The 2026 Landscape at a Glance

If you have been watching the short-term rental (STR) loophole, the last few years felt like a moving target. Bonus depreciation was sliding toward zero, every year-end article warned you the window was closing, and the political climate around real estate tax breaks was hard to read. Then the 2025 One Big Beautiful Bill Act (OBBBA) changed the math. This article is not another explainer of how the loophole works mechanically. It is a forward-looking landscape piece: where things actually stand in 2026, what the new law did and did not do, what could still change, and what an investor should genuinely keep an eye on.

The short version is that the strategy is on firmer footing than it has been in years, but the reasons people lose on audit have not changed at all. The legislative wind is at your back on depreciation. The execution risk is still entirely on you. Understanding that split is the whole point of planning well in 2026.

Quick framing: the STR loophole lets a short-term rental escape the automatic-passive rule. Cost segregation and bonus depreciation supply the large deductions. Material participation is what lets you actually use them. The 2026 news is mostly about that middle piece.

What the Loophole Actually Is (and Isn't)

Before talking about what changed, it helps to be precise about what the loophole is, because a lot of confusion in 2026 comes from people thinking Congress created or could simply repeal it. It did not, and largely cannot with a single line.

Under Treas. Reg. 1.469-1T(e)(3), an activity is generally a 'rental activity' if customers use the property for an average period of more than seven days. If your average guest stay is seven days or fewer, the activity falls outside that definition. That single fact is the entire loophole: a property that is not a 'rental activity' is not automatically passive, which means you do not need Real Estate Professional status (REP, sometimes written REPS) to treat losses as non-passive. You still must materially participate, but you escape the high bar that traps most W-2 earners who own long-term rentals.

Average stay is computed per property for the year: total rental nights divided by the number of separate reservations. Most people miscount this. A handful of longer bookings can quietly push your average over seven days, and you would not know until a CPA or an examiner runs the numbers. This is exactly why REP Helper calculates your average stay per property directly from your bookings, so you find out you are over the line in February, not during an audit.

The Loophole IS

- A regulatory definition, not a one-time tax cut

- An exception to the automatic-passive rule for rentals

- Available to ordinary W-2 earners without REP status

- Dependent on a seven-day-or-fewer average stay

- Still gated by material participation

The Loophole IS NOT

- A statute Congress passed that could be 'repealed' easily

- An automatic write-off just for owning an Airbnb

- A substitute for materially participating

- Safe if your average stay creeps above seven days

- The same thing as bonus depreciation (that is separate)

The Big 2025 Change: OBBBA Restored 100% Bonus Depreciation

The headline development driving the 2026 outlook is the 2025 One Big Beautiful Bill Act. It permanently restored 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025. This reversed the phase-down schedule that had been steadily eroding the value of the strategy.

To appreciate why this matters, look at where the rules had been heading. Bonus depreciation was 80% for property placed in service in 2023, dropped to 60% in 2024, and was scheduled to keep falling. Property placed in service in early 2025, before the law changed, fell under the 40% rate. After January 19, 2025, qualified property is back to 100%. For an STR owner using cost segregation, that is the difference between deducting a large chunk of reclassified components immediately versus spreading a meaningful portion over future years.

- 2023: 80% bonus depreciation on qualified property

- 2024: 60% bonus depreciation

- Early 2025 (before Jan 19): 40% under the old phase-down

- After January 19, 2025: 100% bonus depreciation restored, permanently per OBBBA

Here is the mechanism that makes this so powerful for STRs. A cost segregation study is an engineering-based analysis that reclassifies building components, things like flooring, cabinetry, appliances, certain electrical and plumbing serving equipment, and land improvements, into shorter MACRS recovery periods of 5, 7, or 15 years instead of the default 27.5 or 39 years. Assets with a recovery period of 20 years or less are eligible for bonus depreciation. With 100% bonus back in play, those reclassified, shorter-life assets can be deducted in full in the first year. Cost segregation finds the deductions; bonus depreciation accelerates them; the loophole and material participation determine whether you can use them against your W-2 income.

Worth saying plainly: the word 'permanently' in tax law means 'until a future Congress changes it.' Treat 100% as the firm current rule for planning, not as an unbreakable promise. We cover that nuance in the risk section.

What the New Rules Mean for STR Investors

For someone buying or already operating a short-term rental, the restored 100% bonus changes the planning conversation in a few concrete ways.

- Cost segregation is more attractive again. When bonus sat at 40-60%, a study still helped, but a larger share of deductions was deferred. At 100%, the front-loaded benefit is back to its full strength, which improves the return on the cost of the study itself.

- Timing of placed-in-service matters as much as ever. Depreciation starts when the property is ready and available for its intended use, meaning listed and available to rent. To claim the deduction in a given year, that has to happen by December 31.

- The bottleneck shifts entirely to material participation. With the depreciation rules favorable, the question is no longer 'how big is the deduction' but 'can I legally use it this year against active income.' That answer turns on whether you materially participate.

- Documentation is the new differentiator. A favorable law plus weak records is still a losing audit. The investors who win in 2026 are the ones who can prove average stay and hours, not the ones with the biggest spreadsheet of projected savings.

Notice that none of these advantages help if your average stay drifts above seven days or if a property manager logged more hours than you did. The favorable depreciation rules amplify a correctly structured strategy; they do nothing for a structurally flawed one. That is the recurring theme of the 2026 outlook: the law got friendlier, the discipline requirements did not get easier.

The Regulatory and Political Climate

Tax strategy does not exist in a vacuum, and the climate around real estate tax breaks shapes how comfortable you should feel leaning in. A few currents are worth tracking heading through 2026.

At the federal level, the OBBBA's restoration of 100% bonus signals a political environment that, for now, favors capital investment incentives, including those that flow to real estate. That is a meaningful tailwind. But tax policy is cyclical. Bonus depreciation has been raised, lowered, and scheduled to expire multiple times over the past decade. The current 'permanent' status reflects the present majority's priorities, not a structural guarantee. Any future shift in control of Congress could reopen the question, which is why prudent investors capture benefits while the rules are clear rather than counting on them indefinitely.

At the state and local level, the bigger near-term pressure on STRs is not tax law at all, it is regulation of the rentals themselves. Cities continue to tighten permitting, occupancy caps, registration requirements, and outright bans in some neighborhoods. None of that changes the federal loophole, but it can quietly defeat the strategy: if local rules force you into longer minimum stays, your average could climb past seven days and you lose the non-rental classification entirely. The federal door stays open while the local door closes.

The pattern to internalize for 2026: federal depreciation policy is currently favorable; local STR regulation is generally tightening. Your strategy can be undone from the bottom up even when the top-down rules are friendly.

Sunset and Risk Factors to Watch

Calling something permanent does not make it immune to risk. Here are the forward-looking factors that could change the calculus, ranked roughly by how much you can control them.

- Future legislative change. A later Congress could reduce or re-phase bonus depreciation. The current 100% is the law today, but 'permanent' is a political status, not a contractual one. Do not build a plan that only works if the rate never moves.

- Local regulation forcing longer stays. The most immediate, concrete risk for many owners. Minimum-stay ordinances can push your average over seven days and break the loophole's threshold requirement.

- Recapture on sale. Accelerated depreciation is not free money; it is a timing benefit. On sale, gain attributable to depreciation is recaptured, taxed up to 25% for real property and at ordinary rates for personal-property components. A big first-year deduction can become a meaningful tax bill later.

- Personal-use creep, especially in house hacking. Under Section 280A, if you personally use the dwelling more than the greater of 14 days or 10% of rental days, it is treated as a residence and your loss deductions are limited.

- Self-rental traps. Renting your STR to your own LLC or company does not create a tax-free arrangement. Under Section 469, net rental income from property you rent to an activity you materially participate in is recharacterized as non-passive, while losses generally stay passive. It usually does not help the loophole and can surprise people who assume it does.

The common thread: most of what could go wrong is not a future law change you cannot influence. It is execution risk, average stay, personal use, structure, and documentation, all of which are within your control today. That is good news. It means the smart response to uncertainty is not to wait, but to execute cleanly and keep records that survive scrutiny.

IRS Scrutiny Trends on STR Loophole Claims

As the STR loophole has gone mainstream, it has attracted attention. Large first-year losses from cost segregation, offsetting high W-2 income, on a recently acquired property, are exactly the kind of pattern that draws a second look. The encouraging part is that examiners tend to probe the same two pressure points, so you know in advance where to be airtight.

Pressure Point 1: Average Stay

- Was the seven-day-or-fewer threshold actually met for the year?

- Computed correctly per property, total nights divided by reservations?

- Did a few longer bookings push the average over the line?

- Is there booking data to back the number, not just an estimate?

Pressure Point 2: Material Participation

- Did the owner truly meet one of the seven Reg. 1.469-5T tests?

- Were hours logged contemporaneously, or reconstructed later?

- Did a cleaner, co-host, or property manager out-participate the owner?

- Whose hours are being counted, and can they be attributed?

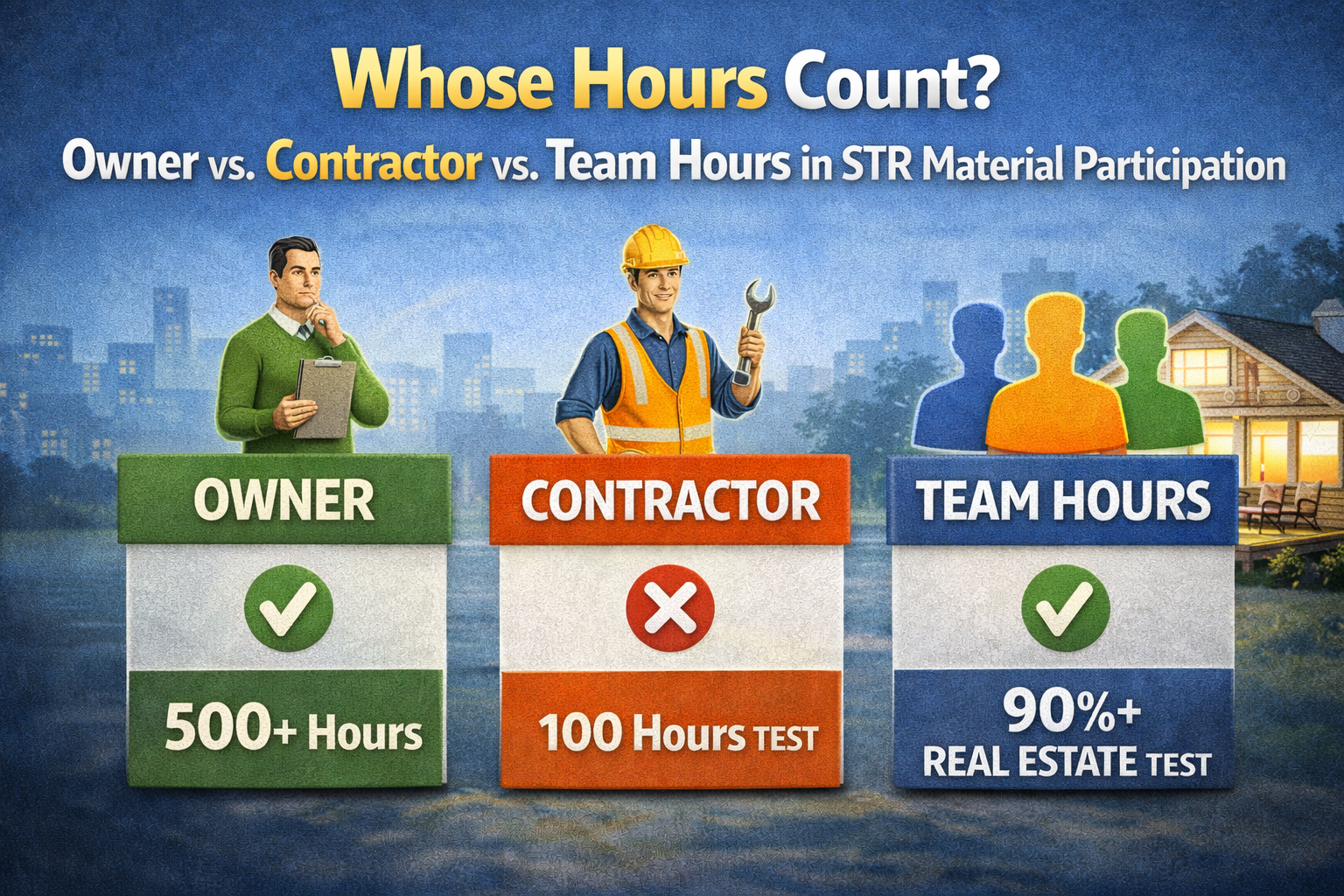

Material participation is where most claims unravel. The common tests for STR owners are: more than 500 hours in the activity; or more than 100 hours when no one else participates more; or doing substantially all of the participation yourself. The trap is the 100-hour test. Contractor, employee, and property-manager hours do not count as your hours, and they can defeat that test by showing someone else participated more than you did. A self-managed owner who hires a full-service property manager often loses precisely here.

This is the single most defensible thing to get right, and it is hard to fix after the fact. REP Helper logs your material-participation hours contemporaneously by phone, voice, or web, and tags each activity by who performed it, owner, spouse, cleaner, co-host, or property manager, so you can demonstrate you out-participated everyone else for the 100-hour test. It tracks your progress toward whichever test you are targeting and keeps the placed-in-service date and supporting evidence. Reconstructed logs invite skepticism; contemporaneous, attributed logs answer the examiner's question before it is asked.

What to Watch Through 2026 and Beyond

If you want a short watchlist to carry into the rest of the year, focus on signals you can actually act on rather than headlines you cannot.

- Federal bonus depreciation rate: confirm 100% still applies to your placed-in-service date before relying on it for a large deduction.

- Your local STR ordinances: check for new minimum-stay, permitting, or registration rules that could push your average stay over seven days.

- Your own average stay, recomputed as bookings come in, not estimated once at purchase.

- Your material-participation hours versus everyone else's on each property, all year long.

- Placed-in-service timing for any acquisition or improvement you want to deduct this tax year, with a Dec 31 deadline in mind.

- Recapture exposure if a sale is on the horizon, so the first-year benefit is weighed against the eventual tax on the gain.

Cost segregation studies themselves are performed by specialist engineering firms, and choosing a quality provider matters. But the study only delivers a usable result if you can prove the two things the IRS actually asks about: that your average stay qualifies and that you materially participated. That proof is the part you build all year, and it is where REP Helper produces CPA-ready documentation that ties your bookings, your hours, and your placed-in-service evidence into one defensible package. The favorable 2026 depreciation rules reward the investor who shows up with that file and frustrate the one who does not.

The Bottom Line for 2026

The 2026 outlook for the STR loophole is, on balance, a good-news story with an asterisk. The good news: OBBBA restored 100% bonus depreciation for qualified property placed in service after January 19, 2025, the loophole's underlying regulatory definition is intact, and the strategy is more valuable than it was during the phase-down years. The asterisk: 'permanent' is political, local regulation is tightening, recapture awaits on sale, and material participation is still where most claims fail.

The rational response is not to time the law but to execute cleanly while the rules are favorable. Confirm your average stay qualifies, document your hours contemporaneously and by participant, mind your placed-in-service dates, and keep records that would satisfy an examiner. Do those things and a future change to bonus depreciation cannot retroactively unwind a deduction you have already properly earned and used.

This article is general education, not personalized tax advice. Bonus depreciation rates, local STR rules, and your own facts vary. Work with a qualified tax advisor and a reputable cost segregation firm before acting, and use them to confirm the current rate for your specific placed-in-service date.

Frequently Asked Questions

Q: Did the 2025 OBBBA create or expand the STR loophole itself?

A: No. The STR loophole comes from the long-standing regulation, Treas. Reg. 1.469-1T(e)(3), that treats a property with an average guest stay of seven days or fewer as a non-rental activity. OBBBA did not touch that definition. What it changed was bonus depreciation, restoring it to 100% for qualified property placed in service after January 19, 2025. The loophole determines whether you can use accelerated depreciation against active income; OBBBA made that depreciation larger and front-loaded again. They work together, but they are separate rules.

Q: Is 100% bonus depreciation guaranteed to stay forever?

A: It is the current law and was enacted as permanent, so you can plan around it today. But 'permanent' in tax means until a future Congress changes it, and bonus depreciation has been adjusted repeatedly over the past decade. The practical takeaway is to capture the benefit on property you place in service while the 100% rate clearly applies, rather than assuming the rate will never move. Confirm the rate for your specific placed-in-service date with a tax professional before relying on it.

Q: If the depreciation rules are favorable now, can I skip the material-participation work?

A: No, and this is the most common 2026 misconception. Bonus depreciation creates the deduction, but you can only use it against W-2 or other active income if your losses are non-passive, which requires you to materially participate under one of the seven tests in Treas. Reg. 1.469-5T. A large deduction you cannot use this year is just a suspended passive loss. Logging hours contemporaneously and tagging who performed each task, which is what REP Helper is built to do, is what turns a paper deduction into a usable one.

Q: Could local STR regulations affect my federal tax strategy?

A: Indirectly but importantly. Local rules do not change federal law, but if a city imposes a minimum-stay requirement, your average guest stay can rise above seven days. Once that happens, the property is a 'rental activity' again, you lose the loophole's exception, and your losses default back to passive unless you qualify under Real Estate Professional rules. So a local ordinance can quietly break a federal strategy. Tracking your actual average stay per property as bookings come in is how you catch this early.

Q: What is the biggest audit risk in 2026 for STR loophole claims?

A: Examiners concentrate on two things: whether your average stay genuinely met the seven-day-or-fewer threshold, computed correctly per property, and whether you truly materially participated rather than letting a cleaner, co-host, or property manager out-participate you. The 100-hour test is the frequent failure point because contractor and manager hours do not count as yours and can show someone else did more. Contemporaneous, participant-tagged records and booking-based average-stay figures are the most defensible answers to both questions.

About the author

Real Estate Investor · Founder, REP Helper

Carlos Lourenço is a real estate investor and the founder of REP Helper. Over 10+ years he's built a portfolio of long- and short-term rentals across several states, personally qualifying for Real Estate Professional Status (REPS) and running the short-term-rental strategy on his own properties. A product manager by trade, he built REP Helper after years of tracking his own hours and IRS tests by hand.

Connect on LinkedInDisclaimer: Carlos Lourenço is a real estate investor, not a CPA, enrolled agent, or tax attorney. This article is for educational purposes only and is not tax, legal, or financial advice. Tax outcomes depend on your specific facts and on current law, which changes. Always consult a qualified CPA or tax attorney before implementing any tax strategy.