Why This Step Decides Everything

There is a moment in every short-term rental tax plan where the strategy either works or quietly collapses, and it is not the moment most owners worry about. People obsess over the 7-day average stay rule, the cost segregation study, the bonus depreciation percentage. Those matter. But none of them put a dollar against your W-2 income unless you clear one final, unglamorous hurdle: material participation. This is the step where the loophole is actually won, and it is the step most people treat as an afterthought.

Here is the logic in plain terms. If your average guest stay is seven days or fewer, your property is not a "rental activity" under Treasury Regulation Section 1.469-1T(e)(3). That removes the automatic passive label that normally traps rental losses. But removing the automatic label does not make your losses non-passive by itself. Once the property is treated like any other trade or business, the passive-versus-non-passive question turns on a single test: did you materially participate? Beat the 7-day rule and fail material participation, and your losses are still passive. The depreciation still piles up; it just sits suspended, doing nothing for your tax bill until you sell.

This guide is deliberately action-oriented. It is not another explainer of the seven tests. It is the operating manual: pick your test, do the qualifying work, manage the people around you so they don't sink your hours, and log it in a way that survives scrutiny.

We will move in the order you should actually work: choose the right test for your situation, build the year's worth of qualifying activities, handle the cleaners and co-hosts and property managers who can defeat you, and finally set up a logging system you can defend. A note up front, because this area is technical and fact-specific: treat this as a way to run your own playbook and ask your CPA sharper questions, not as a substitute for advice on your specific return.

Step 1: Pick the Test You Will Actually Win

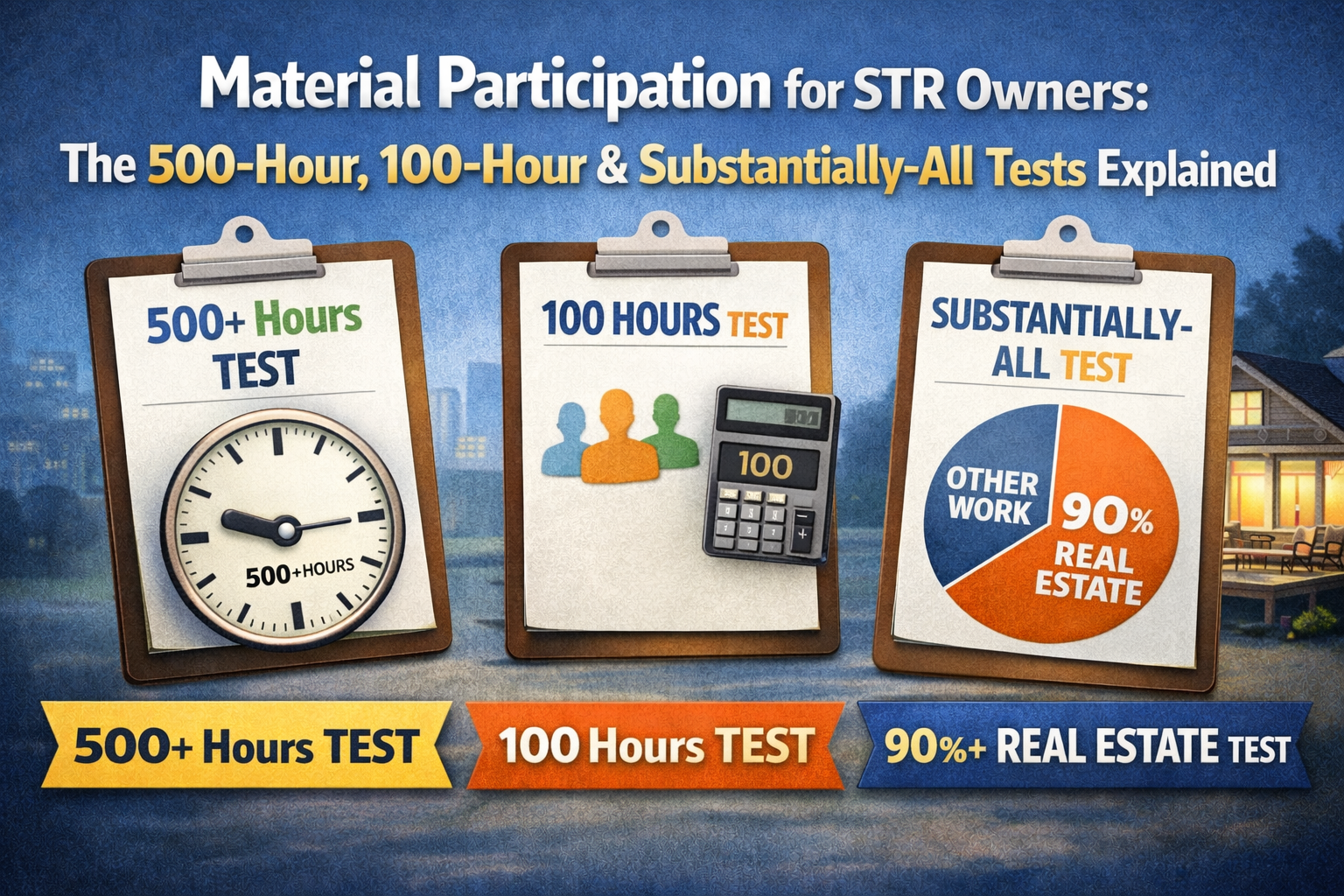

Material participation is defined by the seven tests of Treasury Regulation Section 1.469-5T, but you do not need to satisfy all seven. You need exactly one. The single most important decision in this whole process is choosing which one, because the right choice can cut your required effort by hundreds of hours. For short-term rental owners, three tests do almost all the real work.

The 100-Hour Test (most STR owners' best bet)

- You participate more than 100 hours during the year, AND no other single individual participates more than you do.

- Realistic for a hands-on owner self-managing one or two properties.

- The danger is the second half: a busy cleaner or active co-host can rack up more hours than you and break it.

- Requires tracking not just your hours, but everyone else's hours too.

The 500-Hour Test (the bulletproof option)

- You participate more than 500 hours during the year, full stop, regardless of what anyone else does.

- No comparison to other people, so a hard-working cleaner cannot defeat it.

- 500 hours is roughly 10 hours a week, every week. Demanding but achievable for a portfolio.

- The cleanest test to defend in an audit because it is a single, simple number.

The third common route is the substantially-all test: if you (and your spouse, whose hours count toward your material participation) perform substantially all of the participation in the activity for the year, you qualify. This fits the truly solo operator who handles nearly everything personally and uses outside help only rarely. It has no specific hour floor, but "substantially all" is a high bar, and any meaningful contribution from a paid manager or co-host can knock you out of it.

Decision rule of thumb: if you self-manage and out-work everyone, aim at the 100-hour test and document that you out-participated others. If you use a lot of paid help but still put in serious time, target the 500-hour test, because it ignores everyone else. Pick one as your primary target and treat the others as fallbacks.

One more practical point: if you own more than one short-term rental, you generally test material participation per activity unless you make a valid grouping election to treat them as a single activity. Grouping can make the 500-hour test far easier to reach across a portfolio, but it is a formal election with its own consequences, so make that call with your CPA before the year is over, not after.

Step 2: Know Which Activities Actually Count

Material participation means involvement that is regular, continuous, and substantial. For a short-term rental, the good news is that running the business well naturally generates qualifying hours, you just have to recognize them and capture them. Operating an STR is closer to running a tiny hotel than holding a long-term rental, and almost every operational task you personally perform is participation.

- Guest communication: answering inquiries, screening bookings, sending check-in instructions, responding to mid-stay messages, handling complaints and refunds.

- Turnover coordination: scheduling cleanings between bookings, inspecting the unit, restocking consumables, doing or directing the laundry and reset.

- Pricing and revenue management: setting and adjusting nightly rates, managing minimum-stay rules, running promotions, analyzing occupancy and competitor pricing.

- Maintenance and repairs: diagnosing issues, dispatching and meeting tradespeople, performing small fixes yourself, managing warranties and recurring service.

- Supplies and logistics: shopping for and delivering linens, toiletries, kitchen goods, and replacements; managing inventory.

- Bookkeeping and admin: reconciling income and expenses, managing the listing and calendar across platforms, handling occupancy-tax filings, reviewing reviews and updating the listing.

Two important limits keep these hours honest. First, the regulations exclude work that an owner would not customarily do and that is done mainly to manufacture hours, so don't invent busywork to pad the log. Second, and this trips up many investors, time spent purely as an investor, reviewing financial statements, studying operations in a non-management capacity, does not count unless you are also involved in day-to-day management. The hours that count are operational and managerial, not passive review.

Travel time is a gray area worth flagging: time spent traveling to and from the property for genuine operational work is often defensible, but it should be reasonable and tied to a real task, not used to inflate a borderline log. When in doubt, record the underlying task and the travel separately so the picture is transparent.

Step 3: Build the Hours On Purpose

Material participation is not something you discover at tax time; it is something you build through the year on purpose. If you wait until December to count, you will almost always come up short and be tempted to reconstruct hours from memory, which is exactly the kind of estimate that fails under scrutiny. The owners who clear their chosen test reliably do two things: they front-load real work and they keep a tally as they go.

The single biggest lever is the acquisition and setup phase. Personally handling the furnishing, staging, photography, listing creation, pricing setup, and systems configuration of a new short-term rental can legitimately generate a large block of operational hours in a short window, often enough to put a real dent in your annual target before the first guest arrives. Doing this work yourself, rather than handing it to a setup service, is one of the most effective ways to reach the 100-hour line early.

- Confirm your average guest stay is on track to stay at or under seven days for the year, since material participation is irrelevant if you miss the 7-day rule.

- Choose your primary material participation test (100-hour, 500-hour, or substantially-all) and write down the target number.

- List every operational task you will personally perform and roughly how many hours each will take across the year.

- Personally handle as much of the setup, furnishing, and listing creation as you reasonably can to front-load qualifying hours.

- Set a recurring reminder to log hours weekly rather than reconstructing them later.

- Identify everyone else who will work on the property and plan how to keep your hours above theirs (for the 100-hour test).

- Mid-year, total your hours and compare against your target so you can course-correct while there is still time.

The mid-year check is the step almost everyone skips and the one that saves the most plans. Knowing in July that you are at 40 hours against a 100-hour target gives you five months to do real, legitimate work. Discovering it in March of the following year gives you nothing but a difficult conversation with your CPA.

Step 4: Manage Cleaners, Co-Hosts, and Property Managers

This is where the most strategies quietly die, so read it twice. The hours of your cleaner, your co-host, your handyman, and your property manager are not your hours. They never count toward your material participation. Worse, under the 100-hour test, their hours are counted against you, because that test requires that no other individual participates more than you do. A diligent cleaning team that spends six hours per turnover across a busy season can easily clear 150 to 200 hours, and if you only logged 110, you have failed the very test you were relying on.

The key word is individual. The 100-hour test compares you to each other person separately, not to everyone combined. So three different cleaners who each work 40 hours do not automatically beat your 110 hours, but one cleaner who works 120 does. This is why you must track other people's hours by person, not as a lump sum, and why the makeup of your team matters as much as the total work outsourced.

Choices that protect your hours

- Self-manage guest communication, pricing, and booking decisions rather than delegating them.

- Spread outsourced work across multiple individuals so no single person out-works you.

- Personally coordinate and inspect turnovers even when someone else does the cleaning.

- If outside help is heavy, aim at the 500-hour test, which ignores other people entirely.

Choices that put your claim at risk

- Hiring a full-service property manager who handles nearly everything (this is the classic plan-killer).

- Relying on one cleaner for every turnover all season while logging modest owner hours.

- Counting your manager's or cleaner's hours as if they were yours.

- Targeting the substantially-all test while paying others to do most of the work.

A full-service property manager deserves special warning. If a manager handles guest communication, pricing, turnovers, and maintenance, two bad things happen at once: your own operational hours shrink because there is little left for you to do, and the manager's hours almost certainly exceed yours. That combination defeats the 100-hour test and makes the 500-hour test nearly impossible. The short-term rental loophole and a hands-off, fully managed property are largely incompatible. If you want the tax benefit, you have to stay genuinely involved.

Because the 100-hour test is a head-to-head comparison, you have to be able to show you out-participated every other individual. REP Helper tags each logged activity by who performed it, owner, spouse, cleaner, co-host, or property manager, so you can prove at a glance that no single person beat your hours, instead of guessing at the end of the year.

Step 5: Use Spouse Hours Correctly

There is one person whose hours help you instead of hurting you: your spouse. For material participation purposes, the participation of your spouse counts toward your material participation, whether or not you file a joint return and whether or not the spouse has any ownership interest in the activity. This is a genuinely useful tool that many couples leave on the table.

Practically, this means a household can combine efforts to clear a test that neither spouse would clear alone. If one spouse handles guest communication and bookkeeping while the other manages turnovers and maintenance, their combined operational hours count toward your participation. For the 100-hour test, the comparison is then between your combined household hours and each other outside individual, which makes it considerably easier to stay on top.

Do not confuse this rule with the Real Estate Professional tests. The 750-hour and 50%-of-working-time REP tests are measured per individual and a spouse cannot lend hours to them. The spouse-hours rule for material participation is separate and more generous, which is one more reason the short-term rental path can work for couples where full REP status would not.

The catch is documentation. Spouse hours only help if you can show who did what, when, and for how long, just like your own. Log your spouse's tasks with the same discipline you apply to yours, attributed to them by name, so the combined total is transparent and defensible rather than a vague assertion that "we both worked on it."

Step 6: Log It So It Survives an Audit

You can do all the right work and still lose if you cannot prove it. Tax Court decisions in this area turn again and again on the quality of the time log, and reconstructed estimates, round numbers, and "ballpark" totals routinely fail. The regulations technically allow you to establish participation by any reasonable means, but in practice a contemporaneous, detailed log is the standard that holds up. A calendar created the week before you meet your accountant does not.

A defensible log captures four things for every entry: the date, the time spent, who performed the work, and a specific description of the task. Specificity matters. "Managed property, 3 hours" is weak; "Coordinated and inspected turnover for departing guest, restocked consumables, and messaged incoming guest with check-in details, 1.5 hours" is strong. The detail demonstrates that the work was real operational management, not investor review or invented busywork.

- Record entries contemporaneously, ideally the same day, not from memory months later.

- Tag every entry with the person who did the work so you can run the 100-hour comparison.

- Describe the specific task, not a vague category, so the operational nature is obvious.

- Keep corroborating evidence: guest message timestamps, cleaning invoices, repair receipts, calendar entries, and platform activity that line up with your log.

- Track other people's hours alongside your own so the comparison is complete, not one-sided.

- Keep the records with your tax file for at least the years the return remains open to examination.

This is the pain point REP Helper was built for. It logs material-participation hours contemporaneously by phone, voice, or web so entries happen in the moment rather than from memory, tags each activity by who performed it, tracks your running progress toward your chosen test, and produces CPA-ready documentation, alongside the average-stay calculation that confirms you cleared the 7-day rule in the first place.

Step 7: Connect It to the Depreciation Payoff

It is worth remembering why all this hour-tracking is worth the effort: material participation is what lets you actually use the large depreciation deductions that make the short-term rental strategy famous. A cost segregation study, performed by a specialist engineering firm, reclassifies parts of your building into shorter recovery periods (5-, 7-, and 15-year property) instead of the standard 27.5 or 39 years. Those shorter-life components are eligible for bonus depreciation.

Under the 2025 One Big Beautiful Bill Act, 100% bonus depreciation was restored for qualified property acquired and placed in service after January 19, 2025, after the earlier step-down years (80% in 2023, 60% in 2024, and 40% for property placed in service in early 2025 before the change). That can convert a chunk of your purchase into a first-year deduction. But the deduction only offsets your active income if the loss it creates is non-passive, and the loss is only non-passive if you materially participated. Cost segregation builds the deduction; material participation unlocks it.

Keep proof of your placed-in-service date with your participation log. Depreciation begins when the property is ready and available for its intended use, meaning listed and available to rent, and it must be placed in service by December 31 to deduct for that year. The placed-in-service date and your material participation are the two facts that, together, let the depreciation flow through to your return.

One honest caveat to keep in view: depreciation is not free money. When you sell, depreciation recapture applies, and gain attributable to depreciation is taxed, partly at rates up to 25% for real property and at ordinary rates for personal-property components. The strategy is powerful for deferral and for offsetting active income now, but plan the exit with your advisor so the recapture does not surprise you later.

Frequently Asked Questions

Q: Do I need Real Estate Professional status to use the short-term rental loophole?

A: No, and that is the whole point. If your average guest stay is seven days or fewer, the property is not a rental activity under Treasury Regulation Section 1.469-1T(e)(3), so the 750-hour and 50%-of-working-time REP tests never apply. You only need to materially participate under one of the seven tests of Treasury Regulation Section 1.469-5T. That is why the strategy works for people with demanding full-time jobs in unrelated fields.

Q: How many hours do I really need to materially participate?

A: It depends on the test. The 500-hour test requires more than 500 hours and ignores everyone else. The 100-hour test requires more than 100 hours but also requires that no other single individual participates more than you do. The substantially-all test has no fixed hour floor but requires that you (and your spouse) perform nearly all the work. Most hands-on owners target the 100-hour test and use the 500-hour test as a fallback when they outsource heavily.

Q: Can my cleaner's or property manager's hours count toward my participation?

A: No. Hours worked by a cleaner, co-host, handyman, or property manager never count as your hours, and under the 100-hour test they count against you, because that test requires no other individual to participate more than you. A full-service property manager is especially dangerous because it both shrinks your hours and likely exceeds them. Only your spouse's hours count toward your material participation.

Q: What kind of records do I need to prove material participation?

A: A contemporaneous log that records, for each entry, the date, hours, the specific task, and who performed it, backed by corroborating evidence like guest messages, cleaning invoices, and repair receipts. Reconstructed estimates and round numbers tend to fail in audits. Tracking other people's hours alongside your own is essential so you can prove you out-participated everyone for the 100-hour test. This is exactly the documentation REP Helper produces.

Q: Is any of this a substitute for professional tax advice?

A: No. The figures and rules here are illustrative and the law is fact-specific. A qualified tax advisor should confirm your test, your grouping decisions, and your eligibility, and a specialist firm should perform any cost segregation study. Use this guide to run your playbook through the year and to ask your CPA sharper, better-documented questions.

About the author

Real Estate Investor · Founder, REP Helper

Carlos Lourenço is a real estate investor and the founder of REP Helper. Over 10+ years he's built a portfolio of long- and short-term rentals across several states, personally qualifying for Real Estate Professional Status (REPS) and running the short-term-rental strategy on his own properties. A product manager by trade, he built REP Helper after years of tracking his own hours and IRS tests by hand.

Connect on LinkedInDisclaimer: Carlos Lourenço is a real estate investor, not a CPA, enrolled agent, or tax attorney. This article is for educational purposes only and is not tax, legal, or financial advice. Tax outcomes depend on your specific facts and on current law, which changes. Always consult a qualified CPA or tax attorney before implementing any tax strategy.