A Strategy Hiding in Plain Sight, and Misread by the Pros

The short-term rental loophole is one of the few legitimate ways a high-earning W-2 professional can use real estate losses to offset salary, business income, or capital gains without quitting their job to become a full-time real estate investor. It is well documented in the regulations, it has been around for decades, and it is not exotic. And yet it is one of the strategies most frequently botched, not by aggressive promoters on the internet, but by ordinary, competent, well-meaning CPAs.

That sounds harsh, so let us be precise about why it happens. The STR loophole sits at the intersection of two areas most preparers handle on autopilot: rental real estate (which they reflexively treat as passive) and the passive activity rules of Internal Revenue Code Section 469 (which most clients never trigger in an interesting way). The loophole works by stepping outside the normal rental rules entirely. A preparer who is not specifically looking for it will pattern-match your property to every other rental on their roster and apply exactly the wrong treatment, often without realizing a different path even existed.

This is not a hit piece on CPAs. A good preparer is worth far more than they cost. The point is that the STR loophole is a specialty inside a specialty, and you cannot assume your preparer has seen it before. This article shows you the five errors so you can recognize them, and gives you the questions that separate a preparer who knows this terrain from one who is guessing.

None of this is a substitute for advice on your specific return. Treat it instead as a way to ask your CPA sharper questions and to judge the quality of the answers you get back. The whole strategy hinges on a handful of facts, and a preparer who can speak fluently about those facts is the one you want.

Mistake 1: Treating the STR Like a Passive Rental

Here is the default a busy preparer falls into. You hand them a property that produced a loss. They open Schedule E, enter the income and expenses, generate the loss, and the software dutifully suspends it as a passive activity loss because rental real estate is passive by default. The loss carries forward, does nothing for your current tax bill, and waits until you sell. From the preparer's seat the return looks correct and tidy. From your seat, the entire reason you bought the property just evaporated.

The error is conceptual, not clerical. Under Treasury Regulation Section 1.469-1T(e)(3), an activity is only a "rental activity" if the average period of customer use is more than seven days. If your average guest stay is seven days or fewer, your property is, for Section 469 purposes, not a rental activity at all. The rule that makes rentals automatically passive simply never attaches. The property is treated like any other trade or business, and whether the loss is passive or non-passive turns on a different question entirely: did you materially participate?

A preparer who never asks about your average guest stay will never know to leave the rental-activity bucket. They will treat a property that legally qualifies for non-passive treatment as just another suspended-loss rental. The losses are not lost forever, but a year or more of tax benefit is, and the difference can be tens of thousands of dollars for a high earner.

The tell: if your preparer never asked how long your guests typically stay, they almost certainly defaulted you into passive treatment. The average-stay question is the front door to this strategy, and skipping it means the door was never opened.

Mistake 2: Confusing the Loophole with REP Status

The opposite error is just as common and, in some ways, more damaging because it looks like sophistication. A preparer has heard that real estate losses can offset W-2 income, knows that the path is Real Estate Professional status, and tells you that you cannot use your STR losses because you do not qualify as a REP. They are applying a real rule to the wrong strategy. The STR loophole does not require REP status and never did.

Real Estate Professional status (often written REPS) is a separate doorway with two demanding gates: you must spend more than 750 hours per year in real property trades or businesses, and more than half of all your personal-service working hours must be in real estate. For someone with a full-time W-2 job, that second test is nearly impossible to clear, which is exactly why so many people are told no. But the STR loophole is built on a completely different mechanism. Because a sub-7-day-average property is not a rental activity, you never have to convert yourself into a real estate professional to escape the per-se passive rule. You sidestep it entirely.

REP Status path (Section 469)

- Requires more than 750 hours in real property trades or businesses

- Requires more than half of all working hours in real estate

- Aimed at long-term, standard rental portfolios

- Realistically out of reach for most full-time W-2 earners

- You become, in the law's eyes, a real estate professional

STR loophole path (Reg. 1.469-1T(e)(3))

- No 750-hour test and no half-of-working-hours test

- Requires only that average guest stay is 7 days or fewer

- Aimed at nightly and weekly short-term rentals

- Workable alongside a demanding full-time job

- You remain a W-2 professional; the property is just non-rental

When a preparer collapses these two paths into one, the practical result is that they tell qualified clients they do not qualify. You walk away believing the strategy is closed to you when, in fact, the simpler door was open the whole time. If your CPA brings up the 750-hour test in the context of your short-term rental, that is a sign they are reaching for the wrong rule.

Mistake 3: Missing or Misreading the 7-Day Average

Even preparers who know the loophole exists frequently get the foundational measurement wrong. The 7-day rule is not about whether your listing allows short stays, whether you market it on a nightly platform, or whether you call it an Airbnb. It is about a specific arithmetic figure: the average period of customer use for the property, computed for the year.

That average is total rental days (nights) divided by the number of separate guest stays or reservations, calculated per property. A property booked for 200 nights across 40 reservations has a 5-day average and qualifies. The same 200 nights across 12 reservations has roughly a 17-day average and does not. A handful of long monthly bookings, a snowbird who stays for six weeks, or an off-season furnished-rental arrangement can quietly drag the average above seven and silently disqualify the property, and a preparer who never runs the math will never catch it.

The mirror-image error is a preparer who assumes the property qualifies because it is on a nightly platform and never documents the actual figure. If the IRS asks how you arrived at a sub-7-day average, "it was an Airbnb" is not an answer. You need the booking-level data showing nights and distinct reservations per property.

Where REP Helper fits: it pulls your bookings and calculates the average stay per property automatically, so you and your preparer can see, before the return is filed, whether each property is genuinely under the 7-day line, and keep the booking-level backup if the figure is ever questioned.

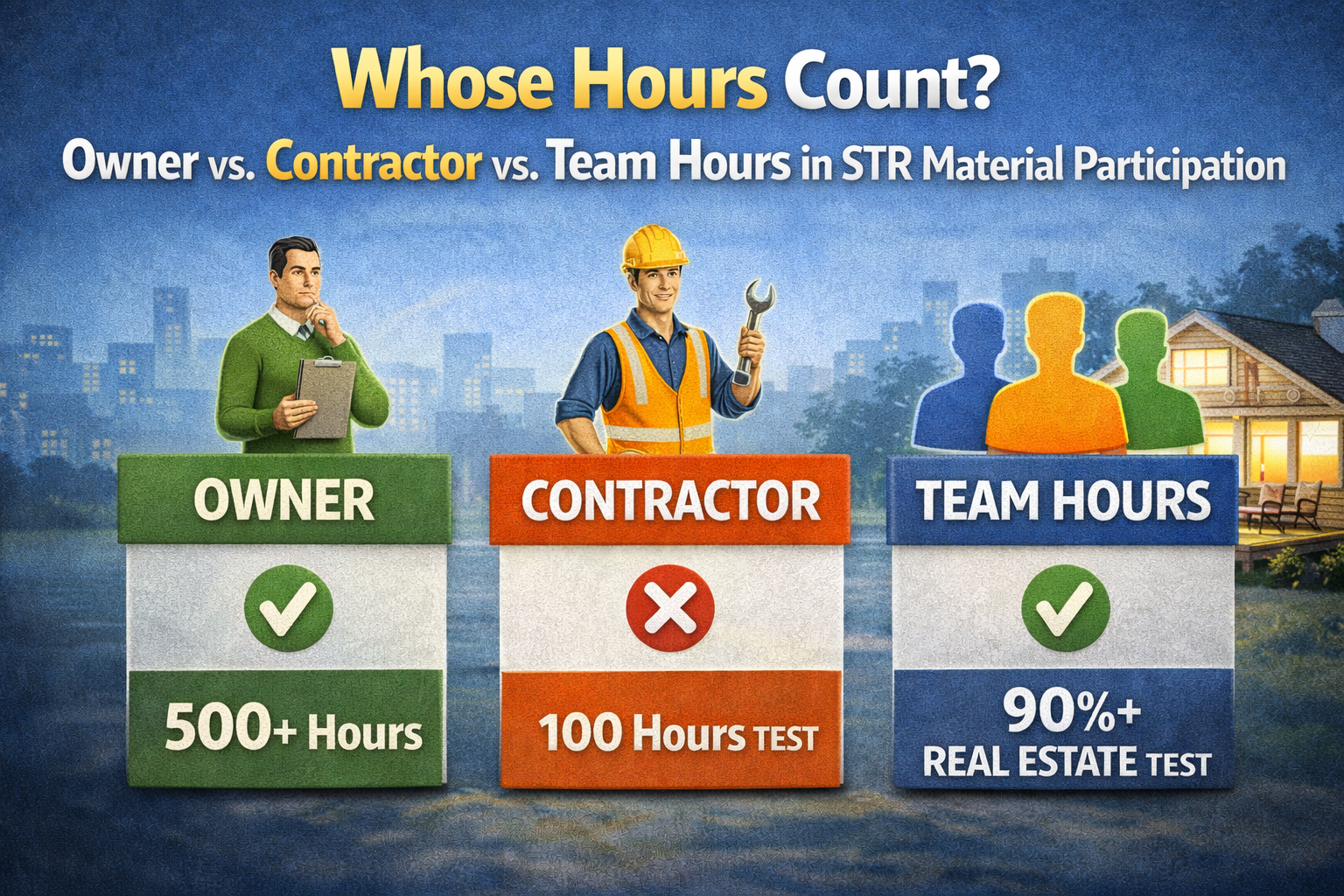

Mistake 4: Mis-Applying the Material Participation Tests

Clearing the 7-day rule only gets you to the starting line. It takes the property out of the rental-activity bucket, but a loss from any trade or business is still passive unless you materially participate. This is the step where preparers most often wave their hands, and it is the step most likely to collapse under audit, because material participation is governed by seven specific tests in Treasury Regulation Section 1.469-5T and only a few of them are realistic for a short-term rental owner.

- The 500-hour test: you participate in the activity for more than 500 hours during the year.

- The substantially-all test: your participation is substantially all of the participation by everyone, including paid help.

- The 100-hour-and-most test: you participate more than 100 hours and no other individual (cleaner, co-host, property manager, contractor) participates more than you do.

- The other tests (such as the significant-participation aggregation and the prior-year tests) exist but rarely fit a single-property STR cleanly, which is why preparers should not lean on them casually.

The error here takes two forms. The first is a preparer who simply asserts material participation without any record of your hours, which is exactly what an examiner is trained to challenge. The second, more subtle, is mis-applying the 100-hour test by ignoring who else worked on the property. The 100-hour test is not just about your hours; it requires that no one else participated more. If you logged 120 hours but your property manager logged 300, you fail, and a preparer who only counts your time will not see the problem coming.

Where REP Helper fits: it logs your participation hours contemporaneously by phone, voice, or web, and tags every activity by who performed it, owner, spouse, cleaner, co-host, or property manager. That is what lets you prove you out-participated everyone else for the 100-hour test and tracks your progress toward whichever of the seven tests you are aiming for.

There is also a quieter trap: contractor, employee, and property-manager hours do not count as your hours. Outsourcing the work can be a perfectly good business decision, but every hour you hand off is an hour that strengthens someone else's participation and weakens yours. A preparer who never asks who actually does the work cannot warn you that your management arrangement is undermining the very test the strategy depends on.

Mistake 5: Being Too Aggressive on Cost Segregation

Cost segregation is what makes the STR loophole feel dramatic. An engineering-based study reclassifies building components into shorter MACRS recovery periods, 5-, 7-, and 15-year property, instead of stretching everything over 39 years. Those shorter-life assets (20-year recovery period or less) qualify for bonus depreciation, and under the 2025 One Big Beautiful Bill Act, 100% bonus depreciation was permanently restored for qualified property acquired and placed in service after January 19, 2025. The result can be a very large first-year deduction.

Here is where preparers and promoters get over their skis. Cost segregation does not create the right to deduct against your active income; it only enlarges a deduction you are entitled to use only if the prior facts are in place. Run an aggressive study, generate a six-figure paper loss, and then fail the 7-day average or fail material participation, and you have built a large passive loss that does nothing this year except draw attention. The deduction is real, but its usefulness is entirely downstream of the two facts this article keeps returning to.

- Aggressive percentages: a study that pushes an implausibly high share of the building into 5- and 15-year buckets to maximize the deduction invites scrutiny and may not survive it.

- DIY or rule-of-thumb studies: a real study is engineering-based and documented; a back-of-the-envelope reclassification is hard to defend.

- Sequencing the deduction before the facts: claiming the loss against W-2 income before confirming the 7-day average and material participation puts the cart before the horse.

- Ignoring placed-in-service timing: depreciation starts when the property is ready and available to rent, and that must occur by December 31 to deduct in that year.

- Forgetting recapture: accelerated depreciation is taxed back on sale, partly at up to 25% for real property and at ordinary rates for personal property, so the benefit is partly a timing shift, not a free deduction.

The disciplined version is unglamorous: the cost segregation study is performed by a qualified specialist firm, the deduction is sized to defensible engineering, and the loss is claimed against active income only after the average-stay and material-participation facts are nailed down and documented. REP Helper does not perform the cost seg study, that is the specialist's job, but it proves the two facts that let you actually use the depreciation the study produces.

How to Vet Your Preparer: Questions That Reveal the Truth

You do not need to become a tax expert to tell whether your preparer is. You need a short list of questions whose right answers are specific and concrete. A preparer who knows this strategy will answer quickly and in the language of the regulations. A preparer who is guessing will reach for reassurance, change the subject to REP status, or tell you not to worry about it.

- How will you classify this property for Section 469 purposes, and does the 7-day average rule apply to it? (Right answer: they reference the average period of customer use and the non-rental-activity treatment.)

- How will we document the average guest stay, per property, for the year? (Right answer: booking-level nights divided by distinct reservations, with backup.)

- Which material participation test are we relying on, and how will we prove it? (Right answer: a named test from Reg. 1.469-5T and a contemporaneous hour log.)

- Whose hours count toward that test, and have you accounted for our cleaner, co-host, or property manager? (Right answer: only the owner's and spouse's hours count, and they compare them against everyone else.)

- Are you treating this as needing REP status? (Right answer: no, the loophole does not require the 750-hour or half-your-hours tests.)

- If we do a cost segregation study, who performs it, and what do we need in place before claiming the loss against my W-2 income? (Right answer: an engineering firm does the study; the 7-day and material-participation facts must be documented first.)

- How do you handle placed-in-service timing and depreciation recapture on a future sale? (Right answer: they can explain both without hesitation.)

If those answers come back crisp, you have found someone who genuinely understands the strategy, and you should keep them. If they come back vague, it does not necessarily mean your preparer is bad at their job; it usually means this particular strategy is outside their normal lane. In that case the fix is not to fire them but to either bring in a specialist for this piece or to arrive at your next meeting with the average-stay and material-participation documentation already in hand, so the conversation starts from facts rather than assumptions.

Where REP Helper fits: it produces CPA-ready documentation, the average stay per property, the contemporaneous hour log tagged by participant, the placed-in-service evidence, so you walk into the meeting with the exact facts your preparer needs to classify the activity correctly instead of defaulting you into passive treatment.

Frequently Asked Questions

Q: My CPA says I cannot use my Airbnb losses because I am not a real estate professional. Are they right?

A: Quite possibly not. The STR loophole does not require Real Estate Professional status, so the 750-hour and more-than-half-your-working-hours tests are irrelevant to it. If your average guest stay is seven days or fewer and you materially participate, the property is not a rental activity and your losses can be non-passive without you ever becoming a REP. If your preparer is invoking REP status to tell you no, they may be applying the wrong rule. It is worth asking them specifically about Reg. 1.469-1T(e)(3) and the average-period-of-customer-use test.

Q: How do I know if my preparer treated my STR as passive by mistake?

A: Look at how the loss landed on your return. If your short-term rental produced a loss and that loss did not reduce your taxable income, it was almost certainly suspended as a passive activity loss. The clearest early warning sign is that your preparer never asked how long your guests typically stay or how many separate reservations you had. Without that data they could not have computed the average stay, and without the average stay they had no basis to take the property out of the per-se passive rental bucket.

Q: Is being aggressive on cost segregation what gets people audited?

A: Aggressive studies can attract scrutiny, but the deeper risk is sequencing. Cost segregation only enlarges a deduction; it does not create the right to use that deduction against your active income. The audit exposure comes from claiming a large loss against W-2 income while the underlying facts, a genuine sub-7-day average and real material participation, are thin or undocumented. A defensible, engineering-based study sized to the actual building, paired with solid documentation of those two facts, is far safer than a big number with nothing behind it. When in doubt, have a qualified cost-seg professional and your tax advisor weigh in.

Q: My property manager handles almost everything. Does that hurt my material participation?

A: It can, and this is a point preparers routinely miss. Hours worked by a property manager, cleaner, co-host, or contractor do not count as your hours, and they actively count against you on the 100-hour test, which requires that no other individual participates more than you do. If your manager logs more hours than you, you can fail that test even if you personally cleared 100 hours. The fix is to participate meaningfully yourself and to track who does what, so you can show you out-participated everyone else or, alternatively, clear the 500-hour test on your own.

Q: Should I switch CPAs if mine got this wrong?

A: Not necessarily. A preparer being unfamiliar with the STR loophole is common and does not make them bad at the rest of your return. The strategy is a niche inside a niche. Often the better move is to bring this specific piece to a specialist or to arrive with your average-stay and hour documentation already prepared, so your existing preparer has the facts they need to classify the activity correctly. If, after seeing the regulations and the documentation, they still insist on passive treatment without a clear reason, that is a stronger signal that it may be time for a second opinion.

About the author

Real Estate Investor · Founder, REP Helper

Carlos Lourenço is a real estate investor and the founder of REP Helper. Over 10+ years he's built a portfolio of long- and short-term rentals across several states, personally qualifying for Real Estate Professional Status (REPS) and running the short-term-rental strategy on his own properties. A product manager by trade, he built REP Helper after years of tracking his own hours and IRS tests by hand.

Connect on LinkedInDisclaimer: Carlos Lourenço is a real estate investor, not a CPA, enrolled agent, or tax attorney. This article is for educational purposes only and is not tax, legal, or financial advice. Tax outcomes depend on your specific facts and on current law, which changes. Always consult a qualified CPA or tax attorney before implementing any tax strategy.