

What Material Participation Actually Means

Material participation is a legal standard defined in Treasury Regulation section 1.469-5T. Strip away the jargon and it asks a single question: are you really running this activity, or are you a silent investor along for the ride?

The regulation uses three words to describe real involvement: regular, continuous, and substantial. Showing up consistently throughout the year, staying involved over time, and doing meaningful work, not just rubber-stamping a property manager's decisions, is the heart of the test.

This looks like material participation

- Screening tenants and handling leases yourself

- Coordinating repairs and meeting vendors

- Managing bookings, pricing, and guest communication

- Keeping the books and making spending decisions

- Being on call for issues throughout the year

This looks passive

- Hiring a manager and only reviewing a year-end statement

- Approving large expenses by email a few times a year

- Letting a syndicator run everything for you

- Owning a slice with no operational role

- Doing a burst of work once, then disappearing

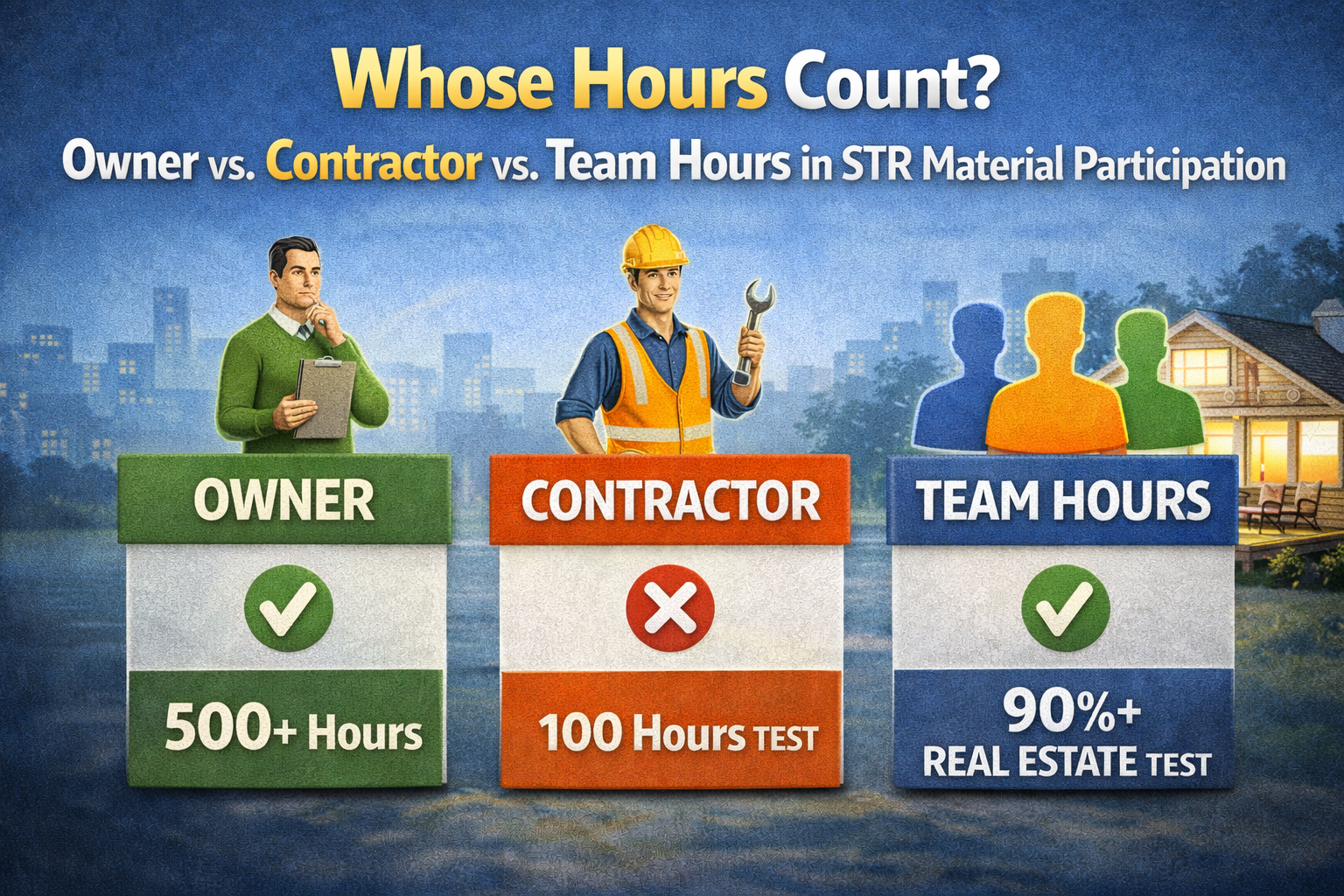

The One Test Most People Use: 500 Hours

The IRS lists seven different ways to prove material participation, but most rental owners lean on the simplest and most defensible one: the 500-hour test. If you spend more than 500 hours on the activity during the tax year, you materially participate. Full stop, no further analysis required.

Five hundred hours sounds like a lot until you spread it across a year. It works out to roughly ten hours a week. For owners who self-manage, who handle a short-term rental, or who are mid-renovation, that pace is realistic. For a single long-term rental run by a property manager, it usually is not, which is an honest signal that the activity may simply be passive for you.

Why 500 is the favorite: it is a bright-line number. The other tests involve comparisons, multi-year history, or vaguer "facts and circumstances" judgment calls. If you clearly clear 500 hours, you avoid all of that.

The catch is that 500 hours is also 500 hours you must be able to prove. A guess on a tax return is not evidence. This is exactly the gap REP Helper is built to close: you log work contemporaneously by phone, voice, or web as it happens, so by year-end your hours exist as a record rather than a reconstruction.

The Other Six Tests, in One Glance

You do not need to memorize the full list to understand material participation, but it helps to know that 500 hours is not the only door. Here are the other six tests in plain language. You only have to satisfy one of the seven.

- Substantially all: you did essentially all of the work in the activity, even if total hours were modest.

- 100 hours and not less than anyone else: you worked more than 100 hours and no other single person worked more than you did.

- Significant participation activities: you spent more than 100 hours in this activity and your combined hours across several such activities top 500.

- Any 5 of the last 10 years: you materially participated in 5 of the prior 10 tax years.

- Personal service activity for any 3 prior years: relevant mainly to certain service businesses, not typical rentals.

- Facts and circumstances (100+ hours): based on the full picture you participated regularly, continuously, and substantially, and worked at least 100 hours.

Want the deep version? Our full deep-dive walks through all seven tests with a worked example for each. This primer stays in the fast lane on purpose.

Why It Matters: Passive vs. Non-Passive

Here is the payoff that makes all of this worth understanding. Under the passive activity loss rules of Internal Revenue Code section 469, losses from a passive activity can generally only offset passive income, not your wages or business profit. Anything you cannot use gets suspended and carried forward to future years.

Materially participating is what flips a loss from passive to non-passive. A non-passive rental loss, often driven by depreciation, can offset active income such as a salary, dramatically changing your tax bill in the year you generate it.

Passive (no material participation)

- Loss only offsets passive income

- Unused loss is suspended and carried forward

- Limited $25,000 allowance phases out from $100k to $150k MAGI

- Salary stays fully taxed this year

Non-passive (you materially participate)

- Loss can offset active income like W-2 wages

- Benefit lands in the current tax year

- No income phase-out to navigate

- Often the whole point of an aggressive depreciation strategy

Illustrative only: figures and outcomes depend entirely on your specific situation, so treat the above as the shape of the rule, not a promise. Always confirm with your tax advisor.

Material Participation Is Not the Same as REP

This is the single most common point of confusion, so it is worth 30 seconds. Real Estate Professional status (REP) and material participation are two separate gates. Clearing one does not clear the other.

- REP status: an annual, per-person test requiring more than 750 hours in real property trades or businesses AND more than 50% of all your working hours in those businesses. REP removes the rule that says rentals are automatically passive.

- Material participation: a per-activity test (the seven tests above) that determines whether you are truly running each activity. This is what actually makes the loss non-passive.

Think of REP as getting you into the building and material participation as getting you into the room. For your rental losses to offset active income, you generally need both, in the same tax year.

Because the two gates use different hour thresholds (750 and 50% for REP, often 500 for material participation), it is easy to satisfy one and quietly miss the other. REP Helper tracks both at once, including your outside W-2 hours so the 50% ratio updates live, and it tracks material participation separately per property or for your grouped portfolio.

A Quick Note for Short-Term Rentals

Short-term rentals deserve a one-paragraph callout because they bend the usual rules. If the average guest stay is seven days or fewer, the activity is not treated as a "rental activity" under Reg. section 1.469-1T(e)(3). That means it is not automatically passive, and you do not need REP status for it.

The catch that trips people up: even with the seven-day rule, you still must materially participate. The STR loophole skips the REP gate, not the material-participation gate.

For STR owners, that average-stay number is load-bearing, so it has to be calculated correctly. REP Helper computes average guest stay automatically and tags your hours to the right material-participation test, which keeps the seven-day claim and the participation claim consistent with each other.

The Part People Skip: Proving It

Understanding the rule is the easy 60 seconds. Surviving an exam is the hard part, and it comes down to one thing: evidence. Courts have repeatedly rejected hour claims that rested on after-the-fact estimates, round numbers, and "ballpark" recollections. If you cannot prove the hours, you do not get the benefit.

- Log hours contemporaneously, as the work happens, not in a year-end scramble

- Record the date, the time spent, and a specific description of each task

- Tag who did the work (you, your spouse, or a contractor), since only the right people's hours count

- Note which property and which test the time supports

- Keep corroborating evidence: emails, invoices, calendars, and receipts

- Be ready to produce a clean, CPA-ready summary on request

This checklist is the entire job of REP Helper: contemporaneous logging by phone, voice, or web; automatic tagging by person and by test; per-property and grouped material-participation tracking; and CPA-ready exports when it is time to file or defend a return.

Frequently Asked Questions

Q: What is the simplest definition of material participation?

A: It means you are involved in your rental activity on a regular, continuous, and substantial basis, rather than as a hands-off investor. The most common way to prove it is to spend more than 500 hours on the activity during the tax year, which is one of seven IRS tests.

Q: Is 500 hours a hard requirement?

A: No. The 500-hour test is just the most popular and most defensible of the seven tests because it is a bright line. You can also qualify by doing substantially all the work, by working 100+ hours when no one else worked more, or by meeting one of the other tests. You only need to satisfy one.

Q: Do I need to be a Real Estate Professional to materially participate?

A: No, they are separate. Material participation is a per-activity test that makes a loss non-passive. REP status is a separate annual test (more than 750 hours and more than 50% of your working time in real property businesses) that removes the automatic-passive label on rentals. For losses to offset active income you generally need both, but one does not grant the other.

Q: Why does material participation matter for my taxes?

A: It determines whether a rental loss is passive or non-passive. Passive losses can usually only offset passive income and otherwise carry forward, while a non-passive loss can offset active income like your salary in the current year. That difference is often the entire reason an investor pursues a depreciation-driven strategy.

Q: How do I prove I materially participated if the IRS asks?

A: With a contemporaneous log of dates, hours, and specific tasks, backed by corroborating records like emails, invoices, and calendars. Estimates reconstructed at filing time tend to fail in audits. Tools like REP Helper let you log the work as it happens and export a CPA-ready record, which is the difference between claiming the hours and proving them. As always, confirm your specifics with your tax advisor.

About the author

Real Estate Investor · Founder, REP Helper

Carlos Lourenço is a real estate investor and the founder of REP Helper. Over 10+ years he's built a portfolio of long- and short-term rentals across several states, personally qualifying for Real Estate Professional Status (REPS) and running the short-term-rental strategy on his own properties. A product manager by trade, he built REP Helper after years of tracking his own hours and IRS tests by hand.

Connect on LinkedInDisclaimer: Carlos Lourenço is a real estate investor, not a CPA, enrolled agent, or tax attorney. This article is for educational purposes only and is not tax, legal, or financial advice. Tax outcomes depend on your specific facts and on current law, which changes. Always consult a qualified CPA or tax attorney before implementing any tax strategy.